Salesforce, Inc. (NYSE: CRM), a leading provider of cloud-based customer relationship management services, has delivered stable revenue growth in recent years, both organically and supported by acquisitions. The company’s near-term growth strategy is largely focused on monetizing generative AI, primarily by integrating the technology into its Einstein platform.

Stock

Salesforce’s stock entered 2024 on a positive note but lost some momentum in recent weeks. However, it stayed above the 52-week average. The highest-ever value was recorded on March 01, 2024. While the current valuation looks high, CRM seems to be on track to regain the lost strength and set new records this year.

It is estimated that the company’s first-quarter 2025 earnings, excluding special items, jumped to $2.38 per share from $1.69 per share in the comparable period of 2024. It is in line with the forecast issued by the Salesforce leadership. On average, analysts forecast revenues of $9.15 billion for the April quarter. The company is looking for Q1 revenues in the range of $9.12 billion to $9.17 billion. The report is expected to be released on Wednesday, May 29, at 4:00 p.m. ET.

AI Power

Being a market leader with an impressive track record of customer relationship management, Salesforce stands to benefit significantly from the widespread adoption of generative AI across industries. The recent launch of its AI-enabled products should translate into revenues in the coming years. Meanwhile, growth will likely be restricted by cautious enterprise spending on technology due to macroeconomic headwinds.

Over the years, Salesforce has ramped up its ecosystem through strategic acquisitions, including the purchase of Demandware, Mulesoft, Tableau, and Slack. However, economic uncertainties have weighed on performance lately, prompting the company to embark on a cost-cutting program and repurchase shares to strengthen the bottom line.

From Salesforce’s Q4 2024 earnings call:

“At FY ’24, we’ve laid the foundation for success through strategic restructuring, streamlining our go-to-market approach, deeper inspection, and continued operational excellence. As part of our transformation, we also refined and scaled our big deal motion and introduced new product bundles to give our customers comprehensive solutions on a unified, trusted platform. And, we’re unlocking customer spending with new channels like AWS Marketplace and driving C-level relevance through strategic collaboration with McKinsey. The adjustments we made are paying off.”

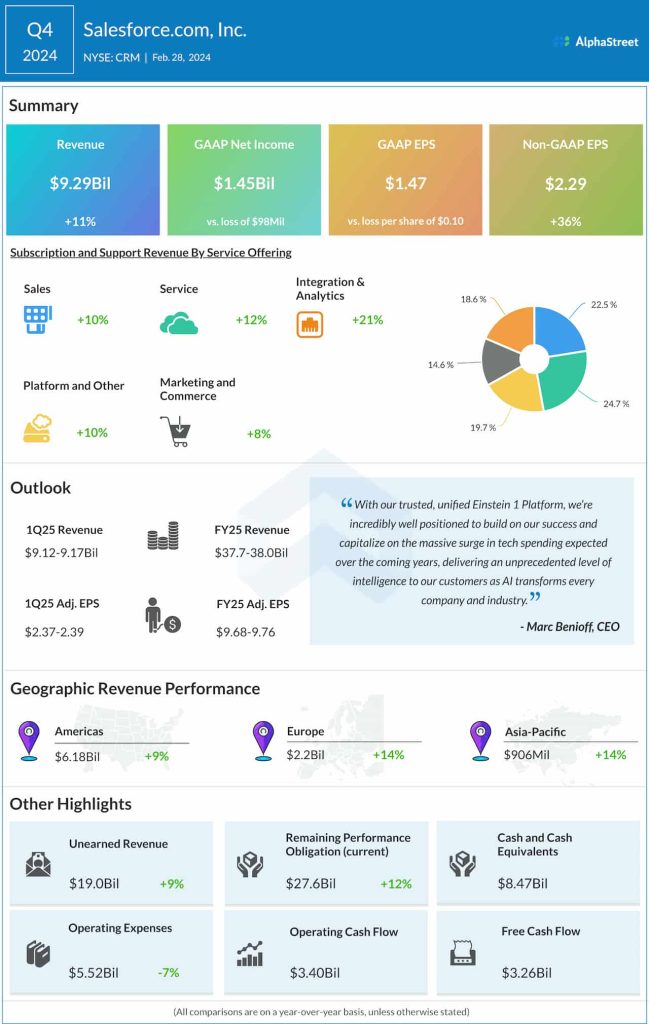

Q4 Numbers Beat

In the fourth quarter, revenues grew 11% annually to $9.29 billion and topped expectations, with all key operating segments registering strong growth. Excluding non-recurring items, January-quarter earnings increased to $2.29 per share from $1.68 per share in the same quarter last year. On an unadjusted basis, the company reported a profit of $1.45 billion or $1.47 per share for Q4, compared to a loss of $98 million or $0.10 per share in the corresponding period of 2023. Interestingly, its quarterly profit has either beaten or matched expectations consistently for over a decade.

For the whole of fiscal 2025, the management projects revenues in the range of $37.7 billion to $38.0 billion. Full-year adjusted profit is expected to be between $9.68 per share and $9.76 per share.

Shares of Salesforce have gained more than 10% since the beginning of 2024. They traded higher throughout Wednesday’s session.