PayPal Holdings Inc. (NASDAQ: PYPL) has maintained its dominance in the payment solutions market, navigating through unfavorable market conditions and rising competition. The company is now busy streamlining the business through initiatives like rightsizing the cost structure and reducing its real-estate footprint.

Though shares of the San Jose-headquartered payment solutions provider had a positive start to 2023, they could not maintain the momentum. This week, the stock traded close to the levels seen at the beginning of the year. Going by experts’ outlook on the company and the broad market, PYPL is on track to regain the lost momentum and cross the $100 mark in the coming months.

Checkout Experience

The management’s focus has been on enhancing the checkout experience lately, to defend and grow market share in the company’s branded checkout business, amid competition from the likes of Apple Pay which recently launched a futuristic mobile checkout service. PayPal is maintaining a healthy cash flow that would help it execute growth initiatives and reinvigorate the top line, thanks to the company’s 435 million active accounts.

From PayPal’s Q4 2022 earnings conference call:

“In the past two years, we have introduced a significant number of products and services. For instance, our Buy Now Pay Later services is driving significant lists in checkout and incremental TPV, and it’s now one of the most popular Buy Now Pay Later services in the world with almost $200 million in loans to over 30 million consumers since launching in 2020 and with approximately 300,000 merchants, putting our Buy Now Pay Later upstream on their product pages.”

Q1 Results Due

PayPal will be releasing the first-quarter financial report and holding a conference call to discuss the results on May 8, after the regular market hours. On average, analysts following the company are forecasting a 12.5% increase in earnings, on an adjusted basis, to 0.99 per share, continuing the recovery that started in the previous quarter.

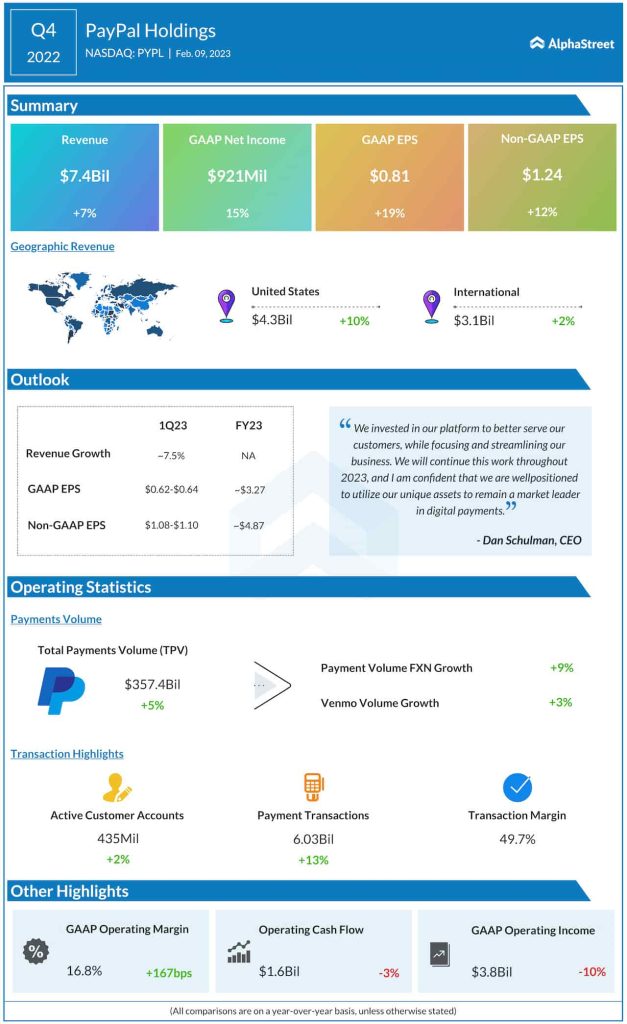

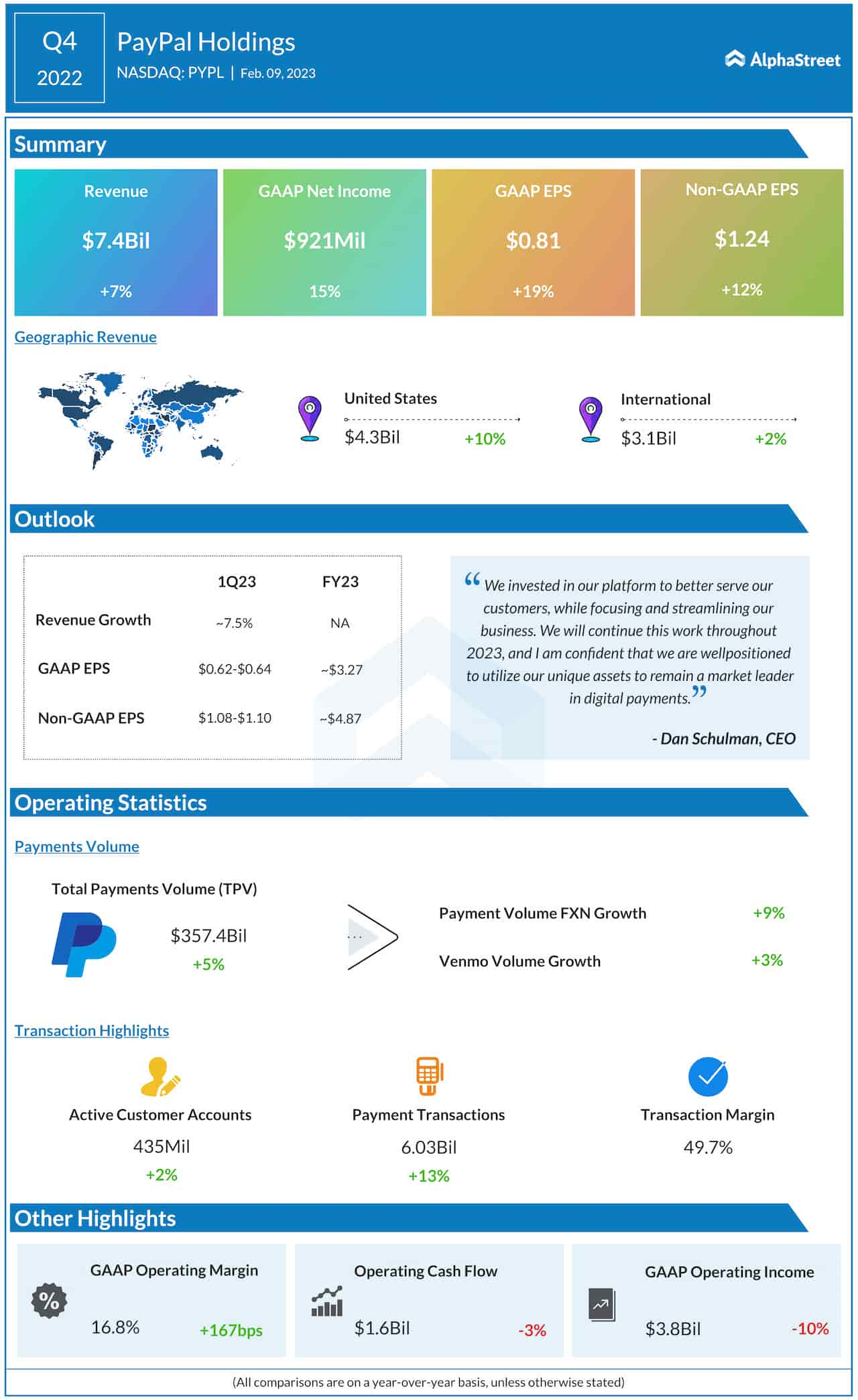

However, the consensus revenue estimate — at $6.27 billion — represents a 3.3% decline from last year. In the fourth quarter, revenues rose by 7% to $7.4 billion, as they did in every quarter last year. The top-line growth resulted in a 12% rise in net profit, excluding one-off items, to $1.24 per share, which marked the first increase after three consecutive declines.

Shrugging off the recent weakness, PayPal’s stock traded slightly higher on Wednesday afternoon. In the last 30 days, it lost about 3%.