PepsiCo Inc. (NASDAQ: PEP) came out of another pandemic-affected quarter with better-than-expected results. Although the company’s top and bottom line numbers dropped in the second quarter of 2020, they were higher than analysts’ projections. The numbers were helped by strength in the company’s snacks business while the beverages division saw a decline.

Snacks vs. beverages

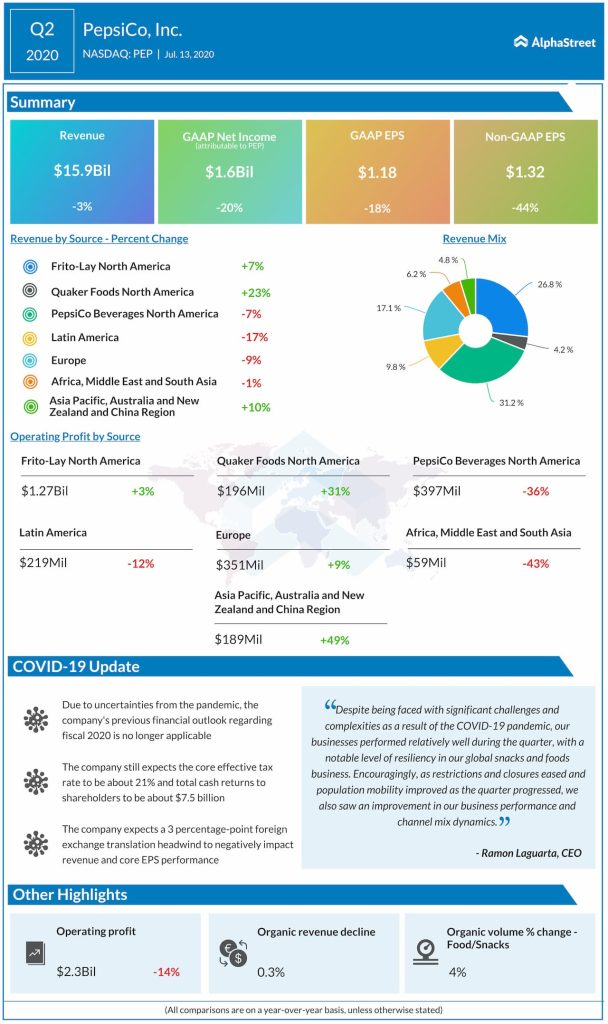

PepsiCo appears to have benefited more from its snacks division than its beverages business despite being known worldwide for its signature soft drink Pepsi. The company’s Frito-Lay segment has consistently performed well, delivering revenue growth while outperforming the Beverages unit most of the time. In 2019, 54% of PepsiCo’s revenue came from Food while 46% came from Beverages.

In the second quarter, the Frito-Lay segment posted revenue growth of 7% and volume growth of 4%, helped by strong growth in snacks like Tostitos, Ruffles, Doritos and Cheetos. The coronavirus pandemic drove higher demand for snacks as well as ready-to-eat foods, which led to a 23% revenue growth in the Quaker Foods segment. Quaker witnessed the highest rate of growth among segments in the quarter, helped by growth in oatmeal, ready-to-eat cereals and Aunt Jemima syrup and mix.

In the PepsiCo Beverages North America division, revenue fell 7% while volume dropped 10%. Volumes fell in both carbonated soft drinks and non-carbonated beverages. The company saw declines in its water and juice portfolios, Lipton ready-to-drink teas, and Gatorade sports drinks as the health crisis caused lower sales in away-from-home channels.

Acquisitions

Even in the midst of the pandemic, PepsiCo continued to make acquisitions which in turn is going to help boost its product portfolio. In March, the company acquired South Africa-based food and beverage company Pioneer Foods for approx. $1.2 billion.

In April, PepsiCo acquired energy drink maker Rockstar for an upfront cash payment of $3.85 billion and contingent consideration of approx. $0.85 billion. The company expects to complete the integration of Rockstar by the end of July. This deal has helped add the Bang, Rockstar and some of the Mountain Dew brands to its energy offer which is a positive development for the company. In June, the company acquired Chinese snack company Be & Cheery for approx. $0.7 billion.

Outlook

Looking ahead to the third quarter of 2020, PepsiCo expects organic revenue to increase within a low-single digit range. Core operating margin is expected to contract but not as much as the second quarter as the company expects to continue incurring costs related to maintaining health and safety. Foreign exchange translation headwinds are expected to negatively impact revenue and core EPS by 3%.

Click here to read the full transcript of PepsiCo Q2 2020 earnings conference call