Shares of McCormick & Company, Incorporated (NYSE: MKC) stayed green on Wednesday. The stock has gained 4% in the past three months. The flavor giant is scheduled to report its earnings results for the fourth quarter of 2025 on Thursday, January 22, before market open. Here’s a look at what to expect from the earnings report:

Revenue

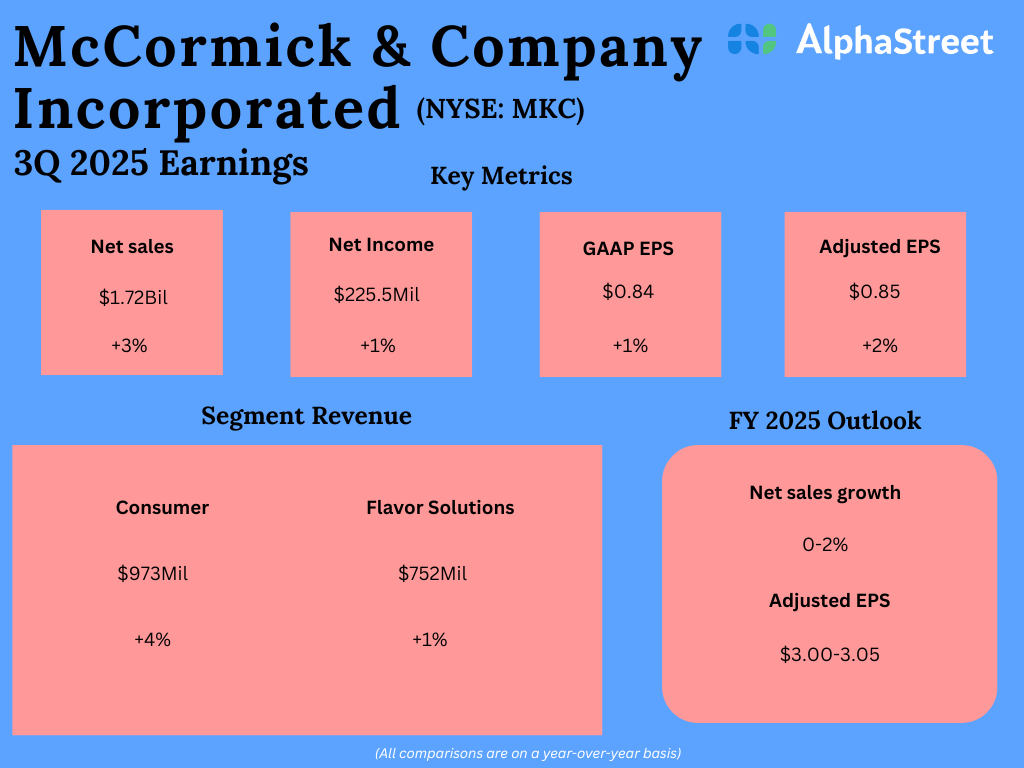

Analysts are projecting revenue of $1.85 billion for McCormick in the fourth quarter of 2025, which indicates a growth of over 2% from the same period a year ago. In the third quarter of 2025, net sales increased 3% year-over-year to $1.72 billion.

Earnings

The consensus target for earnings per share in Q4 2025 is $0.88, which implies an increase of 10% from the prior-year quarter. In Q3 2025, adjusted EPS rose 2% YoY to $0.85.

Points to note

McCormick is operating in an environment where consumers are looking for maximum value on their purchases. They are cooking more meals at home and stretching those meals across a number of occasions. Health and wellness trends remain popular and consumers are preparing healthier, more affordable meals at home while exploring new flavors. These trends are expected to continue fueling demand for the company’s products.

MKC is expected to benefit from continued investment in its brands, expanded distribution and product innovation. In the third quarter, the company saw volume growth with momentum across key markets and categories in the Americas and EMEA. In addition, continued traction in the health and wellness categories is expected to yield gains.

MKC is seeing volume and market share growth in the US and Canada. Within EMEA, it is seeing gains in categories such as spices and seasonings, mustard and hot sauce. The company is also winning business across snack seasonings and better-for-you categories. All these factors are likely to have benefited its performance in the fourth quarter.

However, the condiments maker has been facing headwinds with tough competition in certain categories, soft traffic impacting QSR customers’ volumes, and volume softness in some large CPG customers’ businesses. MKC is working on offsetting these pressures by gaining new customers and expanding into new channels. The company’s margins are also being pressured by rising costs.

Earlier this month, McCormick acquired the controlling interest in McCormick de Mexico, increasing its ownership to 75%. This expanded ownership paves the way for further growth in the Mexican market and expansion in Latin America.