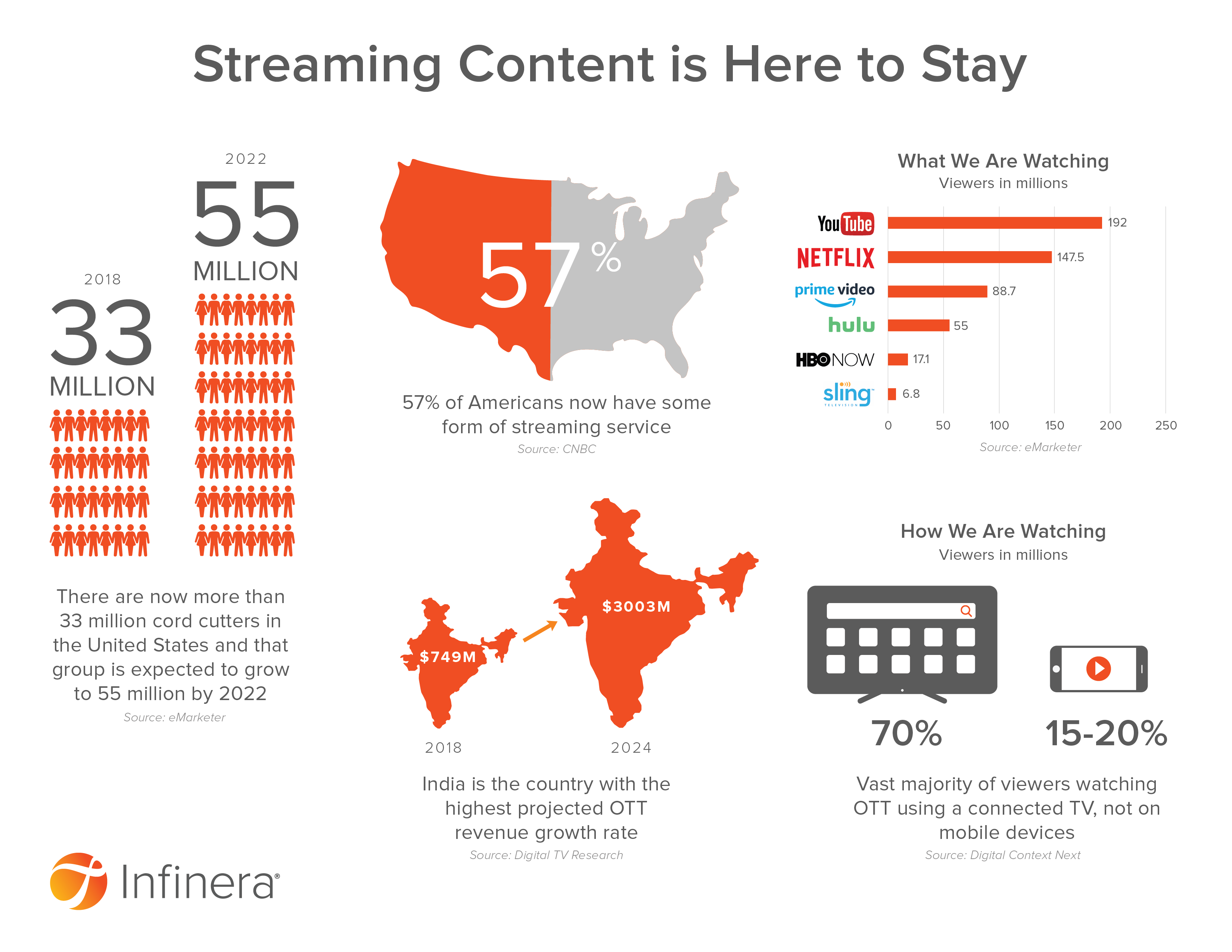

There has been a lot of buzz around Netflix’s (NYSE: NFLX) third-quarter earnings results that released on Wednesday. While some have raised concerns regarding the impact of the upcoming competition on Netflix and its user growth, I continue to be fairly optimistic.

Firstly, in terms of subscriber growth, while the Q3 figure of 6.8 million came in slightly below the company’s forecast of 7 million, it was a considerable improvement over the Q2, when it reported just 2.7 million versus the 5 million forecast.

Paid net adds in the US of 0.5 million have also not matched forecasts of 0.8 million. The company has attributed this slowdown to the recent changes in price and expects modest headwinds to its near-term growth as the competition intensifies.

However, international paid net additions not only rose 23% over the prior-year number but also exceeded internal forecasts. This is a sign of Netflix’s growth prospects outside the US. The company believes there is a large market opportunity to expand its footprint and it has been partnering with local services in countries like India, France, Japan and Mexico to leverage this opportunity.

Secondly, the company has welcomed the rival streaming services from Disney (NYSE: DIS) and Apple (NYSE: AAPL). Although Netflix stated in its shareholder letter that the launch of these services will be noisy and will cause some minor challenges, the streaming giant believes that each player will be unique in terms of their content libraries and rather than take share from each other, they are more likely to edge out linear TV. Much like what cable networks did to broadcast viewing.

There is no doubt that competing with Disney will not be easy considering the vast trove of content it owns but this brings us to the next point – content. Netflix’s growth strategy focuses almost entirely on content. To be exact, original content.

One of the biggest risks Netflix faces is the withdrawal of content from its platform by the owners. To tackle this, the company started the shift to original content and it has showed that this strategy is paying off in terms of viewership and engagement. Stranger Things remains at the forefront of this success with 64 million viewers in the first month for Season 3.

Netflix is investing in original films while also expanding its offerings in foreign languages. Netflix has seen success with its shows in countries like India, Japan and Brazil. The company’s $15 billion content budget gives it meaningful flexibility to pursue this strategy.

Also read: Netflix Q3 2019 Earnings Conference Call Transcript

But the company has not pinned its entire hopes on original content. Netflix has invested a significant amount to acquire the rights to one of the most popular shows in TV history, Seinfeld, which will roll out in 2021. Meanwhile, Netflix also has FRIENDS till the end of this year and it will have The Office throughout next year, which should provide somewhat of a cushion until Seinfeld takes over.

While there will be some challenges like shift in customer preferences and price wars due to the launch of competitive services, once the dust settles, Netflix is very much likely to stand firm.

DISCLAIMER: (This article reflects the opinions of the writer alone and not necessarily that of AlphaStreet)