Micron Technology Inc. (NASDAQ: MU), a market leader in memory and flash storage chips, emerged from a losing streak in the most recent quarter and reported a profit. The recovery is expected to continue in the second half, aided by a better-than-expected rebound in memory chip demand. The chipmaker is scheduled to release third-quarter results on Wednesday after regular market hours.

Interestingly, Micron’s stock has not been materially affected by the recent downturn in its financial performance. In a testament to the tech firm’s strong fundamentals and investors’ confidence in the resilience of the business, the stock price nearly doubled in the past six months and hit an all-time high recently. The company’s AI-driven growth prospects and increased investments in capacity expansion make the stock a good investment option.

Q3 Report on Tap

Micron is expected to post adjusted earnings of $0.51 per share, on average, when it unveils the third-quarter report on Wednesday, June 26, at 4:05 pm ET. That represents an improvement from the prior-year period when the company incurred a loss of $1.43 per share, excluding special items. The positive forecast reflects an estimated surge in revenues to $6.66 billion. Micron executives are looking for an adjusted profit of about $0.45 per share and revenues of approximately $6.60 billion for the third quarter.

Like most chipmakers, Micron is benefiting from the widespread adoption of artificial intelligence chips and looks poised to ride the AI boom by tapping into emerging opportunities, such as the shift to large data centers that power AI applications. Improving market conditions, driven by strong AI service demand and a more balanced supply-demand balance, are providing chipmakers with significant pricing advantages. Micron’s dominance in high-bandwidth memory solutions gives it an edge over peers since the technology enables high-speed data transfer which is crucial for AI servers.

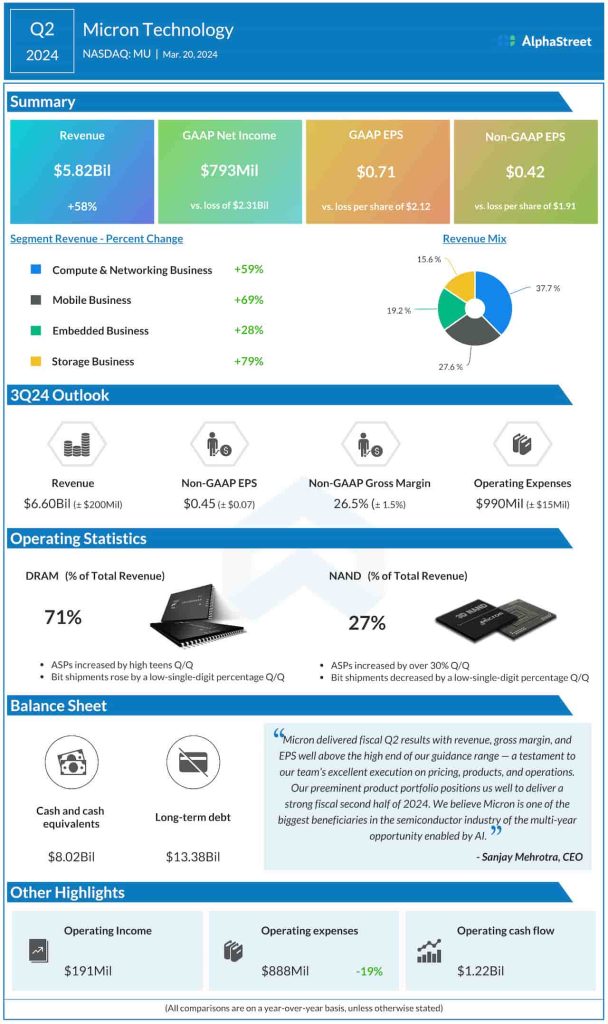

From Micron’s Q2 2024 earnings call:

“We expect DRAM and NAND pricing levels to increase further throughout calendar year 2024 and expect record revenue and much-improved profitability now in fiscal year 2025. Micron is at the forefront of ramping the industry’s most advanced technology nodes in both DRAM and NAND. Reinforcing our leadership position, over three-quarters of our DRAM bits are now on leading-edge 1-alpha and 1-beta nodes, and over 90% of our NAND bits are on 176-layer and 232-layer nodes.”

Financials

Indicating a consistent improvement in the company’s financial performance, quarterly numbers beat estimates in the trailing four quarters. In the second quarter of 2024, the company generated profit for the first time in about one-and-a-half years – adjusted earnings of $0.42 per share vs. a loss of $1.91 per share in Q2 2023. The company delivered a positive operating margin well ahead of expectations. The recovery was driven by a 58% jump in Q2 revenue to $5.82 billion, with strong contributions from all four operating segments. The bottom line also benefited from a 19% drop in operating expenses due to continued cost-cutting efforts. For Q3, the management predicts a year-over-year decline in expenses to around $990 million.

Micron’s shares have mostly stayed above their 52-week average this year. MU started the week higher and traded up 1% Monday afternoon. It has gained 28% in the past three months alone.