Shares of McCormick & Company Inc. (NYSE: MKC) fell over 8% on Tuesday, following the announcement of its earnings results for the third quarter of 2023. While earnings matched estimates, sales fell short of expectations. The stock has dropped 17% year-to-date. Here are the main takeaways from the report:

Sales miss, earnings in-line

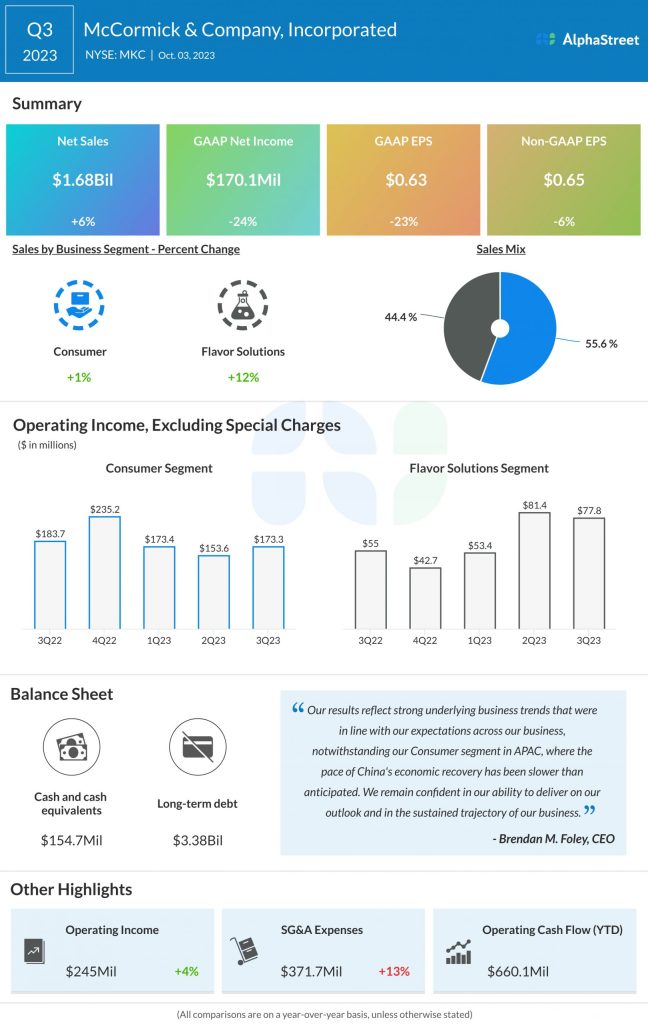

McCormick reported net sales of $1.68 billion for the third quarter of 2023, up 6% from the same period a year ago. The top line growth was mainly driven by pricing but was partly offset by volume and mix decline due to slower economic recovery in China, as well as impacts from business exits and divestitures, and the company’s decision to discontinue low-margin business. Despite the year-over-year growth, sales narrowly missed estimates of $1.70 billion.

GAAP net income fell 24% to $170.1 million, or $0.63 per share, compared to last year. Adjusted EPS fell 6% YoY to $0.65, but was in line with expectations.

Business performance

In the third quarter, sales in the Consumer segment inched up 1% from the year-ago period, driven by pricing. Volumes declined due to softness in China as well as business divestitures and exits. Sales increased across the Americas and Europe, Middle East and Africa (EMEA) regions but the Asia-Pacific (APAC) region saw a 16% decrease due to headwinds from China.

In the Americas, the company saw double-digit growth across its grilling portfolio and also gained share in the mustard, BBQ sauce, and marinades categories. In EMEA, McCormick grew share in herbs, spices, and seasonings. It also saw volume growth in France and the UK.

The Flavor Solutions segment delivered strong performance in Q3 with sales growth of 12%, driven by pricing and volume growth. Sales grew across all regions as well during the quarter.

In the Americas, McCormick saw strong growth in seasonings along with growth in the performance nutrition beverages and health end-markets. The company saw broad-based growth in EMEA, driven by pricing. It also saw strong growth with its quick-service restaurants and packaged food and beverage customers. The spice-maker continues to prune its low-margin business in the region and these actions had an impact on volume growth for the segment during the quarter.

Raised earnings guidance

McCormick expects sales to grow 5-7% in fiscal year 2023, driven mainly by pricing actions. Pricing, along with cost savings, are expected to offset inflationary headwinds. GAAP EPS is expected to range between $2.46-2.51. The company raised its adjusted EPS outlook for the year based on updated expectations with regards to the contribution from its McCormick de Mexico joint venture. It now expects adjusted EPS to be $2.62-2.67 versus the previous range of $2.60-2.65.