AlphaStreet Newsdesk powered by AlphaStreet Intelligence

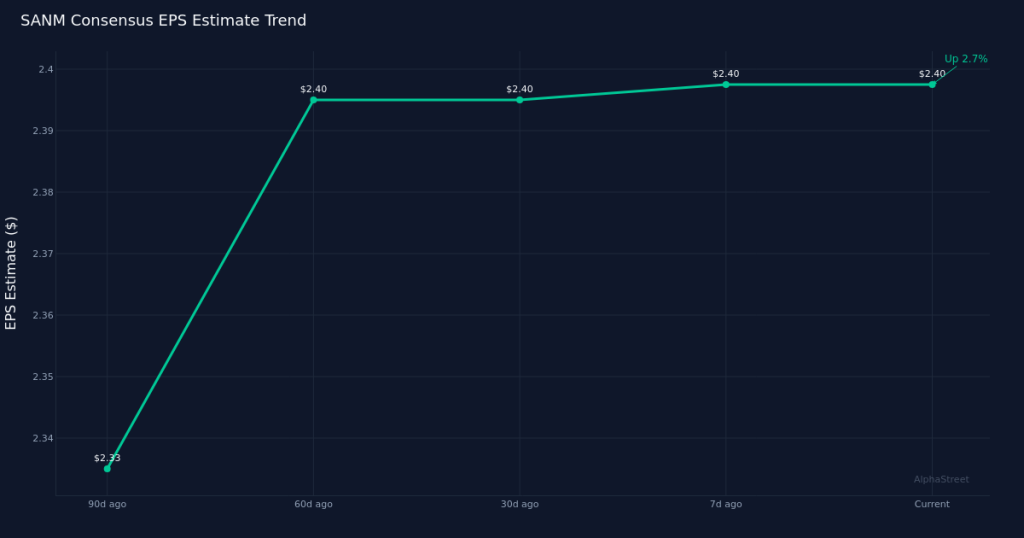

Wall Street expects Sanmina Corporation to report second quarter fiscal 2026 earnings of $2.40 per share on revenue of $3.27B when results are released April 27th. The consensus view is based on estimates from 4 analysts, with EPS projections ranging from $2.35 to $2.44 and revenue forecasts spanning $3.25B to $3.31B. The electronic components manufacturer faces a narrow estimate band, suggesting relative confidence in the business trajectory heading into the print.

Analyst estimate activity shows mixed signals over recent months. While the consensus EPS forecast has remained unchanged at $2.40 over the past 30 days, the 90-day view reveals upward momentum, with estimates rising 3.0% from $2.33 three months ago. This gradual upward revision pattern suggests analysts have been gaining confidence in Sanmina’s earnings power as the quarter progressed, though the stabilization in recent weeks indicates expectations may have settled into a holding pattern ahead of the report.

The year-over-year comparison reveals dramatic top-line acceleration. Consensus revenue of $3.27B would represent a 60.3% increase from the year-ago quarter’s $2.04B, marking extraordinary growth for a contract manufacturer of this scale. In the comparable quarter last year, Sanmina generated net income of $83.6M on a net margin of 4.1%, providing a baseline for profitability expectations. The magnitude of the implied revenue expansion raises questions about whether this growth is organic, acquisition-driven, or reflects new program ramps with key customers. Equally important will be whether the company can maintain or expand margin structure while scaling at this pace, as contract manufacturing businesses often face margin pressure during rapid growth phases.

Sanmina operates in the highly cyclical electronics manufacturing services sector, where visibility into customer demand patterns and inventory dynamics will be critical. The company serves diverse end markets including industrial, medical, defense, and communications infrastructure, providing both design and manufacturing services. Investors will scrutinize commentary around end-market demand trends, particularly given the broader uncertainty in technology hardware spending. The ability to manage working capital efficiently while supporting the implied growth rate will be a key indicator of operational execution, as EMS providers must carefully balance inventory positioning against customer forecast volatility.

The stock’s positioning heading into the report provides context for investor expectations. Where shares trade relative to recent ranges will influence how the market interprets results, with any meaningful deviation from consensus likely to trigger volatility given the concentrated analyst coverage. The relatively tight estimate range suggests limited room for error, as even modest misses or beats could move shares significantly when only 4 analysts are providing forecasts.

Margin trajectory will be as important as the headline revenue and earnings figures. Given the year-ago net margin of 4.1%, investors will closely examine whether Sanmina has been able to leverage the substantial revenue growth into margin expansion or whether competitive dynamics and input costs have kept profitability relatively constrained. The company’s ability to translate top-line momentum into bottom-line performance will signal the quality and sustainability of the growth, particularly important in a business model where scale advantages should theoretically improve operating leverage.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.