RXO Stock Drops Following Larger-Than-Expected Quarterly Loss

Shares of RXO Inc (RXO) fell 6.76% to $15.46 in midday trading on Friday after the company reported fourth-quarter 2025 results that missed earnings expectations despite a slight revenue beat. The stock gapped down from its previous close of $16.58, opening at $15.35 as investors reacted to compressed margins. RXO currently trades significantly below its 52-week high of $22.17, following a volatile year marked by prolonged freight market softness.

Company Description: RXO Inc is a leading North American provider of asset-light transportation solutions, primarily focused on tech-enabled truck brokerage. The company operates three main segments: Truck Brokerage, Managed Transportation, and Last Mile delivery. Its business model leverages the proprietary RXO Connect digital platform to match shipper demand with carrier capacity across retail, e-commerce, and industrial end markets.

Current Stock Price: $15.46 (Midday, Feb 6, 2026)

Market Capitalization: Approximately $2.72 billion

Valuation: RXO currently trades at a trailing P/E ratio of -37.8x due to recent GAAP losses. The valuation reflects a market focus on adjusted EBITDA leverage and the potential for a freight cycle recovery, though multiples remain elevated relative to current depressed earnings.

Margin Compression Intensifies Despite Top-Line Resilience

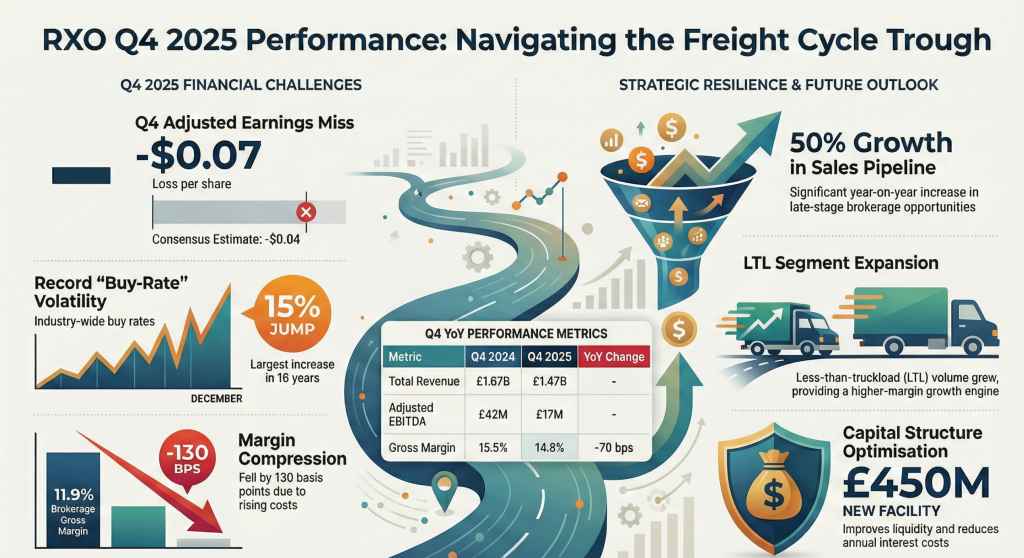

RXO reported fourth-quarter 2025 revenue of $1.47 billion, a 11.9% decrease from $1.67 billion in Q4 2024. Adjusted EBITDA fell to $17 million, a 59.5% decline from $42 million in the prior-year period. The firm posted an adjusted diluted loss of $0.07 per share, wider than the analyst consensus of a $0.04 loss.

| Metric | Q4 2024 | Q4 2025 | YoY Change |

| Total Revenue | $1.67B | $1.47B | -11.9% |

| Adjusted EBITDA | $42M | $17M | -59.5% |

| Gross Margin | 15.5% | 14.8% | -70 bps |

| Brokerage Margin | 13.2% | 11.9% | -130 bps |

Full-year 2025 revenue totaled $5.7 billion, while adjusted EBITDA reached $109 million with a 1.9% margin. The brokerage segment faced a “pronounced margin squeeze” in December as industry-wide buy rates jumped 15% month-over-month—the largest such increase in 16 years—outpacing the firm’s ability to adjust contractual sale rates. Brokerage volume declined 4% year-over-year, as a 12% drop in truckload volume offset a 31% gain in less-than-truckload (LTL).

2026 Guidance and Liquidity Refinancing

RXO issued first-quarter 2026 adjusted EBITDA guidance of $5 million to $12 million, down from $22 million in Q1 2025. The outlook factors in a $2 million headwind from Winter Storm Fern in January and assumes continued weak demand. Management projects Q1 brokerage volume to decline 5% to 10% year-over-year with gross margins between 11% and 13%.

The company finalized a new $450 million asset-based lending (ABL) facility in February 2026, replacing its previous $600 million revolver. The new facility improved interest rates by 35 basis points and is expected to save $400,000 annually in unused commitment fees. Despite current headwinds, management highlighted a late-stage brokerage sales pipeline that has grown 50% year-over-year.

Geopolitical and Sector Risks

While RXO operates primarily in North America, its clients are subject to broader geopolitical and trade risks. Any implementation of 25% blanket tariffs on imported industrial or retail goods could significantly disrupt shipping volumes in the firm’s Last Mile and Managed Transportation segments.

The firm is currently navigating a “cyclical trough” in the freight market characterized by excess carrier capacity and regulatory-driven buy-rate volatility. Management noted that while its asset-light model provides flexibility, rapid spikes in purchased transportation costs remain a primary risk to near-term profitability.

RXO Inc (RXO) SWOT Analysis

Strengths

- Scale & Technology: Proprietary AI-driven platform has increased broker productivity by 19% year-over-year.

- Liquidity Refinancing: New $450M ABL facility improves capital structure flexibility and lowers financing costs.

- Sales Pipeline: Strong momentum with a 50% increase in late-stage brokerage opportunities and $200M in new Managed Transportation awards.

Weaknesses

- Margin Vulnerability: Significant exposure to sudden “buy-rate” spikes in December led to a 130 bps drop in brokerage gross margin.

- Earnings Volatility: Q4 adjusted loss of $0.07 missed consensus by 75%, highlighting difficulty in forecasting during freight troughs.

- Truckload Concentration: A 12% decline in truckload volume continues to weigh heavily on total brokerage performance.

Opportunities

- Cycle Inflection: High operating leverage means modest increases in spot market loads could significantly boost EBITDA margins.

- LTL Expansion: The 31% growth in LTL volume represents a higher-margin growth engine within the brokerage segment.

- AI Efficiency: Continued scaling of “agentic capacity sourcing” tools aims to structurally lift long-term throughput.

Threats

- Prolonged Freight Softness: Q1 2026 guidance suggests a continued weak environment with volumes expected to drop up to 10%.

- Macro/Tariff Risk: Potential trade decoupling or tariffs could disrupt the retail and industrial volumes that drive RXO’s revenue.

- Weather Disruptions: Q1 earnings are already pressured by a $2M EBITDA impact from early-year winter storms.