PepsiCo, Inc. (NASDAQ: PEP) has remained broadly unaffected by inflation pressures and weak consumer spending so far, thanks to the food and beverage giant’s loyal customers and brand value. The company has entered fiscal 2023 on a positive note, reporting an increase in revenues for the first quarter when higher selling prices more than offset a decline in volume. The management’s automation and eCommerce initiatives are having a positive effect on margins.

Last month, shares of the New York-based soft drink company climbed to an all-time high. The stock has been on an upward spiral for quite some time, and the uptrend gathered steam after the last earnings. The stock currently offers a bigger-than-average dividend yield of 2.8%, after a modest hike at the beginning of the year. Encouragingly, the valuation remains reasonable despite the recent gains.

The management has a proper strategy in place to deal with macro uncertainties and the strain on people’s spending power. It is also reducing costs and hiking product prices while being bullish on the company’s future outlook. However, the squeeze on margins compared to the long-term trend will be a concern in the near future.

Q2 Earnings on Tap

When the company releases its second-quarter report next week, the market will be looking for adjusted earnings of $1.95 per share on revenues of $21.7 billion, which is up 5% and 7% year-over-year respectively. The report is expected on July 13, before the market opens.

From PepsiCo’s Q1 2023 earnings conference call:

“We are investing in our innovation, investing in our brands, investing obviously in value in different ways, pricing, and sizing in mostly. So, we’re seeing a good positive competitive environment in the US, in Europe, and also in our developing markets, consistently across the world. When it comes to pricing as we said earlier in February, we have mostly taken the pricing already this year that we needed to cover for our cost increases and that’s — it is where we stand at this point.”

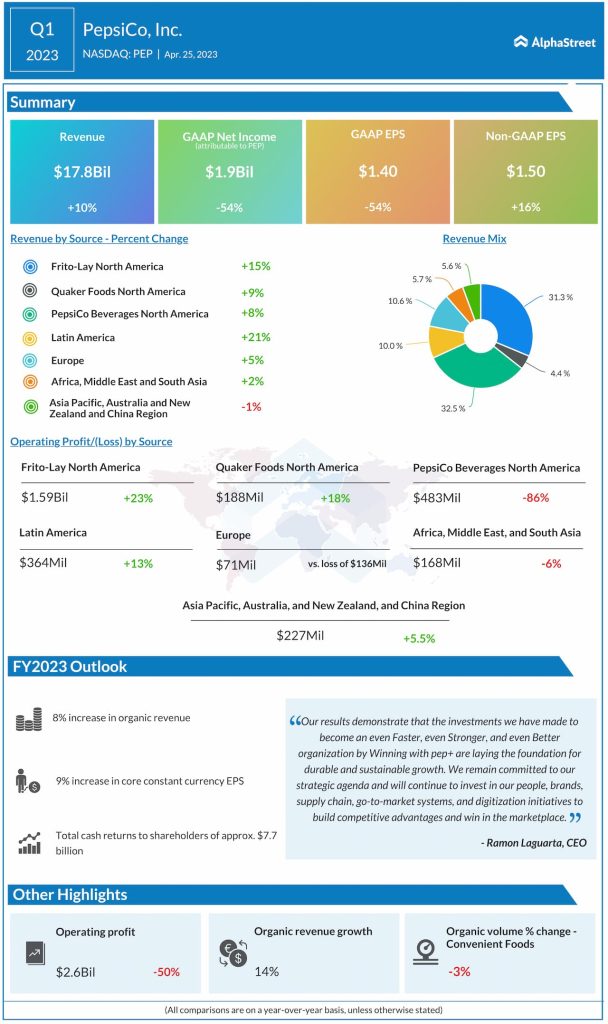

Past Performance

In the March quarter, revenues of the main business divisions, led by PepsiCo Beverages and Frito-Lay, increased. Total revenues grew 10% annually to $17.8 billion, resulting in a double-digit increase in adjusted earnings to $1.50 per share. Unadjusted profit was $1.93 billion or $1.40 a share in Q1, compared to $4.26 billion or $3.06 a share in the year-ago period.

Organic revenue, excluding the effect of acquisitions and divestitures, moved up an impressive 14.3%. The results topped expectations, continuing the long-term trend. Interestingly, the company’s quarterly earnings have either beaten or matched analysts’ estimates regularly for more than a decade now.

Outlook

Anticipating the positive momentum to continue in the remainder of the year, PepsiCo executives raised the full-year earnings growth guidance to 9% from the initial target of 8%. The optimism can be attributed to favorable pricing and the company’s strong portfolio which got bigger after the launch of new energy drinks and sparkling water.

PEP is trading above its 52-week average, after gaining about 5% since the beginning of the year. The stock traded higher in the early hours of Wednesday’s session.