Shares of Philip Morris International Inc. (NYSE: PM) have gained 26% over the past one year and 14% year-to-date. The company ended fiscal year 2021 on a strong note last week with Q4 revenue and profits exceeding expectations. It also provided an upbeat outlook for fiscal year 2022. Here are three points that work in favor of the tobacco giant:

IQOS

IQOS gives PMI ample opportunity for growth. At the end of the fourth quarter, the company had around 21.2 million IQOS users, of which around 15.3 million had switched to IQOS and stopped smoking. IQOS devices accounted for over 6% of the $9.1 billion in net revenue from reduced risk products in 2021.

The rollout of IQOS ILUMA in Japan and Switzerland has generated strong results while IQOS VEEV is gaining traction in early launch markets. IQOS is seeing strong momentum and in the coming year, as device shortages ease, the company expects to slowly return to user growth at or above the prior run rate of around 1 million per quarter.

Smoke-free net revenues comprised over 30% of the adjusted total in the fourth quarter. For full-year 2021, it made up 29% compared to 24% in 2020, putting PMI on track to become a majority smoke-free company by 2025.

Along with strong progress in developed countries like Japan, IQOS is seeing promising growth in low and middle income markets like Egypt, Lebanon, Jordan and the Philippines. PMI continues to roll out its smoke-free products into new geographies as it aims to be in 100 markets by 2025. In the fourth quarter, the company launched IQOS in Morocco and Tunisia. This brings the total number of markets where its smoke-free products are available for sale to 71. In FY2022, the company expects heated tobacco units (HTU) shipment volumes to be 113-118 billion.

Market share

The company continues to gain and retain market share for its categories. In the fourth quarter, PMI’s share of the combustible category recovered and was stable on a year-over-year basis. The company’s leadership in combustibles helps to maximize switching to smoke-free products and it expects to maintain a stable category share over time despite IQOS cannibalization.

PMI’s heated tobacco units now have a 7.1% share in the markets where they are present. In the EU region, HTU share reached 6.4% of total cigarette and HTU industry volume during the fourth quarter. In Hungary, its national HTU share exceeded 20%. In Russia, HTU share reached 8% in Q4. PMI plans to add more markets in 2022 and also broaden its product offer and price segmentation within existing geographies.

Outlook

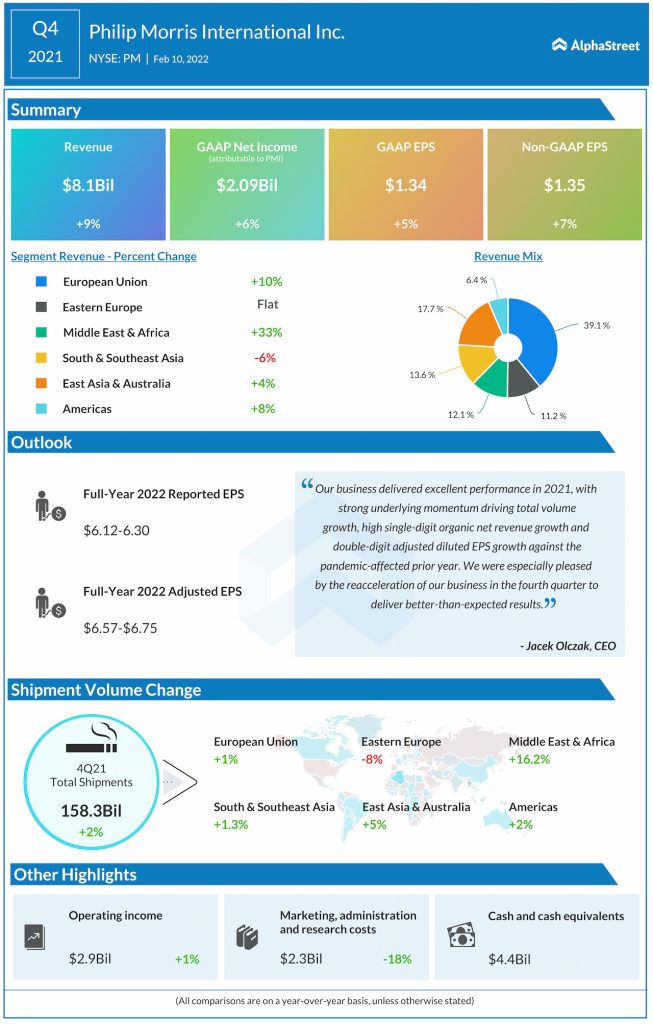

For FY2022, PMI expects organic net revenue growth of between 4-6% keeping it on track to deliver its 2021-2023 CAGR target of more than 5%. Reported EPS is expected to range between $6.12-6.30 while adjusted EPS, excluding currency, is estimated to range between $6.57-6.75.

Click here to read the full transcript of Philip Morris’ Q4 2021 earnings conference call