Pinterest Inc. (NYSE: PINS) is scheduled to report third quarter 2019 earnings results on Thursday, October 31, after the market closes. Analysts are expecting a loss of $0.04 per share on revenue of $280.6 million.

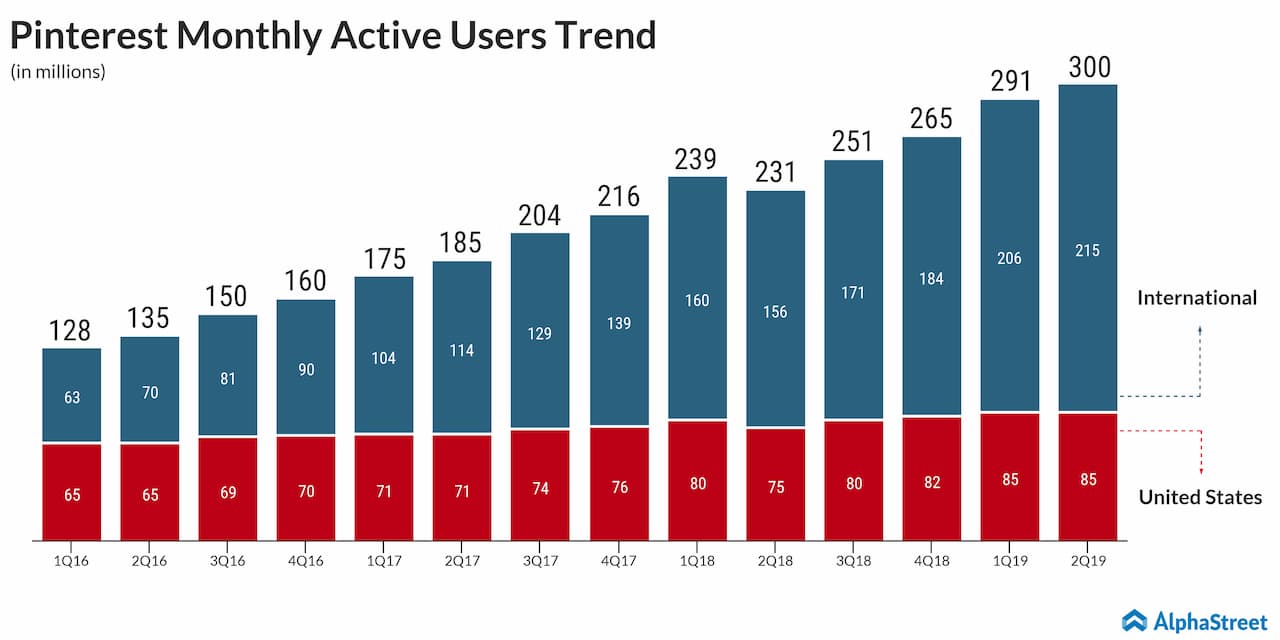

The company has seen strong revenue and user growth both in the US and internationally and this trend is expected to continue in the third quarter. At the end of the second quarter, monthly active users (MAU) stood at 300 million, representing a 30% increase from last year. The growth reflected double-digit increases in MAUs both domestically and internationally.

Also read: Pinterest Q3 2019 earnings results

Pinterest has also seen growth in the average revenue per user (ARPU) metric. Last quarter, global ARPU was up 29%, with a 41% increase in the US. International ARPU jumped 123% year-over-year but foreign markets tend to have a low monetization rate.

The strength seen in advertising revenue is likely to continue in the third quarter as the company focuses on delivering the most relevant content possible. However, Pinterest faces tough competition in the advertising space from Facebook’s (NYSE: FB) Instagram and Twitter (NYSE:TWTR).

In the second quarter of 2019, Pinterest beat revenue estimates and reported a narrower-than-expected loss. Revenues rose 62% year-over-year to $261 million. Adjusted loss narrowed to $0.06 per share versus the loss of $0.27 per share reported last year.

For the full year of 2019, Pinterest has guided for total revenue to be between $1.09 billion and $1.11 billion.

Pinterest’s shares are up nearly 9% since its IPO in April and the stock is currently trading at a 36% upside to its opening price. It has an average price target of $34.44.

Last week, Pinterest’s rival Snap Inc. (NYSE: SNAP) reported third quarter 2019 results, beating analysts’ estimates. Revenues rose 50% while adjusted loss narrowed to $0.04 per share and the user base saw a 13% growth.