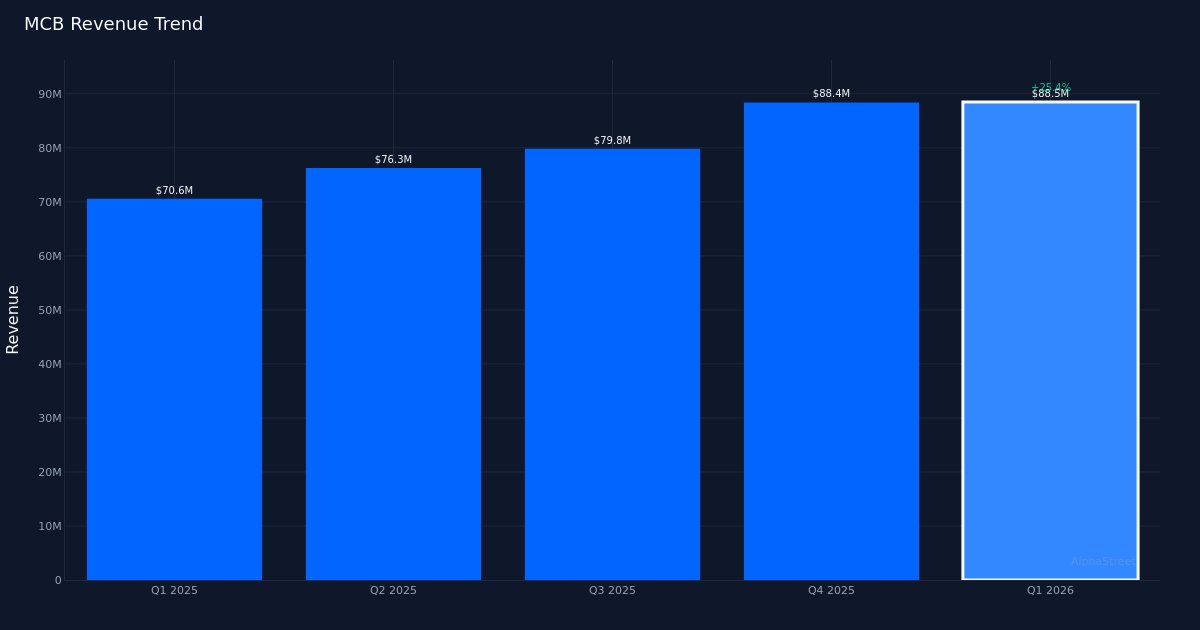

Substantial Beat. Metropolitan Bank Holding Corp. (NYSE:MCB) reported first quarter 2026 diluted earnings of $2.92 per share, crushing the Street’s $2.33 estimate by 25.3% and marking a decisive win for the regional bank. Revenue reached $88.5M for the quarter, while net income came in at $31.4M. The stock traded down 2.7% to $88.85 following the release, an unusual negative reaction to such strong results that likely reflects profit-taking after recent gains or concerns about sustainability of the growth trajectory.

Impressive Growth. The quality of this quarter’s outperformance appears solid, driven by fundamental revenue expansion rather than financial engineering. Year-over-year revenue climbed 25.3% from $70.6M in Q1 2025, while EPS surged 101.4% from $1.45 in the prior-year period. This dramatic earnings growth outpacing revenue gains suggests improving operating leverage and margin expansion across the franchise, pointing to genuine operational momentum rather than cost-cutting alone driving the bottom line.

Core Banking Strength. Net interest income reached $86 million for the quarter, representing the bulk of revenue generation and underscoring the bank’s traditional deposit-and-lending business model remains robust. The loan portfolio stood at $7.05 billion in total loans at quarter end, providing the asset base generating interest income. For a regional bank of Metropolitan’s size, this scale of lending operations demonstrates meaningful market presence and the capacity to sustain growth through its core intermediation activities.

Analyst Support. Wall Street maintains a favorable stance on Metropolitan Bank, with consensus breaking down to 4 buy ratings and 1 hold, while no analysts recommend selling shares. This bullish tilt from the sell-side community suggests confidence in management’s strategy and the bank’s positioning within competitive regional markets, though the hold rating indicates at least one analyst sees valuation or execution risks tempering enthusiasm at current levels.

Market Disconnect. The 2.7% decline in shares despite the significant earnings beat creates an interesting setup for investors. Either the market is signaling skepticism about Metropolitan’s ability to repeat this performance, or technical factors are overwhelming fundamentals in the near term.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.