Mastercard (NYSE: MA) reported higher earnings and revenues for the third quarter, which also topped expectations. The credit card firm’s stock gained early Tuesday, following the announcement.

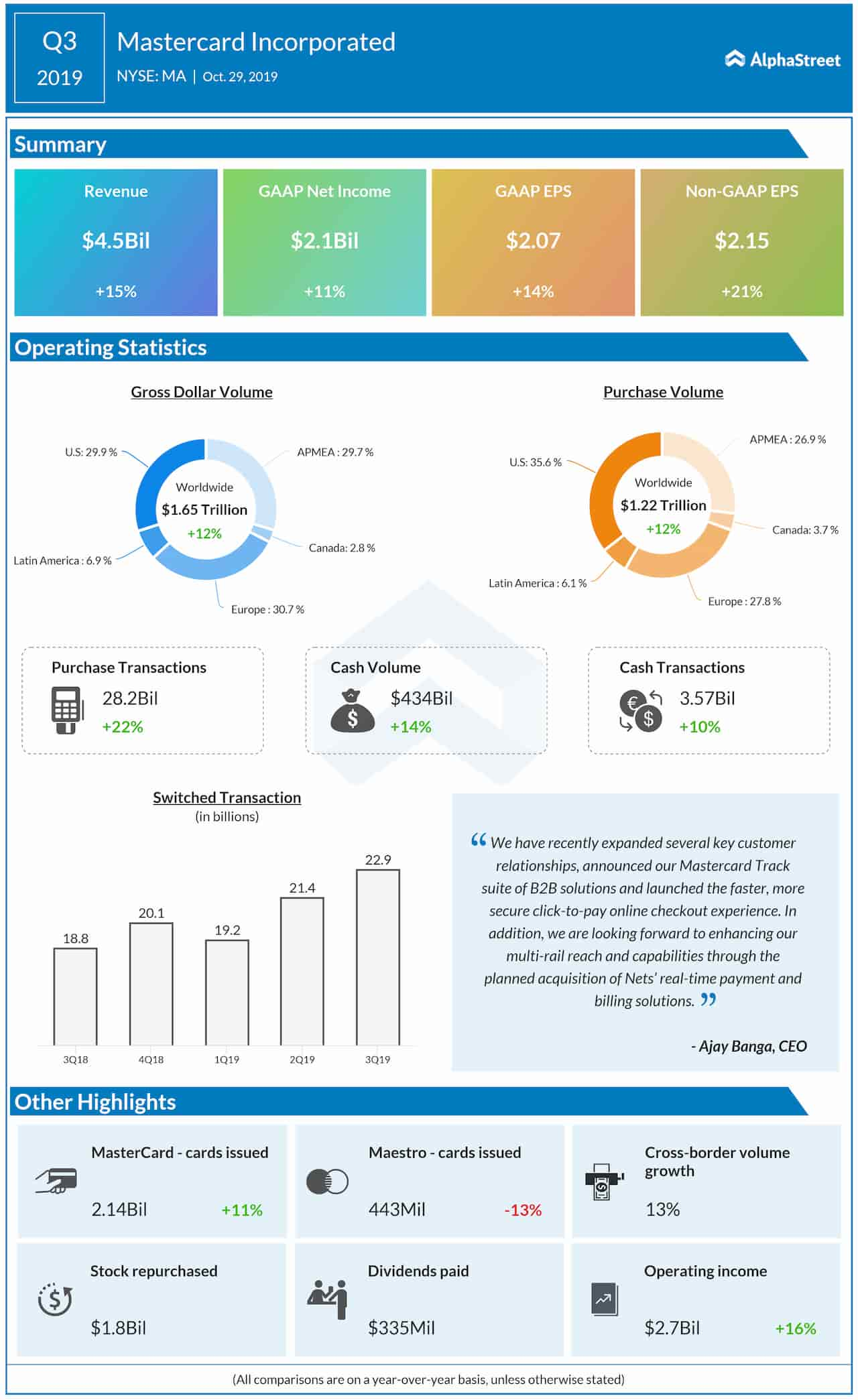

Third-quarter revenues increased 15% annually to $4.5 billion and surpassed the forecast. The top-line growth was spurred by an 20% increase in switched transactions and a sharp increase in cross-border volumes.

Growth Drivers

Adding to the top-line growth, gross dollar volume rose 14% during the quarter, while purchase volume moved up 15%. The positive factors were partially offset by promotional offers such as rebates and incentives, pursuant to fresh and renewed agreements and volume growth. The company’s partners had issued 2.6 billion Mastercard and Maestro-branded cards as of September 2019.

Also see: American Express tops Q3 earnings view

Adjusted earnings advanced to $2.15 per share from $1.78 per share in the third quarter of 2018. Earnings also came in above analysts’ forecast. Reported profit moved up to $2.1 billion or $2.07 per share from $1.9 billion or $1.82 per share a year earlier.

Stock Buyback

During the quarter, the company repurchased around 6.4 million shares for $1.8 billion and paid $335 million in dividends.

CEO Ajay Banga said, “We have recently expanded several key customer relationships, announced our Mastercard Track suite of B2B solutions and launched the faster, more secure click-to-pay online checkout experience. In addition, we are looking forward to enhancing our multi-rail reach and capabilities through the planned acquisition of Nets’ real-time payment and billing solutions.”

Competition

Mastercard’s competitor Visa (NYSE: V) reported Q4 2019 earnings results last week, beating both revenue and profit expectations.

Shares of Mastercard have gained 28% so far this year. The stock has a strong Buy rating and the average price target is $317.31. It moved up during Tuesday’s pre-market trading after the company reported the quarterly results.