Micron Technology Inc. (NASDAQ: MU) is one of the worst affected by the global semiconductor downturn and chip shortage, with the recent ban in China adding to the company’s troubles. The market will be closely following Micron’s upcoming earnings, looking for cues on its financial health.

The Boise-headquartered company’s stock stayed above its 52-week average in recent weeks despite high volatility, but far below the all-time highs of last January. The stock is up 30% since the beginning of 2023. The current slowdown looks temporary since it is linked to the ban imposed on Micron’s products by the Chinese government to some extent. The tech firm’s long-term prospects remain intact, and the valuation is reasonable from an investment perspective.

A Rough Patch

Besides cyclical factors, Micron’s business is also impacted by the post-COVID slump in the PC market, softening of the 5G upgrade cycle, and a slowdown in smartphone sales. While the challenges will likely persist in the remainder of the year, Micron bets on the recent demand recovery and improvements in the supply chain to get back on track.

Meanwhile, the company has revealed plans to invest in its chip packaging facility in the Chinese city of Xian, a move that is expected to help in growing its market share in that country. The announcement comes on the heels of Chinese regulators putting a ban on Micron’s network and infrastructure-related chips for failing a security review.

Weak Outlook

Micron is scheduled to release third-quarter 2023 results on June 28, at 4:00 pm ET. Wall Street expects that the company would report a net loss of $1.57 per share, compared to a profit of $2.59 per share in the year-ago quarter. It is estimated that May-quarter revenues dropped a dismal 57% year-over-year to $3.67 billion. The forecast is broadly in line with the guidance issued by the management a few months ago.

From Micron’s Q2 2023 earnings call:

“We are carefully managing our business to weather this industry downturn, preserving our technology and product portfolio competitiveness and manufacturing capabilities. Micron is the leader in DRAM and NAND process technology and one of only a handful of leading-edge semiconductor manufacturers in the world. Our team continues to drive new breakthroughs for our customers. Memory and storage are at the heart of systems and solutions that fuel the global economic engine, drive new efficiencies, create higher productivity, and split advances that make life better for people around the world.”

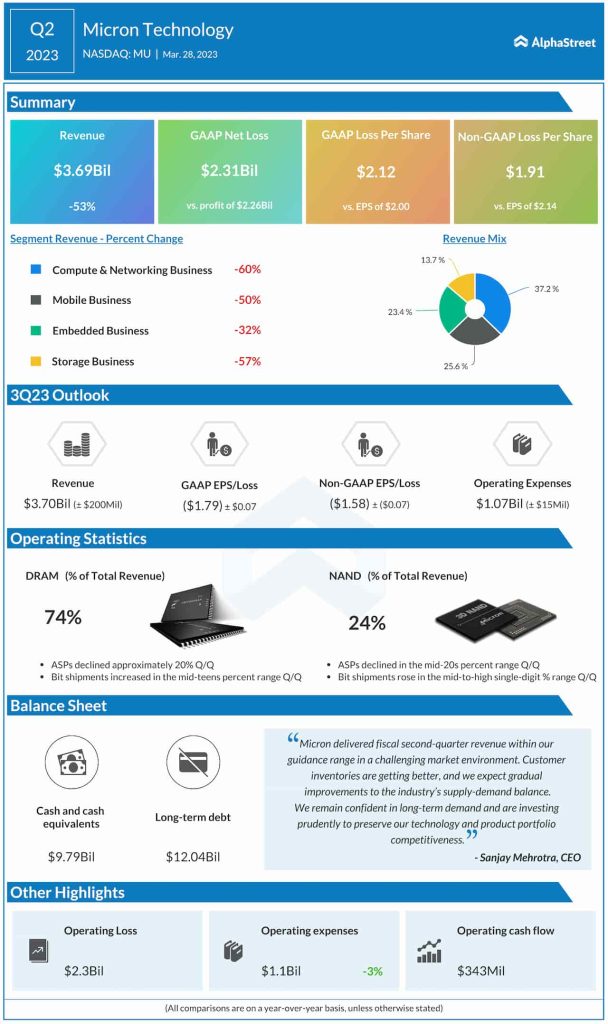

Q2 Results

The estimates point to a repeat of the weak performance seen in the previous two quarters when the company slipped to a loss hurt by sharp declines in revenues. The bottom line also fell short of expectations on each occasion, after beating regularly in every quarter for over six years. In the second quarter, there was broad-based weakness and all four business divisions contracted sharply. As a result, revenues plunged to $3.69 billion from $4.09 billion last year, representing a 53% decrease. Loss per share, on an adjusted basis, was $1.91, compared to earnings of $2.14 per share in Q2 2022.

MU’s performance ahead of next week’s earnings has not been very impressive. The stock, which maintained a downtrend for most of this month, traded lower on Friday afternoon.