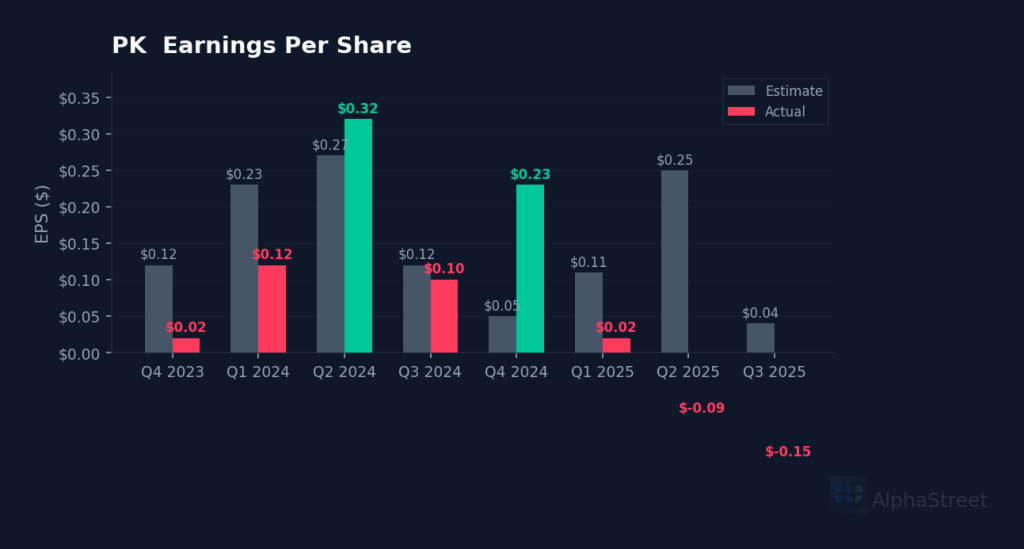

Worst miss in two years. Park Hotels & Resorts delivered a Q4 loss of $0.15 per share versus analyst expectations of a $0.04 profit, marking a 436.3% negative surprise. The hotel REIT posted its fourth consecutive quarterly miss, extending a troubling pattern that began in Q2 2025. Revenue for the quarter hit $2.54 billion, though the company provided no comparison guidance figure.

The stock shrugs it off. Despite the earnings disaster, PK shares rose 3.8% to $11.55 in regular trading, with after-hours action adding another 1.8% to reach $11.32. The market’s muted response suggests investors had already priced in operational weakness after three straight quarters of disappointment. The stock traded near its 50-day average of $11.07, having spent most of early 2026 in a tight $10.50-$11.80 range.

RevPAR deterioration accelerates. In Q3 remarks that telegraphed Q4’s weakness, CFO Sean M. Dell’Orto reported revenue per available room of $181, down 6% year-over-year. Excluding the Royal Palm South Beach renovation closure, the decline was still 5%. Hotel adjusted EBITDA came in at $141 million, pointing to margin compression as the company battles elevated operating costs. The 16.2% operating margin in fundamentals data reflects persistent pressure across the portfolio.

Cost cuts can’t keep pace. Management’s focus on “minimizing cost in a challenging operating environment” hasn’t offset top-line deterioration, according to CEO Thomas J. Baltimore’s prepared remarks. Analysts on the Q3 call questioned whether expense reductions could match the pace of revenue declines, with one noting “you’re pulling expenses down to a surprising degree to offset” the lower RevPAR outlook. The company pointed to efficiency initiatives started in Q1 and Q2, but benefits have yet to materialize in earnings.

Balance sheet remains solid. With $8.83 billion in total assets and $3.38 billion in stockholders’ equity as of Q3, Park maintains financial flexibility despite operational struggles. The company paid $1.00 per share in dividends during 2025, maintaining its REIT distribution requirements. Analysts from Evercore, Citi, Deutsche Bank, and eight other firms grilled management on capital allocation priorities given the earnings trajectory.

No forward visibility. Park provided no Q1 2026 or full-year guidance, leaving investors to extrapolate from the consensus estimate of $0.10 for the current quarter ending March 2026. The forward P/E of 15.5x assumes $0.745 in annual earnings, a target that looks increasingly aggressive given four straight misses averaging 165% below estimates. Revenue declined 7.3% year-over-year in the most recent fiscal period.

This article was generated using AlphaStreet’s proprietary financial analysis technology and reviewed by our editorial team.