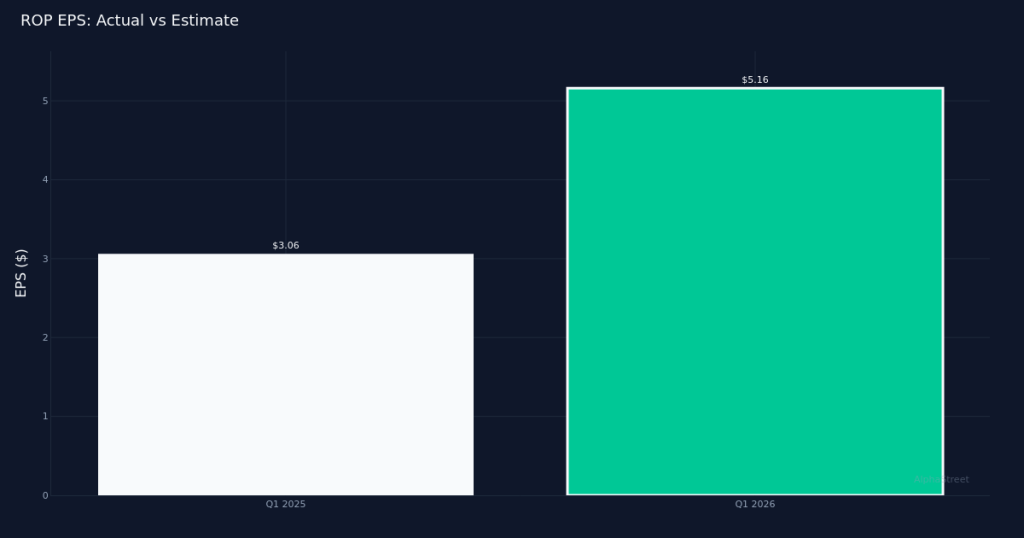

Solid Beat. Roper Technologies, Inc. (NASDAQ:ROP) delivered Q1 2026 adjusted earnings of $5.16 per share, beating the $4.99 consensus estimate by 3.4% based on estimates from 17 analysts. Revenue of $2.10B exceeded Wall Street’s $2.06B forecast by 1.5%, representing an 11.0% increase from $1.88B in Q1 2025. The stock traded largely unchanged following the report, suggesting investors had anticipated the modest outperformance or remain cautious on valuation despite the growth trajectory.

Revenue-Driven Performance. The quality of this beat appears fundamentally sound, anchored by organic revenue growth of 6.0% for the quarter. This metric indicates Roper is generating expansion from existing operations rather than relying solely on acquisitions or cost management to drive results. Bottom-line profit came in at $539.0M, reflecting the company’s ability to convert top-line momentum into meaningful profitability. The 11.0% year-over-year revenue growth demonstrates accelerating momentum in Roper’s diversified software and technology portfolio, with organic expansion providing a sustainable foundation for continued performance.

Application Software Dominance. Application Software led the business with $1.19B in revenue, up 11.5% year-over-year, underscoring the segment’s position as the primary growth engine. This vertical represents the majority of Roper’s total revenue base and its double-digit expansion validates management’s strategic focus on recurring, high-margin software businesses. The segment’s outperformance relative to the company’s overall growth rate suggests particular strength in mission-critical application areas where Roper maintains competitive advantages through deep customer relationships and specialized functionality.

Full-Year Outlook. Management provided FY 2026 adjusted EPS guidance of $21.80 to $22.05, establishing clear visibility for investors evaluating the company’s trajectory through year-end. The guidance range implies confidence in sustained operational execution and provides a framework for assessing whether the Q1 momentum represents a sustainable trend or temporary strength. With the first quarter already in the books, the midpoint of this range will serve as the key benchmark for assessing management’s ability to deliver on expectations amid evolving macroeconomic conditions.

Mixed Sentiment. Wall Street consensus stands at 5 buy, 11 hold, and 3 sell ratings, reflecting a cautious stance from the analyst community despite the company’s consistent execution. The hold-heavy distribution suggests many analysts view shares as fairly valued at current levels, even as the fundamental performance remains solid. This positioning indicates limited near-term upside may be priced in, requiring either multiple expansion or sustained beats to drive meaningful appreciation.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.