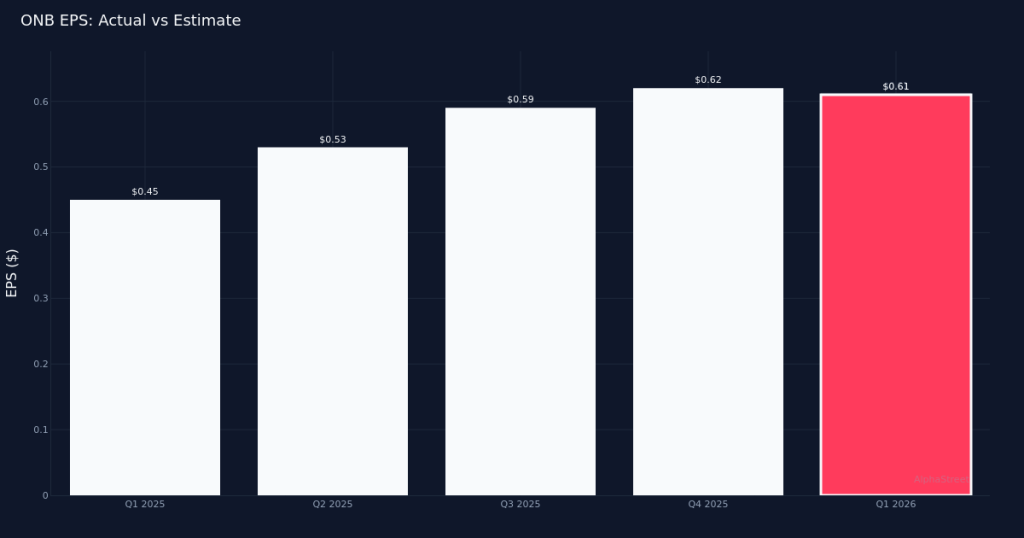

In-Line Performance. Old National Bancorp (NASDAQ:ONB) delivered Q1 2026 adjusted EPS of $0.61, meeting analyst expectations of $0.61, though shares retreated 2.0% to $23.77 as investors digested the results. The regional bank generated $694.9M in revenue for the quarter, marking a substantial 44.6% increase from the $480.4M recorded in Q1 2025. Net income reached $237.7M for the quarter, underscoring solid profitability despite a challenging environment for regional banks navigating interest rate dynamics and competitive deposit pressures.

Revenue-Driven Expansion. The quality of Old National’s performance warrants particular attention, as the sharp year-over-year revenue growth of 44.6% suggests meaningful momentum in the bank’s core business operations rather than reliance on aggressive cost-cutting measures. This revenue expansion likely reflects some combination of loan growth, deposit pricing management, and potentially contributions from acquisitions that have closed over the past year. For a regional bank operating in the Midwest, this magnitude of top-line growth indicates successful market share gains and effective execution on strategic priorities.

Balance Sheet Metrics. Total deposits stood at $55.67B for the quarter, providing the bank with a substantial funding base to support lending activities and future growth. The company operated 49,731,844,000 total loans at quarter end, reflecting the bank’s extensive lending franchise across its geographic footprint. The relationship between deposit gathering and loan deployment remains critical for Old National’s net interest margin and overall profitability, particularly as the Federal Reserve’s monetary policy continues to influence the banking sector’s operating environment.

Market Sentiment. The modest 2.0% decline in shares following the earnings release suggests investors may have been anticipating a modest beat rather than an in-line result, or could be reflecting broader concerns about the regional banking sector’s outlook. Wall Street maintains a generally constructive view on Old National, with analyst consensus standing at 8 buy ratings, 5 hold ratings, and 0 sell ratings. This relatively bullish stance from the sell-side community indicates confidence in management’s strategic direction and the bank’s competitive positioning within its markets.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.