AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street expects modest year-over-year contraction. Analysts project MGIC Investment Corporation will report earnings of $0.74 per share on revenue of $303.1M when the specialty insurance provider releases Q1 2026 results on April 30th. Four analysts cover the stock, with EPS estimates ranging from $0.73 to $0.77 and revenue projections spanning $301.0M to $306.0M. Both consensus figures represent slight declines from the prior-year period.

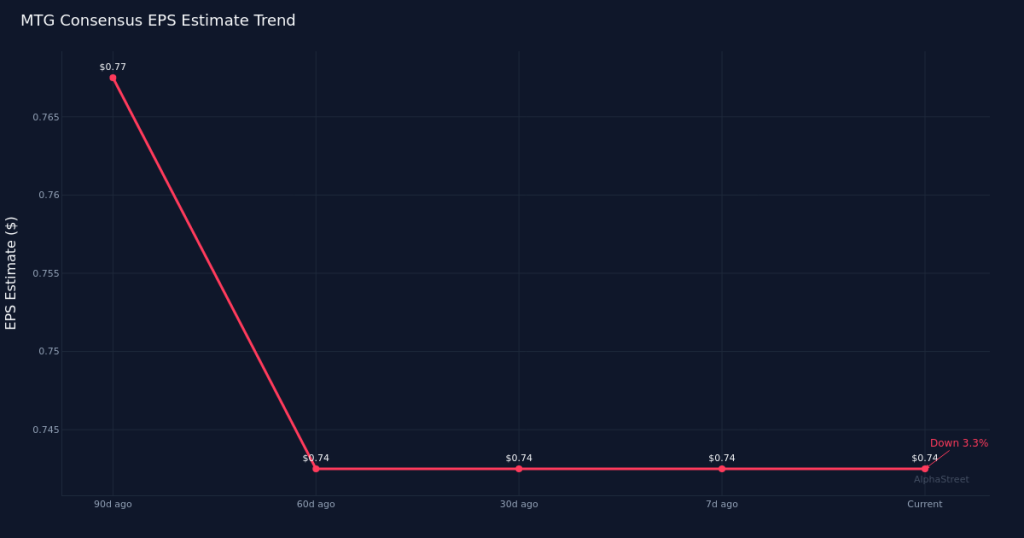

Estimate trajectory shows gradual downward drift. The EPS consensus has held steady over the past month at $0.74, but the 90-day view reveals a downward drift of 3.9% from $0.77. This gradual reduction in analyst expectations suggests mounting headwinds or a more cautious outlook on the mortgage insurance market heading into the first quarter. The downward revision pattern, while modest, signals that analysts have tempered their optimism as they’ve refined their models with more recent data on housing market conditions and underwriting trends.

Year-over-year comparisons point to compression across key metrics. The consensus EPS of $0.74 would represent a 1.3% decline from year-ago earnings of $0.75, while the revenue estimate of $303.1M implies a 1.0% contraction from Q1 2025’s $306.2M. The parallel suggests revenue and profitability are moving in lockstep, a notable shift for a company that generated net income of $185.2M on a net margin of 60.5% in the prior-year quarter. Those profitability figures underscore the highly profitable nature of the mortgage insurance business model when underwriting discipline and favorable loss experience converge, making even modest revenue declines worth monitoring for their potential impact on margin sustainability.

Insurance market dynamics drive performance variability. As a specialty insurer focused on mortgage guaranty insurance, MGIC’s results are heavily influenced by new insurance written, persistency rates on existing policies, premium yields, and loss development trends. The housing market environment—including home price appreciation, refinancing activity, and purchase origination volumes—directly impacts both top-line growth and the quality of the insured portfolio. Any shifts in delinquency rates or claim severity would materially affect loss reserves and ultimately net margin performance. The company’s ability to maintain pricing discipline while growing or defending market share in a competitive landscape remains central to its earnings trajectory.

Margin performance warrants close attention. The year-ago net margin of 60.5% reflects the capital-light, fee-based economics of mortgage insurance once policies are written and loss reserves are adequately established. Whether MGIC can sustain margins near those levels despite the implied revenue decline will hinge on loss ratio trends, operating expense leverage, and investment income generation. Any deterioration in credit performance within the insured portfolio or elevated acquisition costs could compress margins, while benign loss experience and operational efficiency gains could support profitability even as premiums moderate.

Analyst conviction appears moderate. With only four analysts providing estimates and a narrow range of opinions—spanning just four cents on EPS and five million dollars on revenue—the coverage universe suggests limited Street attention relative to larger insurance peers. The tight estimate range indicates broad agreement on near-term fundamentals, leaving less room for dramatic surprises but also offering limited visibility into divergent bull or bear cases that might emerge from the print.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.