After a transformative year, PayPal Holdings Inc. (NASDAQ: PYPL) has revealed plans to right-size the business and streamline operations through various initiatives including spending cuts and workforce reduction. The company, a market leader in digital payments, this week issued positive guidance for the current year, forecasting net profit above estimates.

The stock gained after PayPal reported impressive fourth-quarter results on Thursday evening but retreated early in the next session, indicating the market’s mixed reaction. The past two years have been challenging for PYPL, marked by high volatility and a sharp decline in value. When the market suffered a major selloff last year, PayPal was not spared and the impact further weakened the stock that was already going through a rough patch. It has lost about three-quarters of its value since peaking a couple of years ago.

Buy PYPL?

Going by the current trend, the stock seems to be on its way to crossing the $100 mark this year, representing a 28% increase from the current levels. Prospective investors who want to benefit from those gains should consider buying the stock. At the current valuation, PYPL looks cheap. The management’s efforts to improve efficiency would add to shareholder value going forward.

Check this space to read management/analysts’ comments on quarterly reports

The San Jose-headquartered payment solutions provider has successfully overcome adversities in the past and is currently taking measures to deal with macroeconomic headwinds. The management last month announced a workforce reduction that would affect around 7% of employees.

Financials

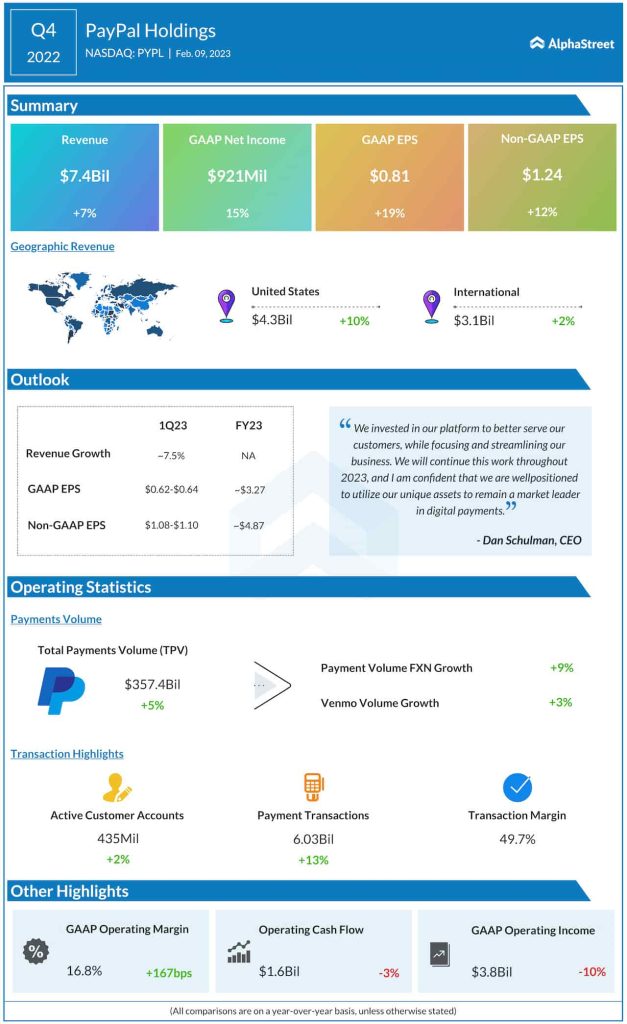

PayPal ended fiscal 2022 setting a new record – in the fourth quarter, revenues crossed $7 billion for the first time. The top line also came in above the market’s projection and was up 7% from the year-ago quarter. The broad-based revenue growth, across all regions, translated into a 12% increase in adjusted earnings to $1.24 per share. Earnings were above the management’s estimates and also topped expectations. There was a 5% growth in total payment volume, supported by a further increase in customer accounts.

Visa Inc.: Three factors that work in favor of this digital payments leader

“By the end of this year, we will have the appropriate cost structure to ensure that we deliver profitable growth with consistent and healthy non-GAAP EPS growth. And more importantly, we are confident we have the right roadmap in place to drive continued improvements in our customer experiences so that we remain a global leader in digital payments. In this current environment with so many of our competitors struggling to make money, we see a path to emerge from this economic downturn in a position of increased strength,” said PayPal’s CEO Dan Schulman.

CEO to Retire

Dan, who played a key role in the company’s growth during his seven-year stint as the CEO, will be stepping down by year-end. The management has initiated a search for a new chief. After retirement, he will continue to be a member of the company’s board of directors.

This week, PayPal’s shares hovered near the $80-mark, which is below their long-term average. The stock traded higher on Friday.