Last week, the better-than-expected fourth-quarter results came as a relief to troubled chipmaker Micron Technology Inc. (NASDAQ: MU), which has been going through a rough patch due to supply-related issues and a ban on its products in the Chinese market.

Despite the company’s unimpressive performance in the recent past, investor sentiment towards the stock has remained positive and it stayed above the 52-week average most of the year. However, the shares slipped following the latest earnings release despite the results beating estimates. The selloff reflects investors’ concerns over the management’s cautious guidance.

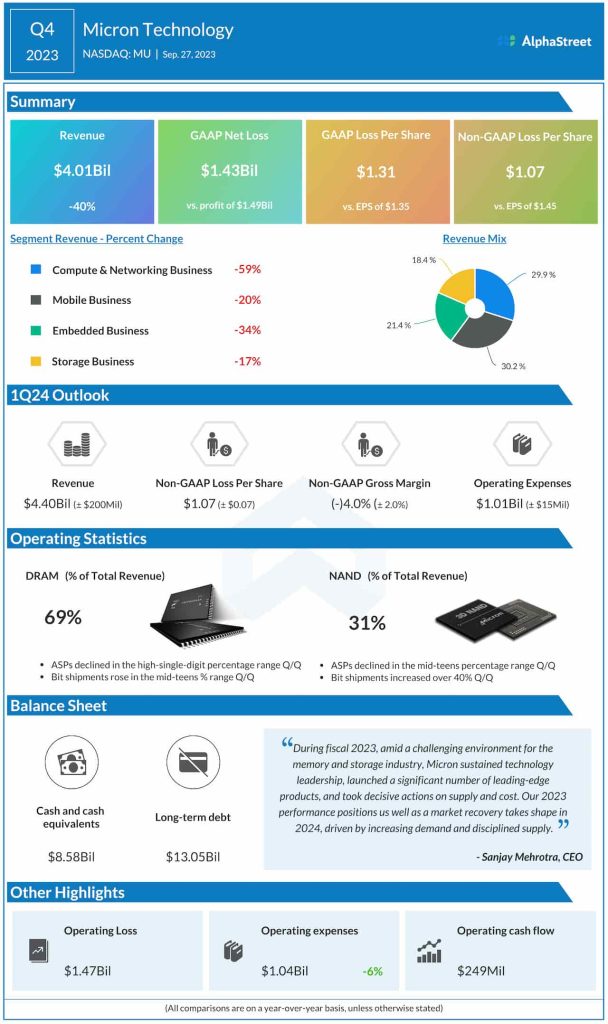

In the fourth quarter, the bottom line exceeded estimates, marking the second consecutive beat since slipping to negative territory a year ago. The company incurred a loss of $1.07 per share in the final three months of fiscal 2023, on an adjusted basis, compared to a loss of $1.45 per share last year. The weakness can be attributed to a double-digit fall in revenues across all four divisions of the business, namely Compute & Networking Business, Mobile Business, Embedded Business, and Storage Business. As a result, total revenues fell a dismal 40% year-over-year to $4.01 billion.

Guidance Misses

Indicating that the current weakness would extend into the first half of 2024, the management predicts an adjusted loss per share of around $1.07 per share for the first quarter. It is looking for revenues of approximately $4.40 billion and operating expenses of around $1 billion for the November quarter. The guidance is below analysts’ estimates.

Meanwhile, Micron’s leadership has exuded confidence that the downturn is over and the company is headed for a turnaround. There is speculation that profitability would improve going forward, aided by better pricing and improvements in the demand-supply environment. Since last year, the tech firm has been working to reduce costs and streamline capital expenditure to strengthen liquidity. The second half of fiscal 2024 is expected to be better in terms of demand and margin performance. The company bets on tailwinds like demand growth, industry-wide supply reductions, and improvements in customer inventory to get back on track.

In Recovery Mode?

The management is of the view that pricing bottomed in the fourth quarter, and it sees a recovery in pricing in the coming months. But the impact of recent headwinds will likely linger, which means it would take some time for the company to return to normal levels of profitability. Free cash flow is seen staying in the negative territory for most of the first half, before improving in the back half of the year.

From Micron’s Q4 2023 earnings call:

“Inventory levels are normal across most customers in the automotive market as well. Datacenter customer inventory is also improving and will likely normalize in early calendar 2024. Consequently, we see demand continuing to strengthen, which has led to an inflection in pricing. Some customers have made strategic purchases in DRAM and NAND to take advantage of unsustainably low pricing as the market begins its recovery. In Data Center, traditional server demand remains lackluster while demand for AI servers has been strong.”

Micron’s stock, which has remained almost stable in recent weeks, closed the last session lower and lost further in the after-hours. It has gained 19% so far this year.