International Business Machines Corporation (NYSE: IBM) has been busy streamlining the business through various initiatives including the separation of its managed infrastructure services business Kyndryl. But the company’s recent performance shows that economic uncertainties and currency headwinds are taking a toll on its core businesses.

When the recent selloff battered technology stocks, IBM was not spared and the stock went through a series of ups and downs. However, the shares bounced back after every dip and hit an all-time high a few months ago. It is a top dividend-paying stock with a bigger-than-average yield of about 5%, after regular dividend hikes. Though there are multiple factors in favor of the stock, like the hybrid cloud and AI push which are considered high-growth areas, some investors might find the valuation slightly high.

Buy It?

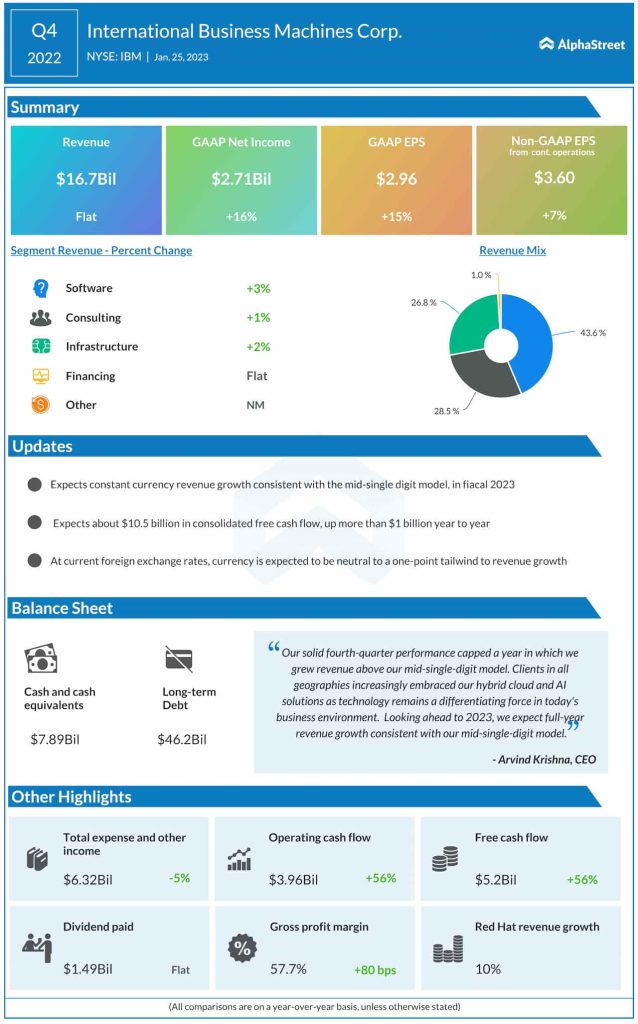

But long-term investors wouldn’t be disappointed since IBM is one of the most stable tech companies that has successfully withstood challenges in the past. Moreover, the company has maintained strong liquidity, and the management is looking for free cash flows of about $10.5 billion for fiscal 2023, which is up more than $1 billion year-over-year. That will help the company pursue the goal of investing big in innovation and also return cash to shareholders.

Q1 Report Due

After posting flat revenues and modest earnings growth for the fourth quarter, the tech firm is expected to report a decline in profit for the first quarter. Analysts are looking for earnings of $1.25 per share, which is down 11% from last year. It is estimated that revenues edged up to $14.36 billion. The results will be published on April 19 after the closing bell.

From IBM’s Q4 2022 earnings conference call:

“Looking at the first quarter, our constant currency revenue growth should be fairly consistent with the full year. Reported growth will also include about a 3-point currency headwind at current spot rates. With operating leverage, we’d expect operating pre-tax margin to expand 50 basis points to 100 basis points in the first quarter, and that’s before the charge I just mentioned for the remaining stranded costs. Given the timing of currency and stranded cost dynamics, we’d expect about one-third of our net income in the first half and about two-thirds in the second half.”

Key Numbers

In the past six years, quarterly profit topped, or matched, expectations consistently and the trend is expected to continue this time. In the final months of 2022, though the main business segments – Software, Consulting, and Infrastructure – grew modestly, that was not sufficient to lift the top line, which remained unchanged at $16.7 billion. However, adjusted profit moved up 7% annually to $3.60 per share.

The stock’s performance ahead of the earnings release has not been very encouraging. It closed Wednesday’s session lower, extending the downtrend seen since the beginning of the year.