In recent years, PepsiCo, Inc. (NASDAQ: PEP) has moved beyond its roots as a traditional soft-drink company, reshaping itself around healthier foods, sustainability, and digital innovation. This transformation has helped the company stay relevant as consumer tastes shift and rivals push hard to capture market share.

Q4 Report on Tap

The company has scheduled the release of its fourth-quarter FY25 earnings report for Tuesday, February 3, at 6:00 am ET. On average, analysts following the business project core earnings of $2.24 per share for the December quarter, higher than $1.96 per share the company earned in Q4 FY24. It is estimated that fourth-quarter revenues increased 4.3% annually to $28.97 billion.

PepsiCo has a strong track record of regularly increasing its quarterly dividends; the stock currently offers a better-than-average yield of 3.9%. Last year, PEP experienced significant fluctuation, and it is currently trading close to the levels seen a year ago. In the past six months, the stock gained about 4%. While the company’s cost-cutting program is expected to translate into better shareholder returns, trimming the product lineup to simplify the portfolio might affect customer loyalty.

Q3 Results Beat

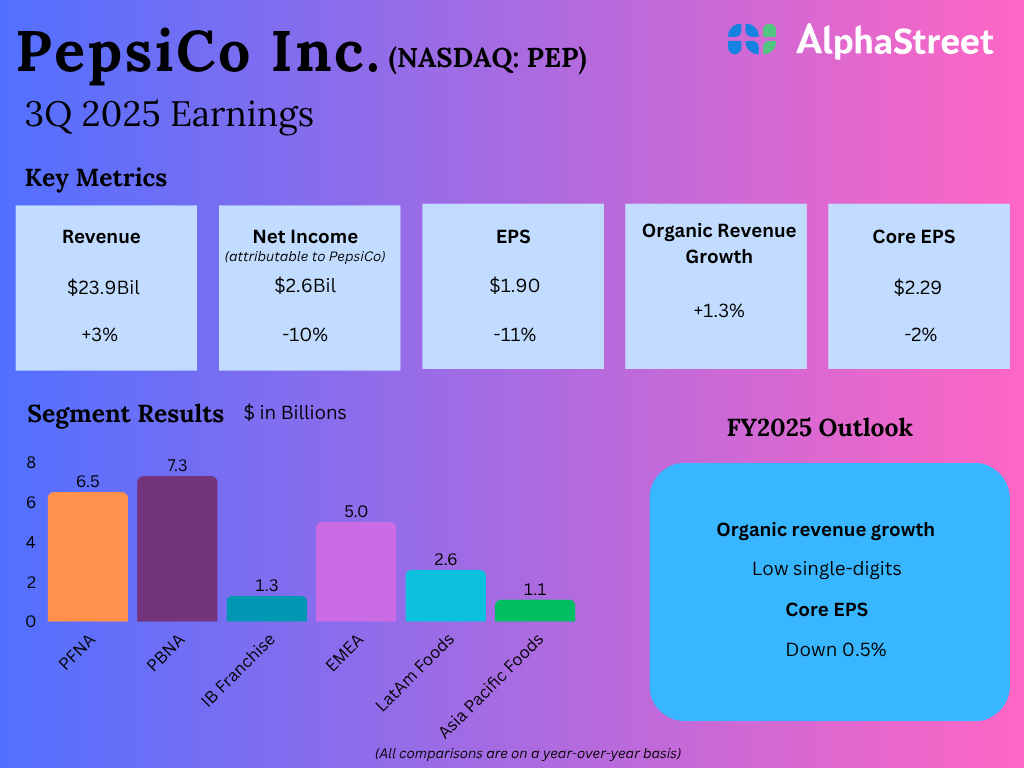

For the third quarter, PepsiCo reported net revenues of $23.9 billion, up 2.6% year-over-year, with organic revenues rising 1.3%. Core earnings, adjusted for special items, moved up 2.3% annually to $2.29 per share in Q3, on a constant currency basis. Net income attributable to the company dropped to $2.6 billion from $2.9 billion in the prior-year quarter. On a per-share basis, earnings were $1.90, which is down 11% YoY. Both revenue and earnings beat expectations. For fiscal year 2025, the company expects a low-single-digit increase in organic revenue and a 0.5% decline in core EPS.

From PepsiCo’s Q3 2025 Earnings Call:

“We’ve invested a lot in technology in the last five years. It is in our P&L. It’s been a cost for us for the last five years. Now, we can benefit from applying technology to everything we do, applying AI, overlaying intelligence to the infrastructure of data we’ve created. And that will give us optionality, agility and flexibility, which is probably what the market requires, given the continuous pivot from the consumer and from our partners and our customers. So that’s how we’re thinking.”

Road Ahead

Now, PepsiCo is positioned as a brand focused on balancing indulgence with wellness, not just as a food and beverage leader. In a recent statement, management said it expects full-year 2026 organic revenue growth to range between 2% and 4%, anticipating growth at the high end of that range in the second half of the year. Acquisitions — net of divestitures — from last year are expected to contribute one percentage point to reported net revenue growth in FY26.

On Thursday, PepsiCo’s stock opened at $148.90, and it was trading up 1% in the afternoon. The shares have gained 4.7% since the beginning of 2026.