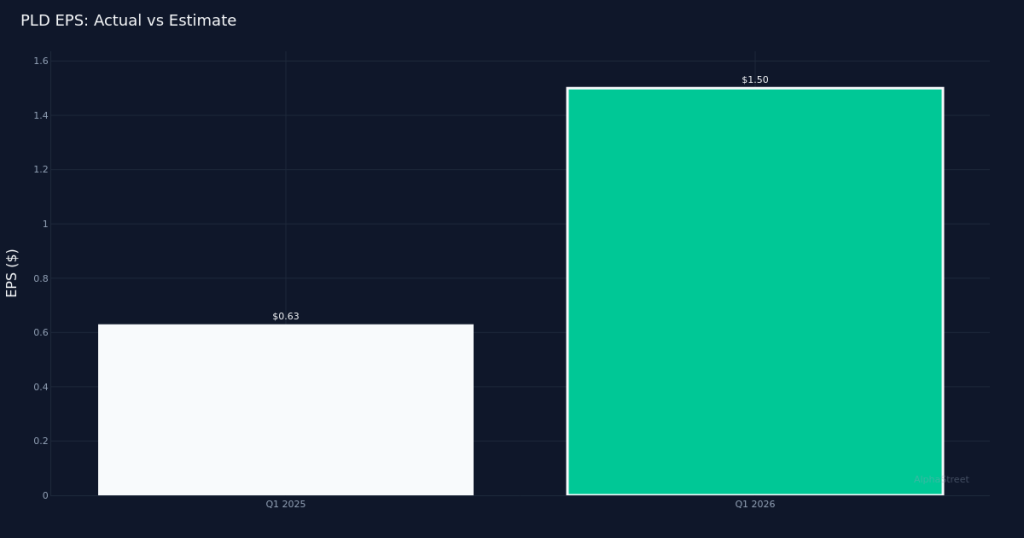

Massive Earnings Beat. Prologis, Inc. (NYSE: PLD) delivered a standout Q1 2026 performance, reporting Core FFO of $1.50 per share that crushed the $0.82 consensus estimate, beating by 82.9%. The industrial REIT generated $2.30B in revenue for the quarter, up 7.4% from the $2.14B recorded in Q1 2025, while Core FFO reached $1.44B. The strong top-line growth accompanying the substantial earnings beat suggests operational momentum rather than mere cost discipline, a quality signal for the world’s largest owner of logistics real estate.

Leasing Momentum Sustained. The magnitude of the Core FFO outperformance reflects robust demand fundamentals in the industrial property sector. Lease signings totaled 64 million of square feet for the quarter, demonstrating continued appetite for modern logistics space despite economic uncertainty. The company operated at 95.3% Period End Occupancy at quarter end, underscoring tight portfolio utilization that supports pricing power. The combination of accelerating revenue growth and substantial leasing volume indicates Prologis is capturing outsized benefits from the ongoing reconfiguration of supply chains and e-commerce fulfillment networks.

Full-Year Outlook. Management guided FY 2026 adjusted EPS to a range of $6.07 to $6.23, providing investors with visibility into expected performance for the balance of the year. This guidance will be scrutinized relative to the exceptional Q1 results, as analysts assess whether the 82.9% earnings beat reflects timing benefits or a sustainably higher earnings trajectory. The midpoint of $6.15 serves as a baseline for evaluating whether Prologis can maintain momentum through potential headwinds including development starts, capital deployment decisions, and cap rate movements.

Market Reaction Muted. Shares traded at $142.38, up just 1.8% following the results, a surprisingly modest response given the scale of the earnings surprise. This restrained reaction may reflect investor caution about sustainability of the beat, concerns about full-year guidance relative to the strong Q1 performance, or broader sector rotation dynamics. The tepid stock movement despite exceptional results warrants attention, as it suggests the market is either pricing in a normalization of performance or awaiting clarification on growth drivers during the earnings call.

Analyst Sentiment Mixed. Wall Street consensus stands at 11 buy ratings and 11 hold ratings with 0 sell recommendations, reflecting a perfectly balanced Street view on the stock. This even split suggests analysts are divided on valuation at current levels despite the company’s market leadership position, possibly weighing near-term execution strength against longer-term growth rate questions or concerns about industrial property cycle positioning.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.