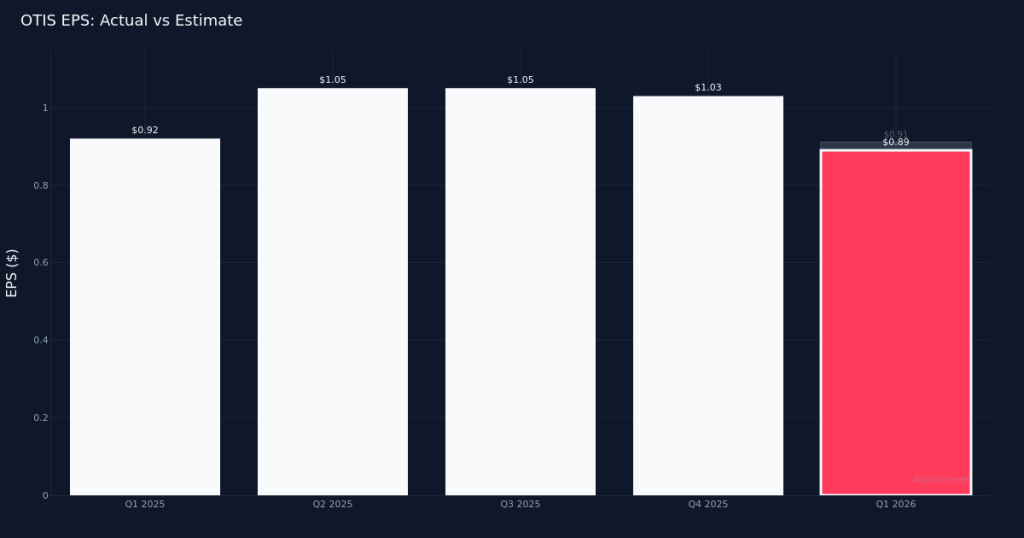

OTIS|EPS $0.89 vs $0.91 est (-2.2%)|Rev $3.57B|Net Income $340.0M

OTIS|EPS $0.89 vs $0.91 est (-2.2%)|Rev $3.57B|Net Income $340.0MSlight miss. Otis Worldwide Corporation (NYSE:OTIS) reported Q1 2026 adjusted earnings of $0.89 per share, falling short of the $0.91 consensus by 2.2%, while revenue of $3.57B climbed 6.0% year-over-year from $3.35B in the prior-year quarter. The modest earnings shortfall comes despite solid top-line momentum, suggesting margin pressures may be crimping profitability in the elevator and escalator giant’s business. Net income reached $340.0M for the quarter as the company maintained its position servicing 2.5M customer units worldwide.

Service strength shines. The standout performance came from Otis’s high-margin Service segment, which generated $2.42B in revenue with an impressive 11.0% year-over-year expansion. This recurring revenue stream remains the crown jewel of the business model, providing stability and cash generation that offsets the more cyclical nature of new equipment installations. However, organic sales growth of just 1.0% for the quarter indicates that currency tailwinds or acquisitions likely contributed meaningfully to the headline revenue growth, raising questions about underlying demand momentum in core markets.

Margin quality questioned. The disconnect between 6.0% revenue growth and the earnings miss suggests operational leverage failed to materialize as expected. With Service growing at double-digit rates—typically the company’s most profitable segment—the earnings shortfall points to either pricing pressures, elevated input costs, or weakness in the New Equipment business dragging on consolidated margins. Management will need to demonstrate tighter cost discipline and pricing power to reassure investors that the growth trajectory can translate into bottom-line expansion.

Guidance offers reassurance. Management maintained its full-year outlook with projected FY 2026 adjusted EPS in the $4.20 to $4.24 range and revenue guidance of $15.10B to $15.30B. At the midpoint, this implies adjusted earnings of $4.22 for the year, suggesting the company expects sequential improvement through the remaining quarters. The steady guidance despite the Q1 miss indicates confidence that first-quarter headwinds are temporary rather than structural, though investors will scrutinize whether management pulls these targets if demand softens.

Market reaction turns negative. Shares fell 2.8% to $76.67 following the release, reflecting investor disappointment with the earnings miss and perhaps concerns about margin trajectory. The sell-side community remains cautiously positioned with 7 buy ratings, 10 holds, and 1 sell, suggesting consensus views the stock as fairly valued at current levels pending clearer evidence of sustainable margin improvement.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.