Ryanair Holdings plc (RYAAY, NASDAQ) is Europe’s largest low-cost airline by passenger numbers, operating short-haul flights across 40+ countries with a single-fleet Boeing 737 model and a high reliance on ancillary revenue.

Share Performance & Market Value

Ryanair shares rose about 1% in early U.S. trading following Q3 FY26 results, valuing the company at roughly $35 billion. Shares remain well above their 52-week low and near the annual high after a strong recovery over the past year.

Financial Report

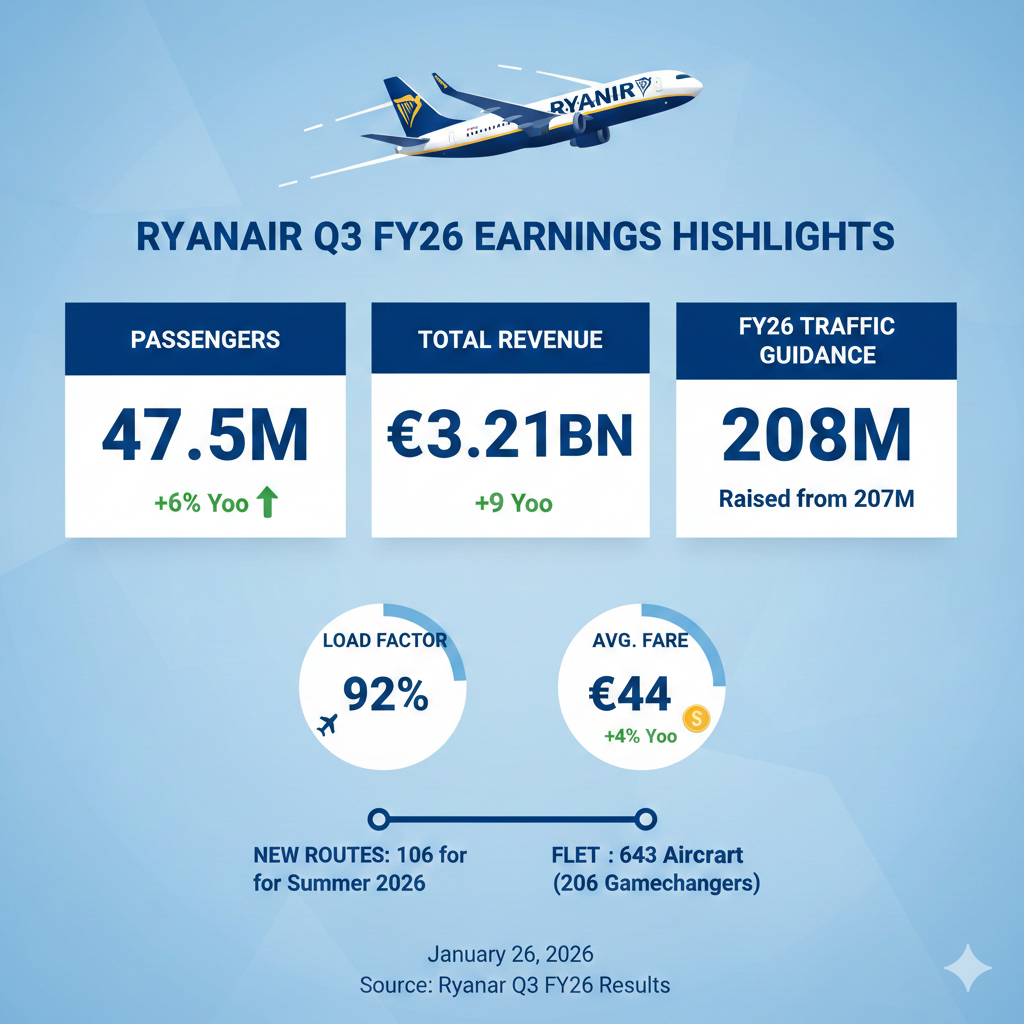

- Revenue: €3.21 billion, up 9% year over year.

- ARPU: Revenue per passenger rose ~3%, driven by a 4% increase in average fares and modest ancillary revenue growth.

- Costs and margins: Operating costs increased 6%; unit costs flat per passenger.

- Profitability: Pre-exceptional profit after tax fell 22% to €115 million. Including an €85 million regulatory provision, reported profit was €30 million.

Passenger Traffic

- Total passengers: 47.5 million, up 6% year over year.

- Growth was supported by strong demand across core European markets.

Fare Trends

- Average fares: Increased 4% year over year, reflecting strong demand and capacity discipline.

- The rise in fares contributed to higher ARPU and offset part of the cost inflation in fuel, labor, and airport charges.

Year-Over-Year & Full-Year Context

Compared with the prior year quarter, Ryanair delivered solid top-line growth from higher fares, ARPU, and passenger gains, but earnings were lower due to exceptional charges. The airline reaffirmed full-year guidance of ~208 million passengers and pre-exceptional profit after tax of €2.1–2.2 billion.

Guidance

Management cited strong forward bookings, fare momentum, and largely hedged fuel costs. Fleet expansion continues, although industry-wide delivery delays remain a constraint.

Analysts & Market Reaction

No major analyst upgrades, downgrades, or price-target changes were reported. Investor focus remained on cost discipline, ARPU trends, and regulatory impacts on near-term profitability.

Sector & Macro Backdrop

European airlines benefit from constrained capacity, supporting fares and ARPU, but face persistent pressure from fuel, labor, airport charges, and regulatory scrutiny.

Competitive Positioning

Ryanair maintains cost and ARPU advantages over peers. Competitors include easyJet, Wizz Air, Lufthansa, and Air France-KLM. Low-cost rivals face fleet and capacity constraints, while legacy carriers operate at higher structural costs.

Bottom Line

Ryanair posted higher revenue, stronger ARPU, rising passenger numbers, and positive fare momentum in Q3 FY26, reaffirmed full-year guidance, but year-over-year profit declined due to exceptional charges. The market reaction reflects solid operational performance tempered by regulatory and cost pressures.