AlphaStreet Newsdesk powered by AlphaStreet Intelligence

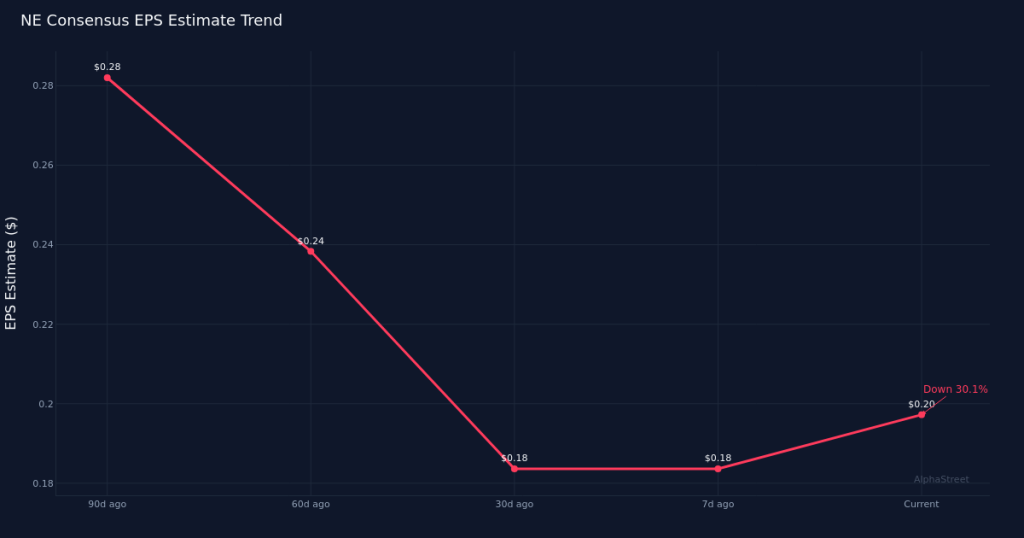

Wall Street expects Noble Corporation plc to report first-quarter earnings of $0.20 per share when the offshore drilling contractor releases results on April 26th. The consensus, drawn from five analysts, calls for revenue of $746.5M. Individual EPS estimates range from $0.15 to $0.23, while revenue forecasts span $726.5M to $773.0M, reflecting a relatively tight band of expectations heading into the print.

Analyst sentiment has diverged sharply depending on the time horizon. Over the past 30 days, EPS estimates have climbed 11.1% from $0.18, suggesting recent improvement in the near-term outlook as analysts digest current market conditions. That positive revision trend stands in stark contrast to the 90-day view: estimates have fallen 28.6% from $0.28 over the past three months. The longer-term downward trajectory signals that analysts have meaningfully reset expectations for Noble’s profitability, likely reflecting changing market dynamics in the offshore drilling sector or adjustments to dayrate and utilization assumptions.

The year-over-year comparison reveals a significant deterioration in both the top and bottom lines. Consensus EPS of $0.20 represents a 23.1% decline from the $0.26 Noble earned in the first quarter of 2025. Revenue expectations of $746.5M similarly trail the year-ago result of $874.5M by 14.6%. A year ago, Noble generated net income of $42.5M on a net margin of 4.9%, establishing a profitability baseline that will be difficult to match given the implied contraction. The narrower profit outlook suggests either pricing pressure on dayrates, lower utilization across the rig fleet, or cost inflation that hasn’t been fully offset by operational efficiency gains.

The offshore drilling market has faced headwinds as the industry digests elevated newbuild deliveries and shifting customer demand patterns. Noble operates a fleet of floating rigs serving deepwater and ultra-deepwater markets globally, and quarter-to-quarter performance typically reflects changes in contract commencements, rig reactivations, and idle time between jobs. While specific operational metrics from the prior quarter are not available, the magnitude of the year-over-year revenue decline points to fewer revenue-earning days, lower average dayrates, or a combination of both factors pressuring financial performance.

Noble’s historical tendency to beat or miss consensus will inform how investors position ahead of the report. The company’s track record of delivering surprises—whether positive or negative—shapes expectations around the likelihood of an in-line print versus a material deviation from the $0.20 consensus. Given the wide swing in estimate revisions over different time periods, any guidance commentary from management will be scrutinized for signals about the sustainability of current market conditions and the trajectory for the remainder of 2026.

Investors should pay close attention to commentary around contract backlog, rig utilization, and customer tendering activity. In the offshore drilling business, leading indicators such as the number of rigs under contract, average contract duration, and the pipeline of new awards provide visibility into future revenue streams. Any discussion of operating leverage—how incremental revenue flows through to the bottom line—will be critical given the margin pressure implied by the year-over-year comparisons. Management’s view on fleet optimization, including decisions around cold-stacked rigs or capital allocation for upgrades, will also factor into the investment narrative.

The balance between near-term estimate momentum and longer-term downward revisions creates an uncertain setup. While the recent uptick in estimates suggests some stabilization, the broader reset over 90 days indicates analysts remain cautious about sustained improvement. How Noble navigates the current market environment—balancing fleet deployment, cost discipline, and customer relationships—will determine whether the company can stabilize margins and return to a growth trajectory in subsequent quarters.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.