Shares of Peloton Interactive Inc. (NASDAQ: PTON) were down 8% on Friday, a day after the company reported mixed results for the fourth quarter of 2021. Although revenues surpassed market estimates, the company reported a larger-than-expected net loss for the quarter.

While the earnings report contained some positive highlights like revenue and subscription growth, there were areas of concern such as the Connected Fitness churn rate and the price cut for the Peloton Bike. The sentiment around the stock is one of cautious optimism based on the challenges and growth plans outlined by the company.

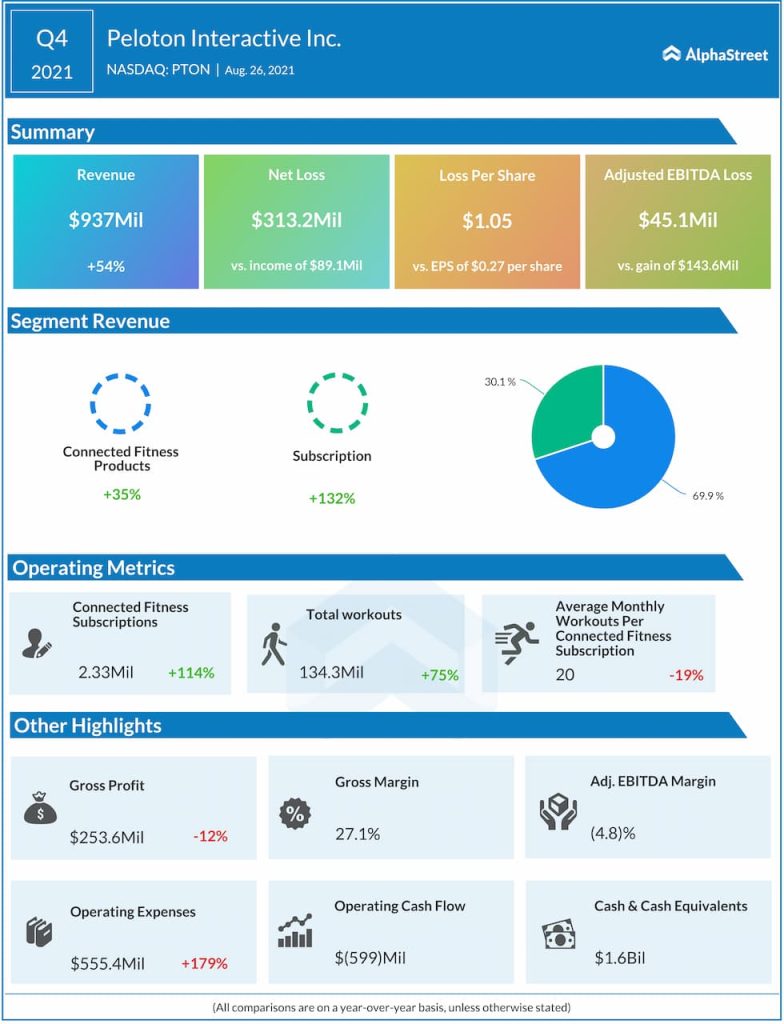

Revenue

Peloton’s total revenue grew 54% year-over-year to $937 million in Q4. Revenues were down sequentially from $1.26 billion in Q3. In Q4, revenue growth was negatively impacted by the Tread product recalls. For the first quarter of 2022, the company expects revenue to grow 6% YoY to approx. $800 million. This is lower than analysts’ projections of $1.06 billion for Q1.

Looking into FY2022, Peloton expects sales trends to be impacted by seasonal weather as well as holiday and New Year’s resolutions purchases. The company expects to see higher unit sales for Bike and Bike+ in 2022 compared to 2021 and also anticipates the lower-priced Tread to gain strong acceptance. Revenues are expected to grow 34% YoY to $5.4 billion in FY2022, better than analysts’ projections of $5.3 billion.

Profitability

In Q4, Peloton reported a net loss of $313.2 million, or $1.05 per share, compared to a net income of $89.1 million, or $0.27 per share, in the year-ago quarter. The company expects its profitability in the near term to be impacted by the Bike price cut, a sales mix shift to Tread, increases in commodity costs and freight rates and other growth investments.

Gross margin in Q4 was 27.1%, below the company’s expectations. This was caused by lower-than-expected margins of 11.6% in the connected fitness product segment. Peloton expects gross margins of 33% for the first quarter of 2022 and 34% for FY2022, based on connected fitness product gross margin of 15% in Q1 and 23% for the year.

Subscriptions

During the fourth quarter, Peloton’s Connected Fitness subscriptions grew 114% to 2.33 million while paid digital subscriptions grew 176% to over 874,000. At the end of the quarter, the company had over 5.9 million members globally, which was up 93% YoY.

Total platform workouts reached 154.5 million, up 86% YoY. Although Connected Fitness subscription workouts were up 75% to 134.3 million, average monthly workouts per Connected Fitness subscription were down to 19.9 from 24.7 in the year-ago quarter. The average net monthly Connected Fitness churn was 0.73%, much higher than 0.31% reported in the third quarter.

Peloton expects to end the first quarter with 2.47 million Connected Fitness subscriptions, which would reflect a YoY growth of 85%. Monthly average net churn for Connected Fitness subscriptions is expected to be 0.85%. For the full year, the company expects Connected Fitness subscriptions to grow 56% YoY to 3.63 million.

Growth plans

Peloton will continue to invest significantly in new hardware, software and content offerings for cardio and strength training. The company will focus more on driving subscription growth than on near-term profitability as it believes there is meaningful opportunity to bring more consumers to connected fitness at home.

Peloton is also looking to expand into new markets as well as tap additional distribution channels such as corporate wellness. As part of its efforts to make its products more accessible to customers, the company is reducing the price of its original Bike by $400 to $1,495. The company plans on investing approx. $600 million in capital expenditures in FY2022 and expects to be adjusted EBITDA profitable in FY2023.

Peloton’s stock has dropped 31% since the beginning of this year.