Ryanair Holdings plc (RYAAY – NASDAQ) is Europe’s largest low-cost airline group, operating an extensive short-haul network that connects major and secondary cities across the continent. It has built its business on a no-frills model, disciplined cost control, and strong unit economics, maintaining high load factors and broad route coverage. Ryanair’s performance is closely watched as a bellwether for European leisure travel demand and cost trends in aviation.

Operational and Demand Trends

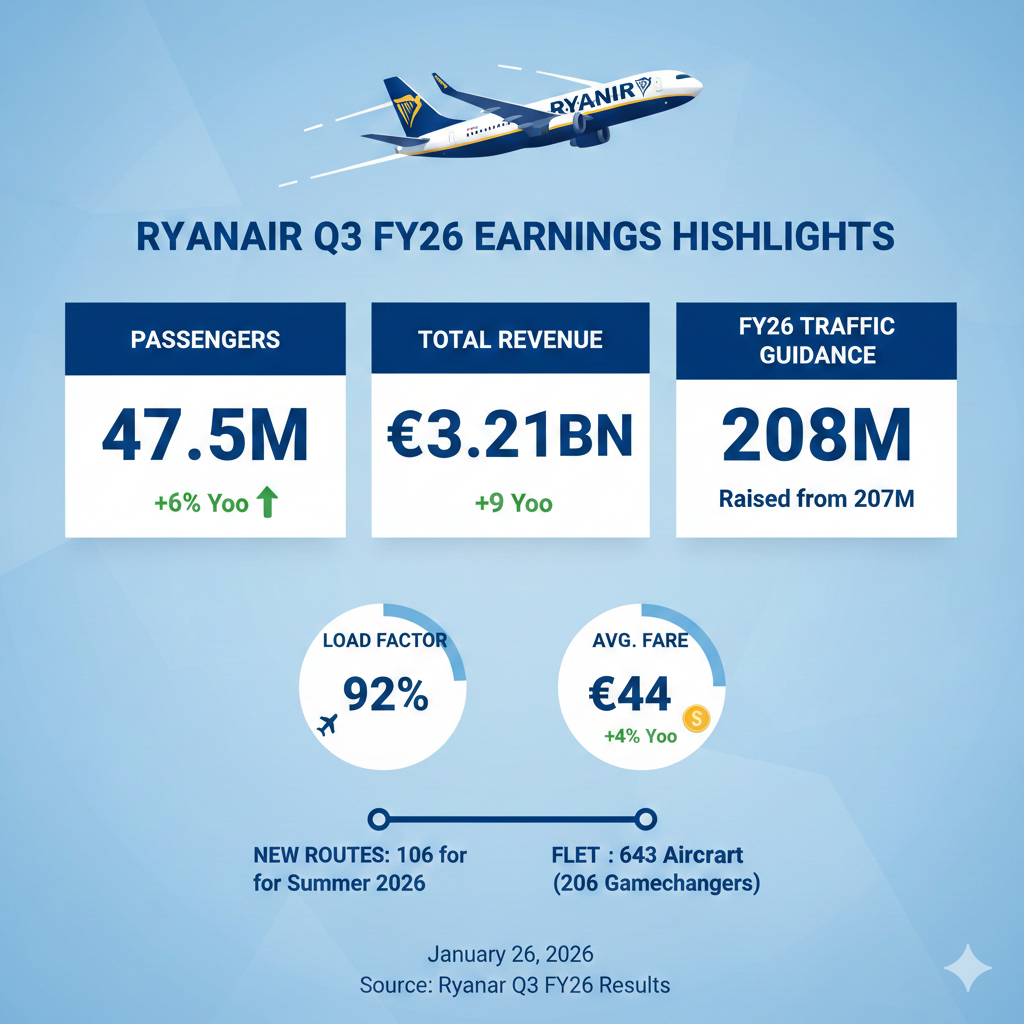

In the third quarter of fiscal 2026, Ryanair reported solid revenue growth and robust traffic expansion, even as reported profitability dipped due to non-recurring charges. Total revenue rose by approximately 9% year-over-year to about €3.2 billion, underpinned by a 6% increase in passenger traffic to roughly 47.5 million and higher average fares. Fares rose around 4% in the period, contributing to improved per-passenger revenue. Cost control was effective, with operating costs rising at a more modest rate and unit costs remaining stable when excluding exceptional items.

Management highlighted that strong travel demand — especially during peak travel periods such as school breaks and the winter holiday season — underpinned both higher traffic and fare resilience. Fuel hedging remains a key element of expense management, with a large portion of future fuel requirements secured at favorable prices, reducing exposure to energy price volatility.

However, reported profit for the quarter was impacted by an exceptional regulatory fine provision, which significantly reduced net income compared with the prior year when such provisions were absent. Management remains confident that the regulatory charge will be overturned on appeal and has emphasized the underlying profitability on a pre-exceptional basis.

Leadership Insights

Demand and Revenue:

Executives stressed strong forward bookings, pointing to sustained leisure travel appetite as a driver for both load factor and fare improvements. They attributed part of the fare uplift to constrained industry capacity, largely stemming from broader aircraft delivery delays affecting competitors. Management indicated confidence in maintaining fare stability, though with an awareness of competitive pricing pressures in certain markets.

Cost Discipline:

Cost discipline was a recurring theme. The airline’s fuel hedging program — covering a significant portion of its projected fuel needs at locked-in rates — was presented as a buffer against near-term cost inflation and a contributor to lower projected unit costs for the next fiscal year. Management also noted stable unit costs in the quarter, a core pillar of its low-fare value proposition.

Fleet and Operations:

While broader industry aircraft delivery constraints have historically affected capacity growth, Ryanair has begun to take delivery of the final aircraft in its current fleet order, supporting network and schedule reliability. Management expressed confidence in future deliveries, which supports ongoing traffic growth expectations.

Market Perspectives

Analysts and investors sought clarification on near-term demand visibility and cost pressures:

- Demand Visibility: While demand remains strong, visibility in specific future months remains challenging due to competitive pricing movements and broader macroeconomic uncertainty. Management emphasized the importance of maintaining flexibility in capacity planning.

- Cost Inflation and Fuel: Fuel hedging was highlighted as a key tool to mitigate cost volatility. While some non-fuel charges (such as air traffic control fees) are increasing, overall unit cost pressures are manageable.

- Regulatory Charge Impact: The provision taken for the Italian competition authority fine is contingent and subject to appeal. Excluding such charges, operational profitability remains solid.

Overall, management conveyed an optimistic yet pragmatic outlook: demand for travel remains resilient; cost management and hedging provide a solid buffer; and while certain external variables — such as regulatory uncertainties and competitive pricing — persist, the underlying business model remains robust.

Environmental, Product, Route, and Management Considerations

Some additional context is available from the company’s reports:

- Sustainability / CO₂ Reduction: The company highlighted ongoing efforts to improve environmental efficiency, including the delivery of fuel-efficient Boeing “Gamechanger” aircraft, retrofitting older B737NG aircraft with winglets, and a long-term target to reach approximately 50 grams of CO₂ per passenger-km by 2031.

- Route and Network Updates: Over 106 new routes were on sale for Summer 2026, including three new bases. This represents operational expansion but was not discussed in detail.

In short, while Ryanair highlighted operational efficiency and environmental ambitions in its reports, the primary focus remained on demand, fares, cost discipline, fleet, and regulatory considerations.

Forward Guidance and Outlook Considerations

Ryanair reiterated its expectations for continued traffic expansion and revenue resilience into the remainder of fiscal year 2026, highlighting that overall passenger numbers are expected to grow year-over-year. Management continues to monitor cost dynamics and competitive responses closely, with strategic emphasis on preserving its low-cost structure while responding to evolving travel patterns.

The near-term environment is framed by strong consumer demand paired with prudent cost strategies, enabling Ryanair to navigate mixed headwinds with operational discipline and strategic flexibility.