Shares of Philip Morris International Inc. (NYSE: PM) jumped 10% on Thursday after the company delivered better-than-expected earnings results for the fourth quarter of 2024 and provided an encouraging outlook for fiscal year 2025. The strong quarterly performance was driven by continued momentum in the smoke-free business as well as strength in combustibles.

Better-than-expected results

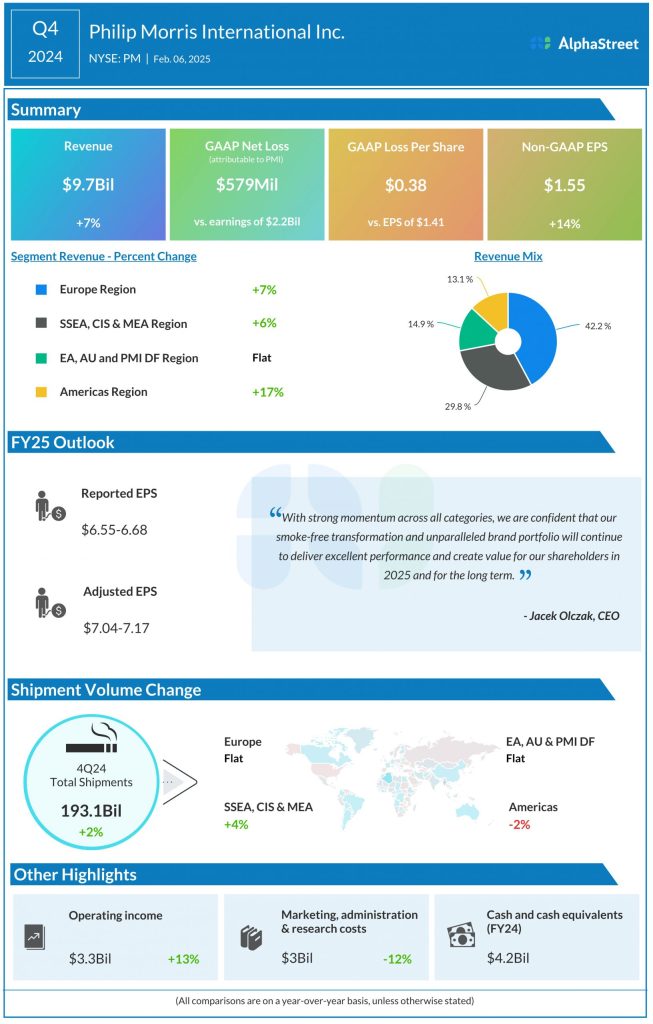

In Q4 2024, Philip Morris’ net revenues increased 7.3% year-over-year to $9.7 billion, beating estimates of $9.4 billion. Organic revenue growth was also 7.3%. Adjusted earnings per share grew 14% to $1.55, surpassing the consensus target of $1.50.

Smoke-free momentum

Philip Morris’ smoke-free business continued to see robust growth in Q4, with revenue up 9.2% and gross profit up 15.1%. This business made up 40% of total revenues and around 42% of gross profit in the fourth quarter. The company’s smoke-free products are now available in 95 markets with an estimated 38.6 million adult users.

The strength in smoke-free was driven by IQOS and ZYN. Heated tobacco units (HTU) adjusted in-market sales (IMS) volume was up 13% in Q4. In Japan, IQOS HTU adjusted market share increased to 30.6%, and in Europe, it increased to 10.6% during the quarter. IQOS benefited from double-digit growth in markets like Spain, Bulgaria, and Germany.

PM’s oral smoke-free products saw shipment volume increase by 22% in the fourth quarter, driven by the growth of ZYN nicotine pouches in the US. ZYN’s shipment volume grew 42% to 165 million cans, and its category share grew to 65.9% in Q4. The company launched nicotine pouches in six new markets during the quarter to reach a total of 37 markets worldwide.

PM is also seeing an increasing contribution to growth in e-vapor from VEEV, which is showing encouraging volume momentum in closed pods as well as a strengthening market position.

Steady combustibles

The combustibles division saw revenues grow by 6% in Q4, driven mainly by high-single-digit pricing and volume growth in markets like Turkey, India and Brazil, where smoke-free products are not allowed. Cigarette shipment volume rose 1.1% in the quarter. The company’s brand portfolio and Marlboro both achieved market share gains.

Outlook

For fiscal year 2025, PM expects organic revenue growth of 6-8%. GAAP EPS is expected to be $6.55-6.68 for the year. Adjusted EPS is expected to be $7.04-7.17, representing a YoY growth of 7.2-9.1%. The company anticipates total cigarette and smoke-free product shipment volume growth of up to 2% for the year, driven by smoke-free products volume growth of 12-14%.