US futures are pointing to a lower open today after ending higher on Tuesday, ahead of Fed meeting minutes and CPI data. Investors remained concerned that the US decision to strike Syria in response to a chemical attack could provoke a response from Russia.

The S&P futures tumbled 0.90% to 2,631, Dow futures fell 0.94% to 24,121, and Nasdaq dropped 0.85% to 6,567.75. Elsewhere, shares at Asian markets closed mixed on Wednesday, and European stocks are trading lower.

On the European economic front, data from Istat showed that Italy’s retail sales rose 0.4% on month in February after falling 0.5% in January. Statistics Portugal data revealed that Portugal’s consumer price inflation accelerated to 0.7% in March from 0.6% in February. Bank of France data showed that France’s manufacturing confidence fell to 103 in March from 105 in February.

Investors remained concerned that the US decision to strike Syria in response to a chemical attack could provoke a response from Russia.

The Office for National Statistics data revealed that industrial production in the UK inched up 0.1% on month in February after increasing 1.3% in January. Another report showed that construction output in the UK fell 1.6% on month and tumbled 3% on year in February. The Office for National Statistics data revealed that visible trade deficit in the UK narrowed to GBP 10.2 billion in February from GBP 12.2 billion in January.

On the Asian economic front, data from the Department of Statistics showed that Malaysia’s industrial production increased 3% on year in February after rising 5.4% in January. The National Bureau of Statistics data revealed that consumer price inflation in China eased to 2.1% in March from 2.9% in February, and producer prices rose 3.1% on year in March after increasing 3.7% in February.

The Bank of Japan data showed that producer prices in Japan fell 0.1% on month in March after rising 0.1% in February. Another Bank of Japan data revealed that bank lending in Japan rose 2% on year in March to 523.08 trillion yen, after increasing 2.1% in February. Westpac Bank data showed that consumer confidence in Australia fell 0.6% to 102.4 in April from 103 in March.

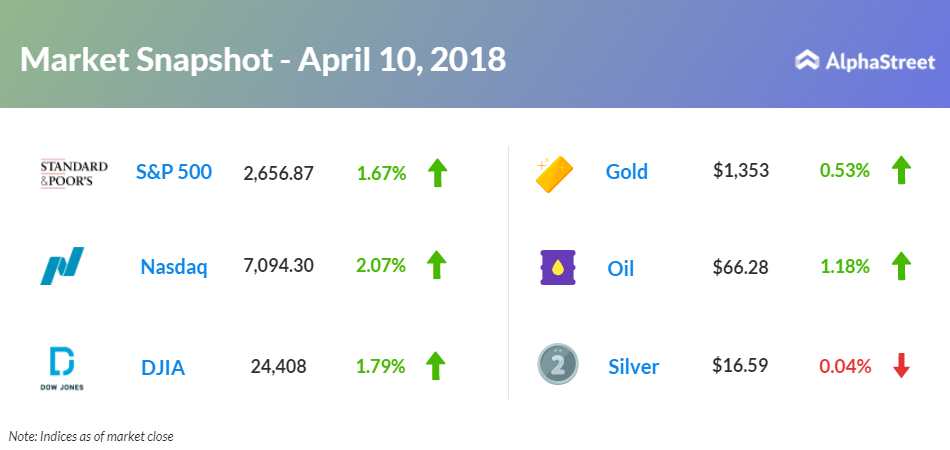

On April 10, US ended higher, with Dow up 1.79% to 24,408. Nasdaq advanced 2.07% to 7,094.30, and S&P 500 gained 1.67% to 2,656.87. Trade tensions eased after Chinese President Xi Jinping lifted limits on foreign investment in automobile and aircraft industries. A Labor Department report showed that producer price index increased by 0.3% in March after rising 0.2% in February.

Meanwhile, key economic events scheduled for today include the Mortgage Bankers’ Association mortgage applications, Labor Department’s consumer price index, Atlanta Fed business inflation expectations, Energy Information Administration petroleum status report, Treasury Department’s treasury budget for March and minutes from the Federal Open Market Committee’s March meeting.

Fastenal (FAST) stock fell 4.36% in the premarket after lower-than-expected first-quarter earnings.

On the corporate front, Fastenal (FAST) stock fell 4.36% in the premarket after lower-than-expected first-quarter earnings. Bed Bath & Beyond (BBBY) stock inched up 0.85% in premarket ahead of the company’s fourth-quarter results after the bell. Twenty-First Century Fox (FOXA) stock tumbled 1.60% in premarket as its UK office drew an inspection by the European Commission for the antitrust probe into sports rights and distribution of sports content.

Crude oil futures are up 1.18% to $66.28. Gold is trading up 0.53% to $1,353, while silver is down 0.04% to $16.59. On the currency front, the US dollar is trading down 0.34% at 106.836 yen. Against the euro, the dollar is up 0.17% to $1.2374. Against the pound, the dollar is down 0.07% to $1.4165.