McDonald’s Corporation (NYSE: MCD) has stayed largely unaffected by the inflation-induced dip in consumer spending this year, aided by competitive pricing and effective marketing campaigns. The fast-food giant is currently planning to add hundreds of new units to its restaurant network in the next few years and double sales from the loyalty program by 2027.

Stock Peaks

The burger behemoth’s stock set a new record early this week after gaining consistently over the past two months, all along outperforming the broad market. However, the shares pulled back since then and traded lower in the following sessions. As far as owning the stock is concerned, MCD is unlikely to disappoint long-term investors.

Being a dividend aristocrat, McDonald’s is a favorite among income investors. It has been paying dividends for nearly five decades and offers a better-than-average yield of 2.4% now, after regular hikes. While the valuation is seemingly high, the shares look poised to grow further and go beyond the $300 mark.

Expansion Spree

The restaurant chain in a recent statement said it is targeting around 50,000 restaurants in the next four years, which will be the fastest period of growth in its history. The company looks to expand its loyalty programs from 150 million to 250 million 90-day active users during that period. Complementing those efforts, it is building an advanced digital ecosystem to give customers a more personalized experience, supported by a partnership with Google Cloud that will connect the latest cloud technology and apply generative AI solutions across the company’s global restaurant network.

But in the near term, macro uncertainties and squeezed household budgets might put pressure on the company’s sales. There are concerns that new weight-loss drugs would impact the demand for fast-food items as they reduce people’s appetite for high-fat and high-sugar processed foods. Also, geopolitical issues like the Middle East unrest and the struggling Chinese economy, which is a key market for McDonald’s, could affect sales.

Stable Performance

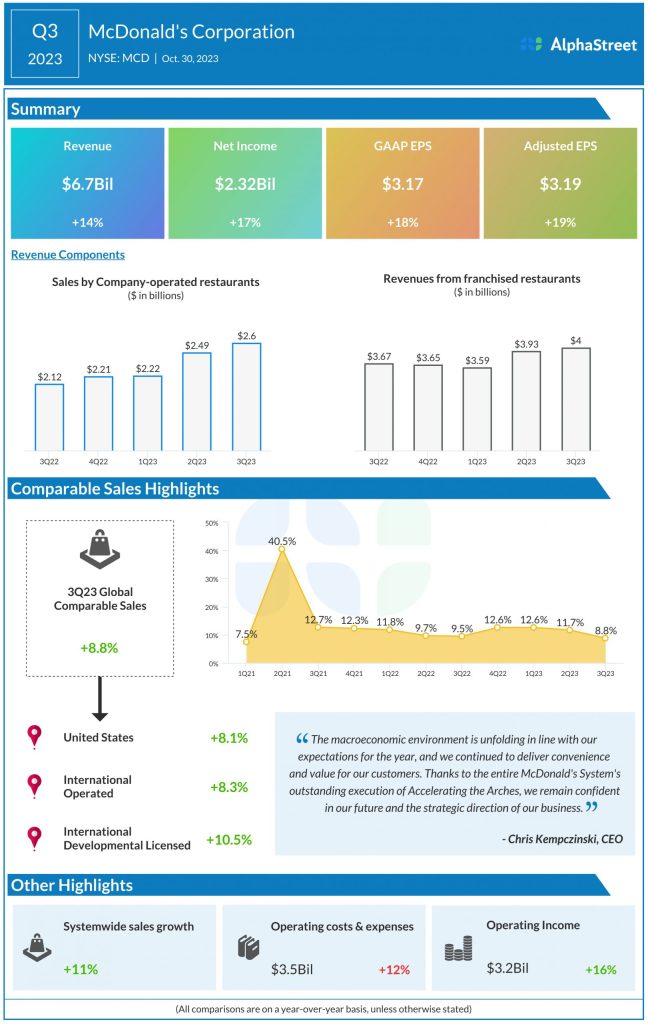

The company has a good track record of delivering better-than-expected quarterly profit and the trend continued in the third quarter. Sales by company-operated stores, a key measure of the strength of the brand, rose 23% annually to $2.6 billion in Q3. Total revenue, including franchise fees, was $6.7 billion, up 14% year-over-year. Adjusted earnings increased 19% annually to $3.19 billion during the three months. Comparable sales were up 8.8%.

McDonald’s CEO Chris Kempczinski said during his interaction with analysts, “As we expected and as we mentioned in prior earnings calls, our top-line growth, while strong across each of our segments and at an elevated level versus historical norms, has continued to moderate. However, we continue to outpace our competitors, thanks to our system’s outstanding execution of our Accelerating the Arches strategy. Over the past year, we’ve been more intentional about sharing and scaling world-class ideas that drive impact globally.”

In 2023, MCD has gained about 6% so far, and it moved above the 52-week average this month. The stock traded down 1% on Friday afternoon after opening the session lower.