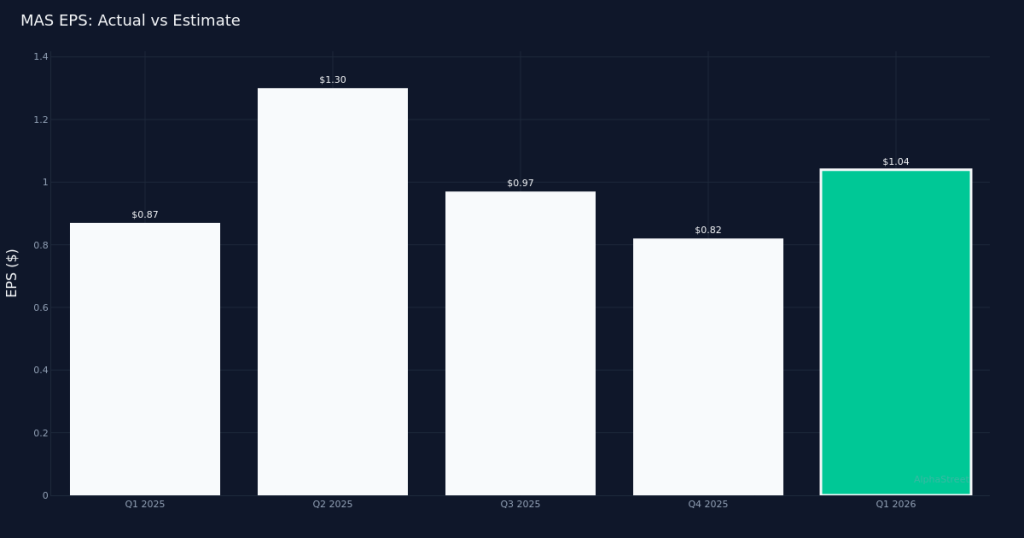

Solid beat. Masco Corporation (NYSE: MAS) reported Q1 2026 adjusted earnings of $1.04 per share, beating the $0.89 consensus estimate by 16.9%, as the building products manufacturer delivered strong performance across its core segments. Revenue totaled $1.92B for the quarter, up 6.0% from $1.80B in Q1 2025, demonstrating resilient demand despite ongoing macroeconomic headwinds in the housing market. The company earned $213.0M in net income during the period.

Revenue-driven performance. The earnings beat appears to be fundamentally sound, driven by top-line growth rather than purely cost management. The 6.0% year-over-year revenue expansion suggests Masco is successfully gaining share and maintaining pricing power in its end markets. This quality of beat is particularly noteworthy given the challenging conditions facing building products companies, with elevated interest rates continuing to pressure new construction and renovation activity. The company’s ability to grow revenue in this environment speaks to the strength of its brand portfolio and distribution relationships.

Plumbing Products shine. The Plumbing Products segment led performance with $1.36B in revenue, up 9.0% year-over-year, highlighting the division’s momentum in both the professional contractor and consumer channels. This segment, which includes brands like Delta and Hansgrohe, represents the lion’s share of Masco’s business and continues to benefit from strong product innovation and the ongoing premiumization trend in kitchen and bath fixtures. The outperformance in this core category should provide confidence that Masco’s market position remains secure.

Confident outlook. Management projected FY 2026 adjusted EPS in the $4.10 to $4.30 range, providing investors with visibility into expected full-year performance. This guidance suggests management anticipates sustained momentum through the remainder of the year, though the range indicates appropriate caution given persistent uncertainty around housing market recovery timing. The midpoint of guidance implies solid earnings growth and reflects management’s confidence in maintaining operational execution across changing market conditions.

Stock response. Wall Street consensus stands at 8 buy, 15 hold, and 1 sell ratings, reflecting a relatively balanced view on the shares.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.