Shares of Philip Morris International Inc. (NYSE: PM) were down over 1% on Monday. The stock has gained 15% in the past three months. The tobacco giant delivered revenue and earnings growth for the fourth quarter of 2025 as its smoke-free business continues to grow and combustibles remain resilient.

Q4 performance

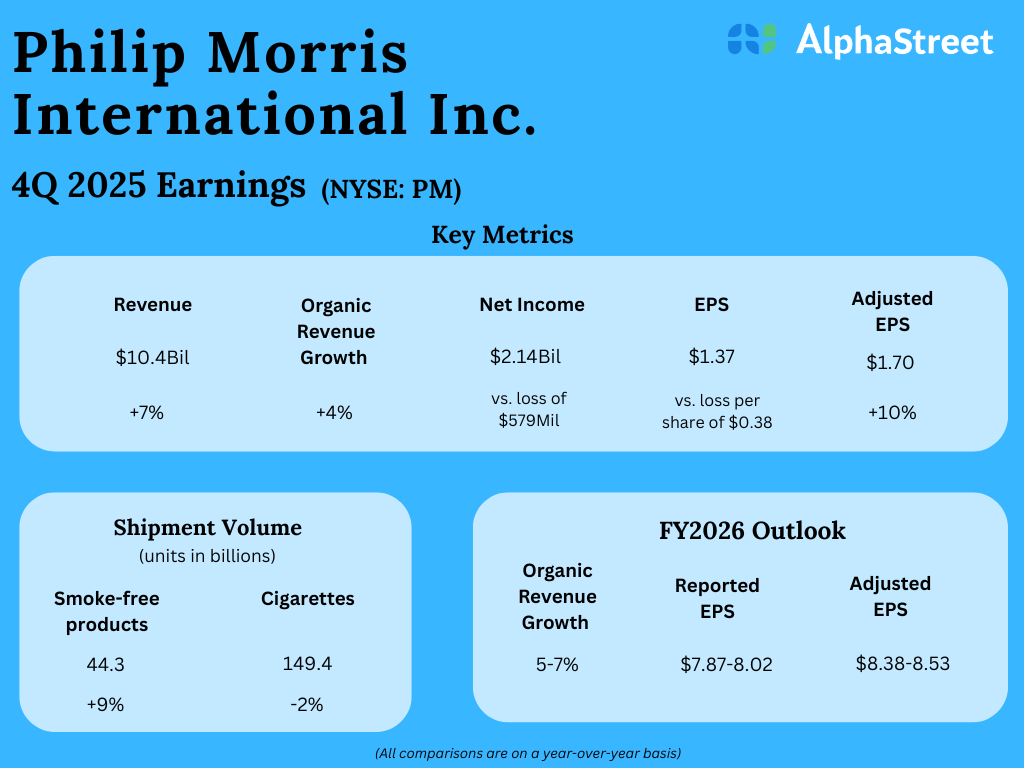

Philip Morris generated revenues of $10.4 billion in the fourth quarter of 2025, which was up 6.8% on a reported basis from the previous year. On an organic basis, revenues grew 3.7%, helped by higher cigarette prices, and favorable volume/mix driven by higher smoke-free product volumes. On a GAAP basis, the company reported earnings per share of $1.37 versus a loss of $0.38 per share last year. Adjusted EPS rose 10% year-over-year to $1.70.

Smoke-free momentum and steady combustibles

Philip Morris continues to see strong performance from its smoke-free business, with double-digit growth in revenue and gross profit during the fourth quarter. Revenue and gross profit were both up 12%, and the smoke-free business made up 50% of net revenues in three of the company’s four regions. PM has expanded its smoke-free products (SFP) into 106 markets.

In the heat-not-burn category, IQOS continues to hold a strong position. In Q4, heated tobacco units (HTU) adjusted in-market sales (IMS) volume growth accelerated to 12%. This category benefited from strong growth in Japan and Europe with regions like Italy, Germany and Spain delivering double-digit gains.

In oral SFP, shipments rose 7.3% in Q4. In the US, nicotine pouches are the fastest growing category, led by Zyn with premium pricing and a majority value share. Zyn’s shipment volume in the US grew 19% in Q4. PM continues to expand its international nicotine pouch business helped by strong market share gains, with Zyn available in 55 markets.

The combustibles business remained resilient with a 3.2% growth in revenue and 5.5% growth in gross profit during the fourth quarter despite a 2.2% drop in cigarette shipment volume. During the quarter, Marlboro’s category share reached 11%, marking a milestone.

Outlook

For fiscal year 2026, PM expects organic revenue growth of 5-7%. The company expects reported EPS to range between $7.87-8.02 while adjusted EPS is estimated to range between $8.38-8.53. For the first quarter of 2026, adjusted EPS is expected to range between $1.80-1.85.