Oil States International, Inc. (NYSE: OIS) reported fourth-quarter results for the period ended December 31, 2025. The company posted consolidated revenues of $178.5 million and a net loss of $117.2 million, which included one-time asset impairment and restructuring charges. Adjusted EBITDA for the quarter was $22.8 million. Market capitalization: $371.6 million.

Latest Quarterly Results (Q4 2025)

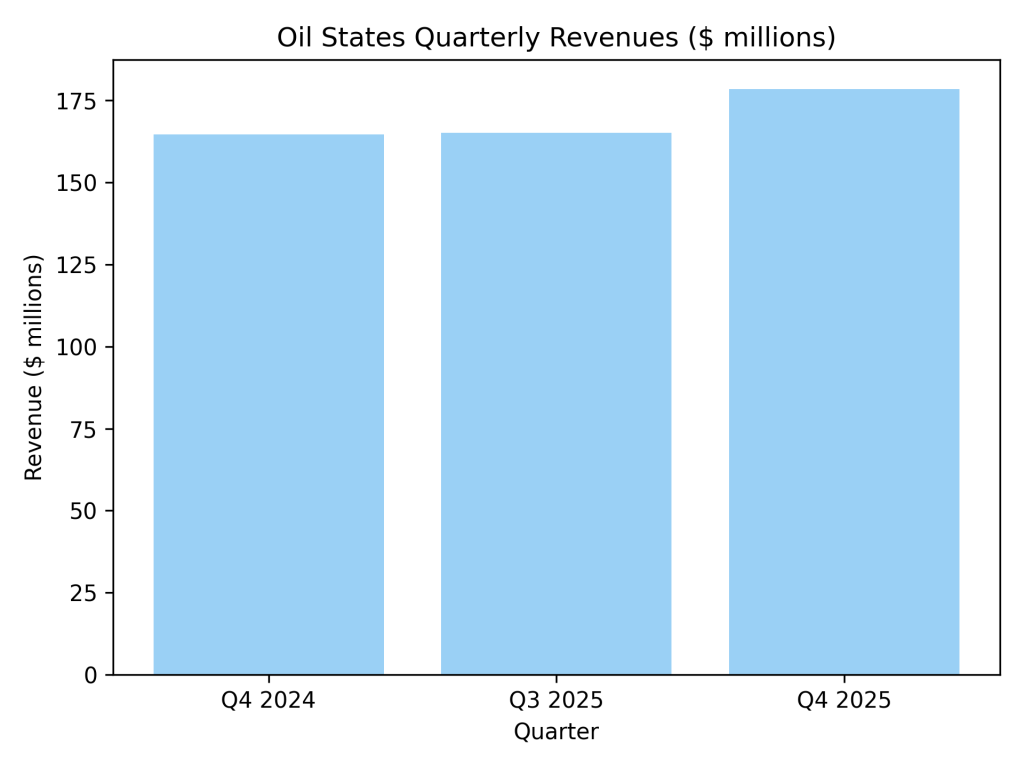

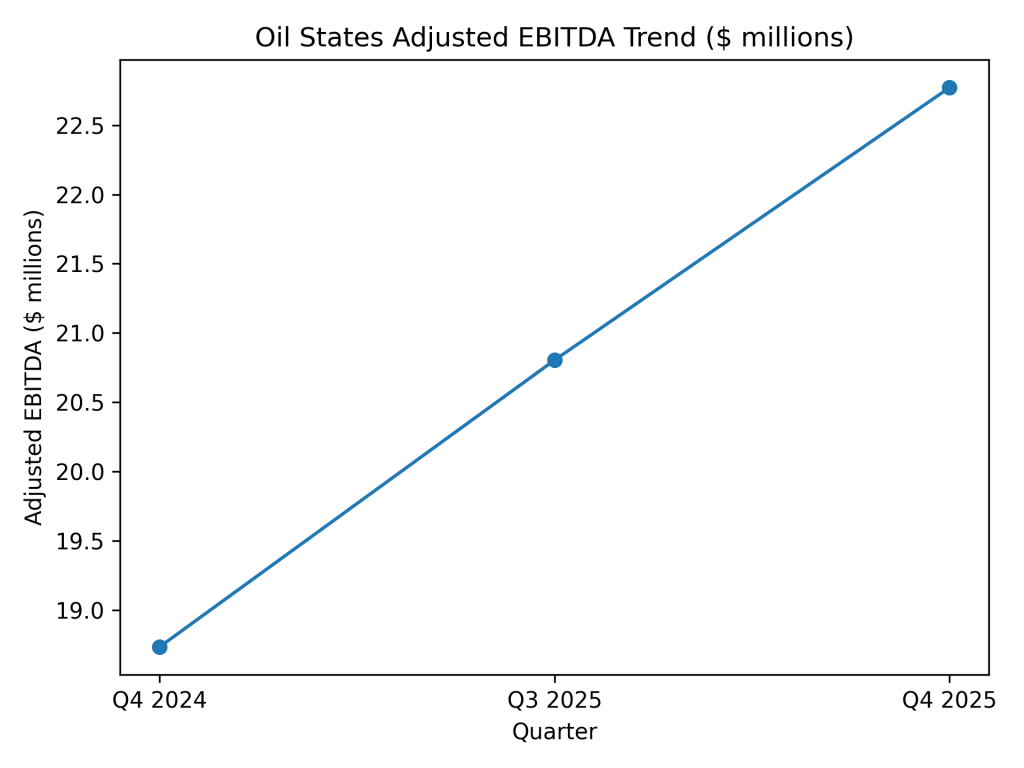

Latest quarterly results (Q4 2025): Consolidated revenue was $178.5 million, up 8% year-on-year from $164.6 million in Q4 2024. Net loss for the quarter was $117.2 million versus net income of $15.2 million in Q4 2024. Adjusted EBITDA was $22.8 million, compared with $18.7 million a year earlier. Adjusted net income, excluding charges and credits, was $7.5 million versus $5.5 million in Q4 2024.

Segment Highlights

Offshore Manufactured Products revenue was $123.3 million. Completion and Production Services revenue was $23.1 million. Downhole Technologies’ revenue was $32.1 million.

Year-over-Year Comparison

| Metric | Q4 2025 | Q4 2024 | YoY change |

| Revenue (Q4) | $178.5M | $164.6M | +8% |

| Net income (loss) (Q4) | ($117.2M) | $15.2M | n.m. |

| Adjusted EBITDA (Q4) | $22.8M | $18.7M | +22% |

| Adjusted net income excl. charges (Q4) | $7.5M | $5.5M | +36% |

Financial Trends

Operating Performance — Quarterly revenue trend

Operating Performance — Adjusted EBITDA trend

Full-Year Results Context

For the year ended December 31, 2025, consolidated revenue totaled $669.0 million compared with $692.6 million in 2024, reflecting a directional contraction year-on-year. Adjusted EBITDA for full-year 2025 was $83.4 million versus $77.0 million in 2024.

Business & Operations Update

During 2025 the company continued to shift emphasis toward offshore and international markets. Backlog in Offshore Manufactured Products reached $435 million as of December 31, 2025. Management reported new contract awards, including military and long-term product contracts, and deployment of new technology platforms such as managed pressure drilling systems and the Low Impact Workover Package.

M&A or Strategic Moves

No announced acquisitions were disclosed in the quarter. Management used cash generated during the quarter to retire $50 million of convertible senior notes and to support balance sheet flexibility.

Equity Analyst Commentary

Institutional summaries cited by management referenced the company’s improved adjusted EBITDA and elevated backlog. Analyst commentary referenced the company’s restructuring actions and the one-time charges recorded in the quarter.

Guidance & Outlook — what to watch for

Prior guidance called for sequential revenue growth of 8%–13% and adjusted EBITDA of $21 million–$22 million for the fourth quarter. Key items to watch include backlog conversion, progress on U.S. land restructuring actions, and cash-flow conversion from adjusted EBITDA.

Performance Summary

Revenues rose year-on-year; the reported GAAP net loss reflected large non-cash and restructuring charges; adjusted metrics showed sequential and year-over-year improvement. Backlog reached a multi-year high, and cash generation funded debt retirement.