Shares of Netflix Inc. (NASDAQ: NFLX) soared 16% on Thursday, continuing its rally from the day before when the company delivered strong results for the third quarter of 2023. The stock has gained 36% year-to-date. The Street appears to be impressed with Netflix’s revenue and subscriber growth in the quarter as well as the progress on its recent initiatives. Here are a few notable points from the Q3 earnings report:

Revenue and profit growth

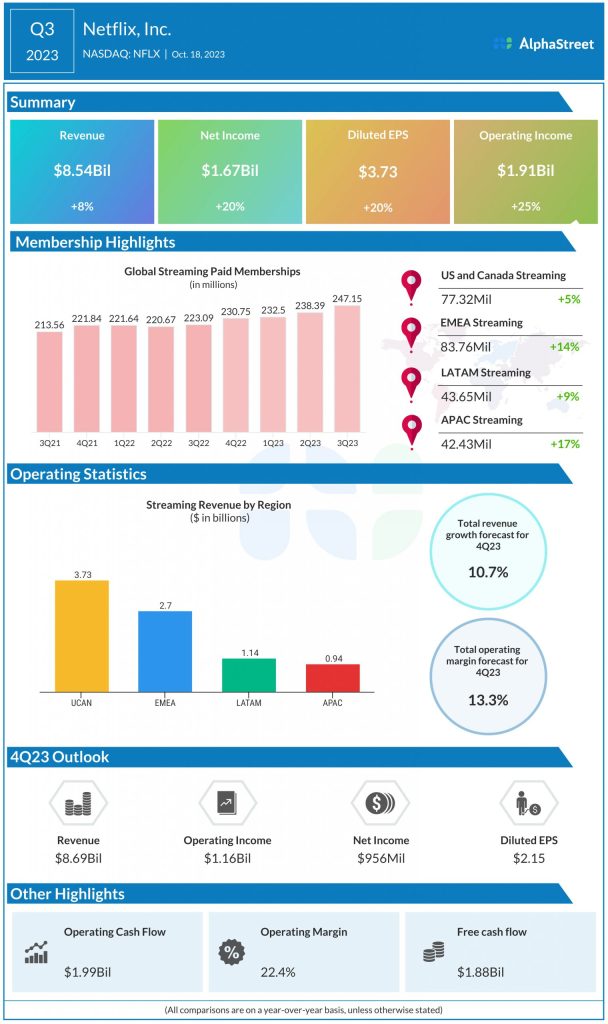

Netflix’s revenue increased nearly 8% year-over-year to $8.54 billion in the third quarter of 2023. The top line exceeded expectations and saw the highest growth rate thus far this year. The company is forecasting revenue to grow nearly 11% to $8.7 billion in the fourth quarter of 2023.

Net income rose 20% YoY to $1.67 billion, or $3.73 per share, in Q3, surpassing projections. Netflix expects net income of $956 million, or $2.15 per share, for Q4 2023 which compares to income of $55 million, or $0.12 per share, reported in the same period a year ago.

Subscriber growth

Netflix ended the third quarter with 247.15 million subscribers, reflecting a YoY growth of around 11%. The company added 8.76 million subscribers during the quarter, which was the highest thus far this year. Paid net additions for the fourth quarter of 2023 are expected to be similar to the third quarter.

Price increases

Netflix has hiked its prices in the US, UK and France. In the US, the company’s basic plan will now cost $11.99 and its premium plan will cost $22.99. Its ad-supported tier and its standard plan will remain the same at $6.99 and $15.49, respectively. The ads and standard plans will remain unchanged in the UK and France as well while the others will see hikes. This move is expected to help boost average revenue per membership.

Paid sharing

Netflix is making good progress in rolling out paid sharing across all its regions. The cancel reaction remains lower than expected and it is seeing healthy retention among borrower households that are converting into full paying memberships. The streaming giant stated in its report that it is revenue positive in every region when accounting for additional spin-off accounts and extra members, churn and changes to plan mix.