PayPal Holdings, Inc. (NASDAQ: PYPL) closed fiscal 2025 with modest but diversified growth, underscoring resilience in its core digital payments franchise even as revenue expansion remained measured. The company emphasized profitable growth and operational discipline, supported by higher payment activity and improved earnings performance.

Fourth-Quarter Performance

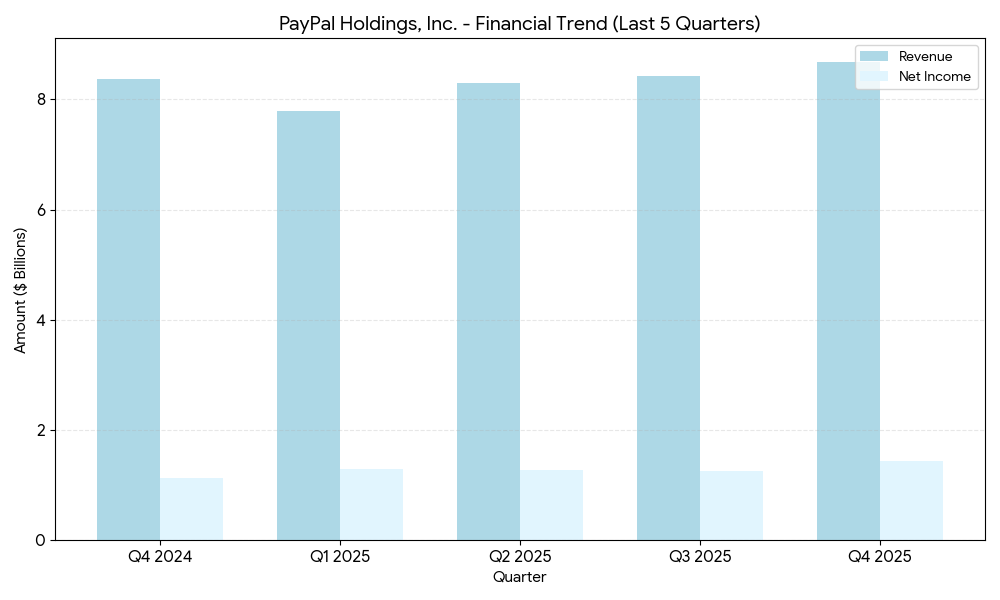

For the fourth quarter ended December 31, 2025, PayPal generated net revenue of approximately $8.7 billion, representing a 4% year-over-year increase. Transaction margin dollars — a key profitability indicator — rose about 3% to $4.0 billion, while GAAP operating income climbed 5% to $1.5 billion. Earnings per share on a GAAP basis surged 38% to $1.53, reflecting improved cost management and operating leverage.

Net income reached roughly $1.44 billion, making it one of the company’s strongest quarterly profit performances in recent periods.

Payment activity remained robust. Total payment volume (TPV) increased 9% to $475.1 billion, supported by continued consumer and merchant engagement, while payment transactions grew to about 6.8 billion.

However, some reports noted that adjusted earnings per share and revenue came in slightly below analyst expectations, highlighting the market’s sensitivity to growth trajectories even amid stable fundamentals.

Full-Year 2025 Highlights

For the full year, PayPal reported net revenues of $33.2 billion, up 4%, alongside a 35% increase in GAAP earnings per share to $5.41.

Annual TPV reached approximately $1.79 trillion, marking a 7% rise and reinforcing the company’s scale within the global digital payments ecosystem.

User metrics showed incremental expansion, with active accounts growing to about 439 million, including a sequential gain of roughly 1.2 million accounts in the fourth quarter.

Strategic Positioning and Operational Focus

Management characterized the year as one of “diversified and profitable growth,” pointing to initiatives designed to strengthen the company’s foundation while accelerating future expansion opportunities.

The combination of higher transaction margins and rising operating profit suggests PayPal is prioritizing quality of revenue rather than aggressive user acquisition — a strategy increasingly visible across mature fintech platforms seeking sustainable returns.

Still, the relatively moderate pace of revenue growth compared with some fintech peers indicates an evolving competitive landscape, where innovation, pricing strategies, and value-added services are becoming critical differentiators.

Outlook Context

Quarterly trends signal a company balancing growth with profitability. While top-line expansion remained in the mid-single digits, stronger earnings and payment volumes point to continued demand for digital payment solutions. As the global shift toward cashless transactions persists, PayPal’s scale, expanding engagement metrics, and improving earnings profile position it to remain a significant participant in the digital commerce infrastructure — even as investors and industry observers closely monitor the company’s ability to reaccelerate revenue growth in the years ahead.