US futures are pointing to a higher open today after ending in red on Wednesday, as the technology sector is poised for a minor recovery. Markets were under pressure this week on global trade war concerns, Facebook’s (FB) data leak scandal, investigation on a fatal Tesla accident and reports that President Donald Trump could be targeting Amazon’s (AMZN) tax treatments. Today marks the official wrap up of the first quarter as Good Friday and Easter break is scheduled ahead.

The S&P futures gained 0.36% to 2,617, Dow futures grew 0.30% to 23,931, and Nasdaq advanced 0.66% to 6,519.75. Elsewhere, shares at Asian markets closed mostly higher on Thursday, and European stocks are trading modestly higher.

On the European economic front, data from the Turkish Statistical Institute showed that Turkey’s gross domestic product grew 7.3% on year in the fourth quarter after rising 11.3% in the third quarter. The Office for National Statistics data revealed that gross domestic product in the United Kingdom rose 0.4% on quarter in the fourth quarter after rising 0.5% last quarter. GfK survey showed that UK consumer sentiment improved to -7 in March from -10 in February.

The Hungarian Central Statistical Office data revealed that industrial producer prices in Hungary climbed 3.9% on year in February after rising 3.3% in January. The labor force survey from Destatis showed that jobless rate in Germany remained unchanged at adjusted 3.5% in February, and the rate climbed on an unadjusted basis to 3.8% from 3.6% last month. Statistics Portugal data revealed that industrial production in Portugal increased 2.1% on year in February after rising 2.5% in January.

On the Asian economic front, data from the Ministry of Economy, Trade, and Industry showed that retail sales value in Japan rose 0.3% on month in February after falling 1.6% in January. The Reserve Bank of Australia data revealed that Australia’s private sector credit grew 0.4% on month in February after rising 0.2% in January. The Department of Statistics data showed that Singapore producer prices declined 0.8% on year in February after falling 1.9% in January.

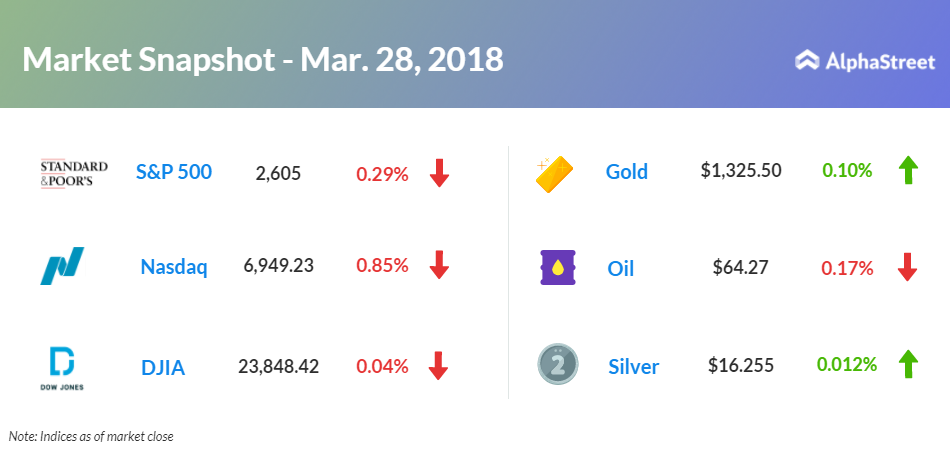

On March 28, US ended lower, with Dow down 0.04% to 23,848.42. Nasdaq tumbled 0.85% to 6,949.23, and S&P 500 slid 0.29% to 2,605. Lingering trade war concerns and a steep fall in technology stocks dragged markets lower. Trump intends to go after Amazon and wants to change Amazon’s tax treatments as mom-and-pop retailers are being put out of business.

A Commerce Department report showed that gross domestic product grew 2.9% in the fourth quarter after increasing 3.2% in the third quarter. The National Association of Realtors report revealed that pending home sales index grew by 3.1% to 107.5 in February, after falling by 5% to 104.3 in January.

Meanwhile, key economic events scheduled for today include jobless claims, personal income, consumer spending, Federal Reserve’s inflation gauge core PCE, Chicago purchasing managers’ index (PMI), Energy Information Agency’s natural gas inventory and Baker Hughes’ rig count. Philadelphia Fed President Patrick Harker will give a speech about economic outlook at the New York Association for Business Economics luncheon.

On the corporate front, Amazon stock rose 1.57% in premarket after traders shed off concerns of Trump intending to change Amazon’s tax treatments. Harley-Davidson (HOG) stock grew 2.09% in premarket after brokerage firm Longbow Research upgraded the shares to Underperform from Neutral. Science Applications International (SAIC) stock rose 1.68% in premarket after better-than-expected fourth-quarter earnings.

Amazon stock rose 1.57% in premarket after traders shed off concerns of Trump intending to change Amazon’s tax treatments.

PVH Corp. (PVH) stock climbed 4.83% in premarket after strong estimate and better-than-expected fourth-quarter results. GameStop (GME) stock slid 2.33% in premarket despite upbeat fourth-quarter results. Progress Software (PRGS) stock jumped 5.77% in the premarket after lifting 2018 earnings outlook and posting better-than-expected first-quarter earnings.

On the earnings front, the key companies reporting earnings today include Movado Group (MOV), Lindsay (LNN), AngioDynamics (ANGO), Constellation Brands (STZ), Worthington Industries (WOR), and Synnex Corp. (SNX).

Crude oil futures is down 0.11% to $64.31. Gold is trading down 0.05% to $1,329.30, and silver is down 0.02% to $16.25. On the currency front, the US dollar is trading down 0.32% at 106.452 yen. Against the euro, the dollar is up 0.11% to $1.2322. Against the pound, the dollar is up 0.02% to $1.4084.