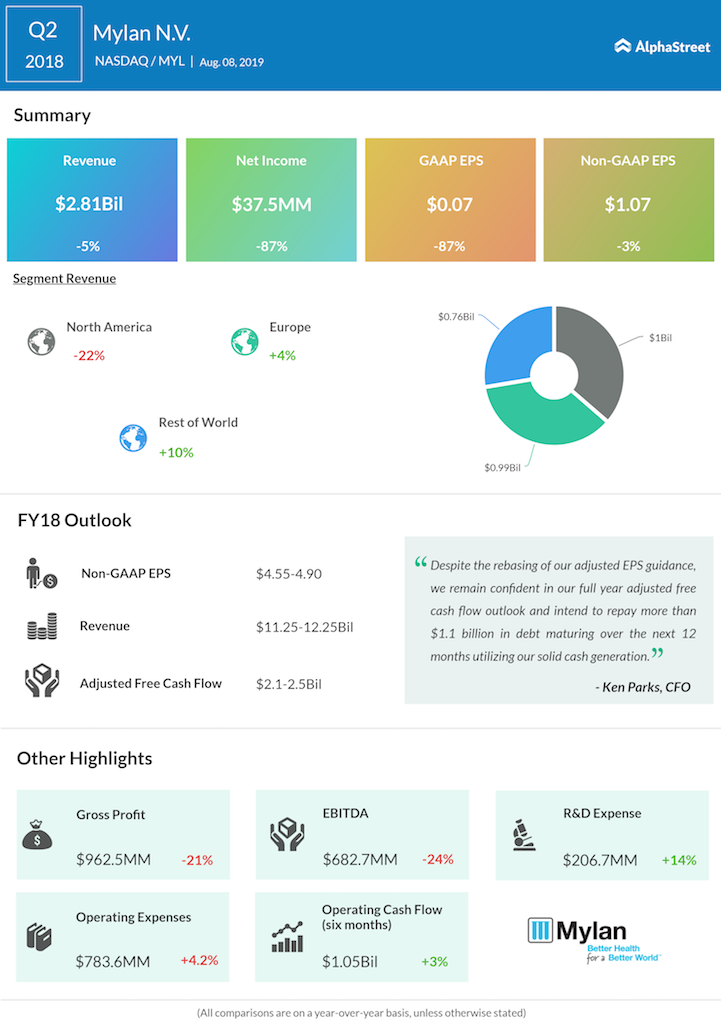

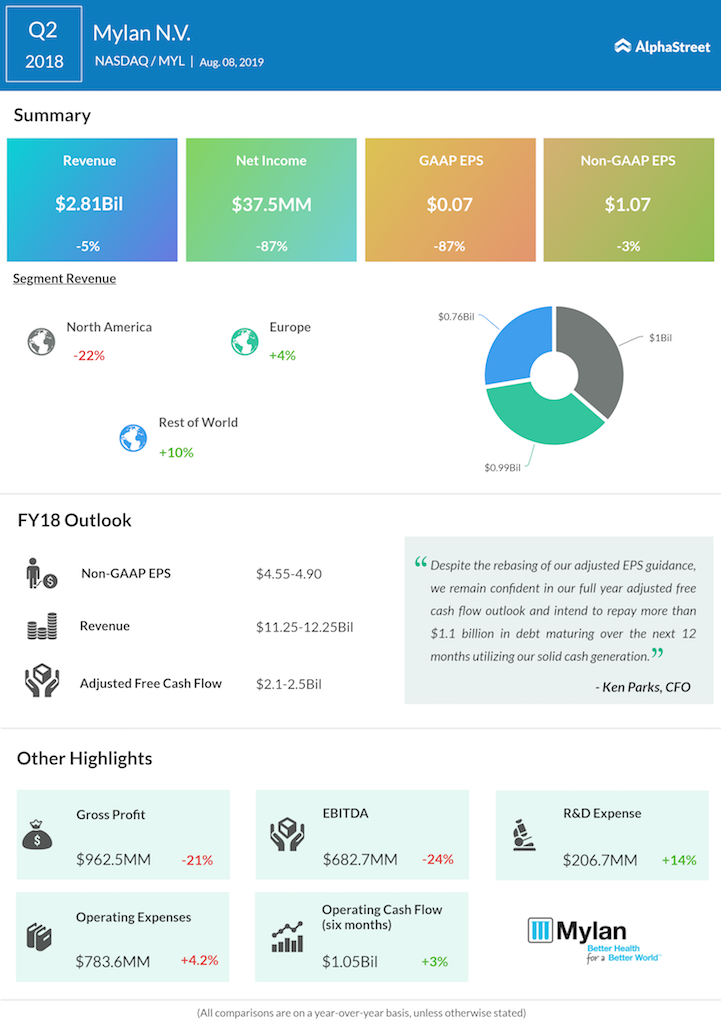

Mylan NV (MYL) missed analyst expectations on revenue and earnings for the second quarter of 2018. The company’s total revenues dropped 5% to $2.81 billion from last year, mainly due to a decline in existing-products sales. The drop in sales from existing products was partially offset by new product launches.

Mylan shares dropped 5% during premarket trading following the announcement.

Total revenues include net sales and other revenues, of which net sales fell 6% while other revenues improved to $52.8 million from $35.7 million last year.

On a GAAP basis, net income fell 87% to $37.5 million or $0.07 per share from the same period last year. Adjusted net income came in at $551.5 million or $1.07 per share for the quarter.

Mylan revised its guidance for the full year of 2018. The company now expects total revenues to come in at $11.25 billion to $12.25 billion, which is essentially flat at the midpoint versus full-year 2017. Adjusted EPS is expected to be $4.55 to $4.90, an increase of 4% at the midpoint when compared to last year. Adjusted free cash flow is expected to be $2.1 billion to $2.5 billion.

Net sales in North America declined mainly due to lower volumes on existing products, including EpiPen. The Europe and Rest of World segments posted sales increases with Rest of World benefiting from new product sales, particularly from the anti-retroviral therapy franchise.

During the quarter, Mylan faced an FDA inspection at its Morgantown facility and the company is making the required improvements at the plant. This, along with job cuts and product discontinuations, led to production and supply issues which affected quarterly results.

The company’s board of directors is said to be looking at strategic alternatives to deal with lower prices and volumes for many of its products in the US market.