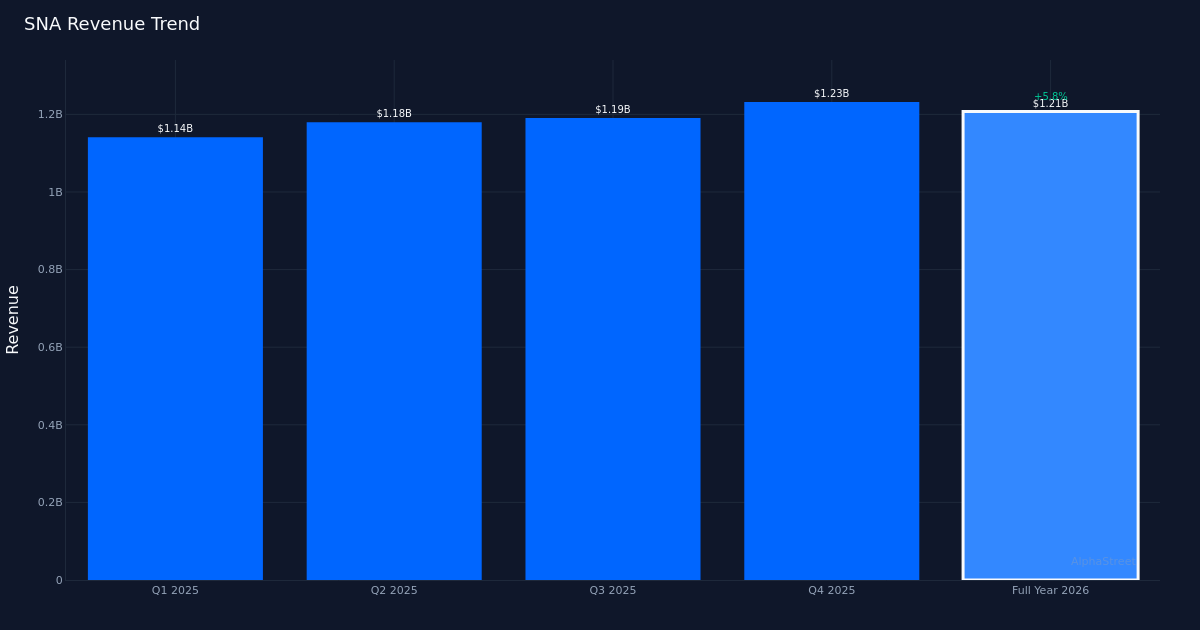

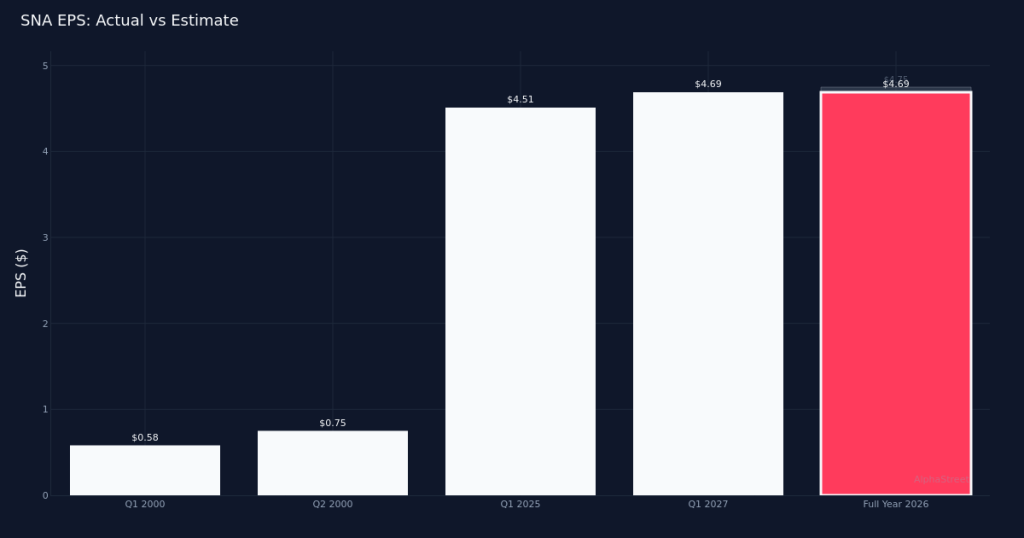

Mixed results. Snap-on Incorporated (NYSE:SNA) delivered a split quarter for Q1 2026, with diluted EPS of $4.69 missing the $4.75 consensus estimate by 1.3%, while revenue of $1.21B exceeded the $1.18B forecast by 2.5%. The stock traded largely unchanged following the announcement, suggesting investors found little to get excited about in the modest earnings shortfall offset by the top-line beat. Bottom-line profit came in at $247.0M as the tools and accessories manufacturer continued to navigate a challenging industrial environment.

Revenue quality solid. The 5.8% year-over-year revenue increase from the $1.14B recorded in Q1 2025 appears to reflect genuine demand strength rather than purely financial engineering. Organic sales growth of 3.4% for the quarter demonstrates that the company is winning business in its core markets, though the gap between reported and organic growth suggests acquisitions or currency tailwinds played a supporting role. Year-over-year, EPS moved up 4.0% from the $4.51 posted in Q1 2025, a respectable showing but one that lagged revenue growth, pointing to margin pressure somewhere in the business model.

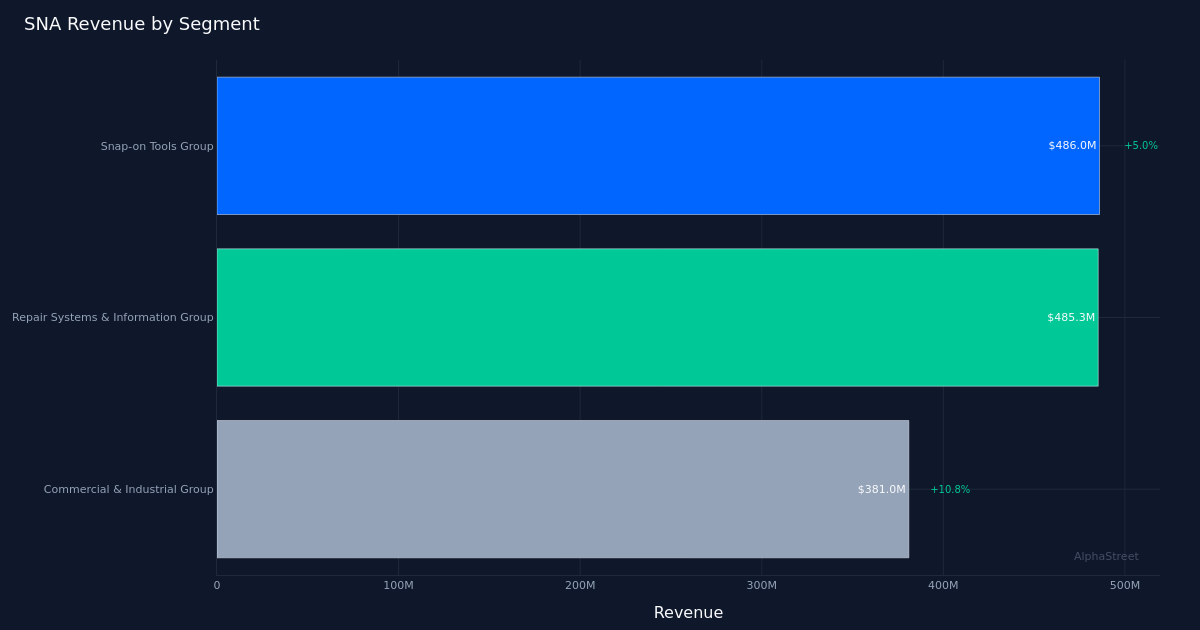

Franchise network drives. The Snap-on Tools Group segment led the charge with $486.0M in revenue, up 5.0% year-over-year, underscoring the continued strength of the company’s franchise distribution model. This channel remains the crown jewel of Snap-on’s portfolio, connecting directly with automotive technicians and other professional tool users through a network of mobile van dealers. The segment’s outperformance relative to the company’s organic growth rate suggests solid execution at the point of sale, though the earnings miss indicates that strength at the top line didn’t fully translate to the bottom line.

Analyst sentiment cautious. Wall Street consensus stands at 5 buy, 7 hold, and 1 sell, reflecting a measured view of the company’s prospects. The hold-heavy rating distribution suggests analysts see limited upside at current valuations, particularly given the modest earnings miss and the relatively subdued stock reaction. With the shares trading flat after the announcement, the market appears to be taking a wait-and-see approach, neither penalizing the EPS shortfall nor rewarding the revenue beat with any enthusiasm.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.