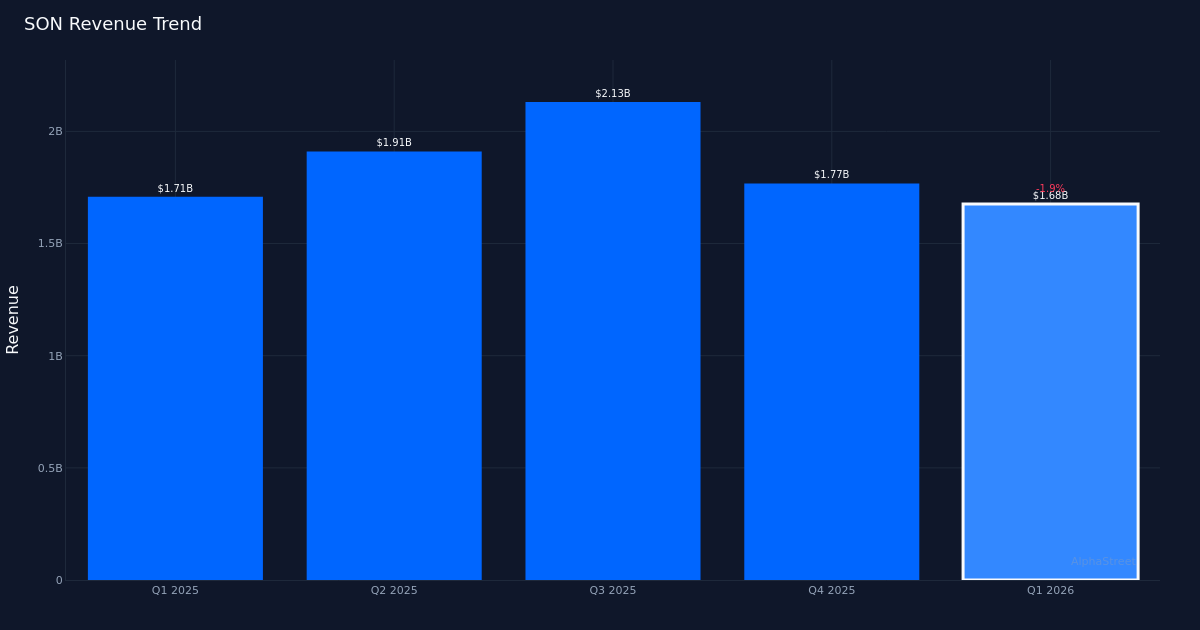

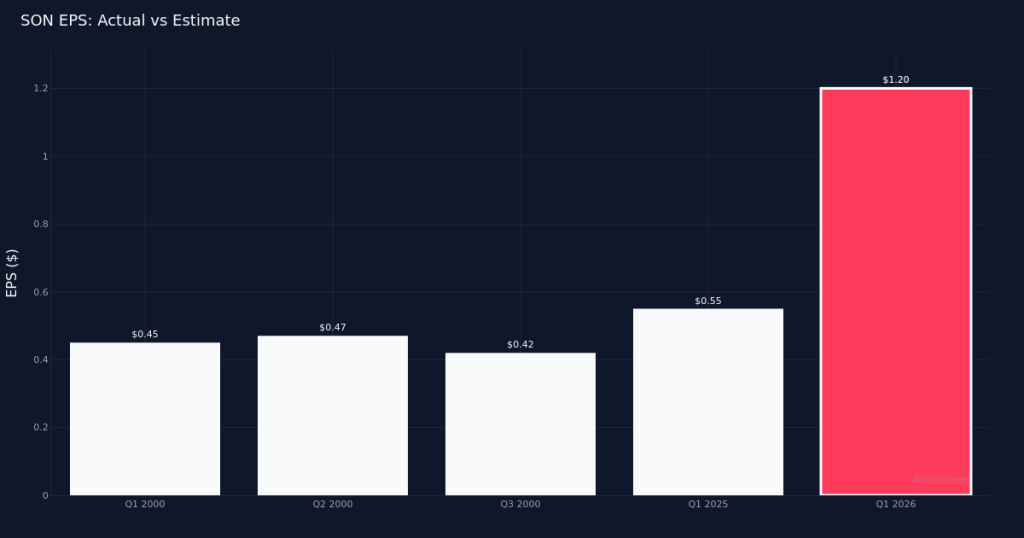

Mixed Quarter. Sonoco Products Company (NYSE:SON) delivered Q1 2026 adjusted diluted EPS of $1.20, precisely matching the $1.20 consensus estimate from 10 analysts, though revenue of $1.68B fell short of the $1.71B forecast by 2.0%. The packaging and containers manufacturer posted bottom-line profit of $119.4M while navigating a challenging demand environment that pressured top-line growth. Shares traded largely unchanged following the release, suggesting investors had largely anticipated the revenue shortfall.

Revenue Decline. The company’s $1.68B in quarterly revenue represents a 1.9% decrease from the $1.71B recorded in Q1 2025, reflecting ongoing headwinds in certain end markets. While the earnings match demonstrated operational discipline, the nature of this performance—meeting profit expectations amid declining revenue—suggests margin expansion through cost management rather than organic volume strength. Adjusted EBITDA reached $276M for the quarter, underscoring management’s focus on protecting profitability even as the top line contracted year-over-year.

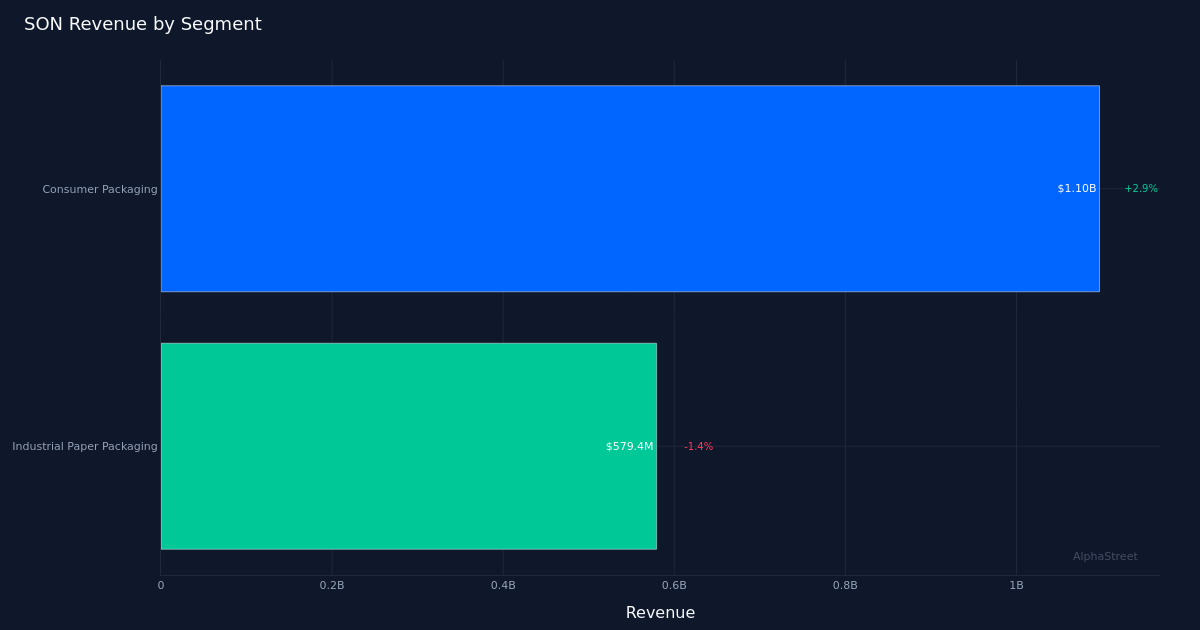

Segment Performance. Consumer Packaging emerged as the bright spot, leading the company’s portfolio with $1.10B in revenue and posting 2.9% year-over-year growth. This segment’s performance partially offset weakness elsewhere in the business and demonstrates Sonoco’s strategic positioning in consumer-facing packaging solutions. The company maintained a workforce of 22,000 total employees at quarter end as it balances operational efficiency with the capacity to serve customer demand across its diversified platform.

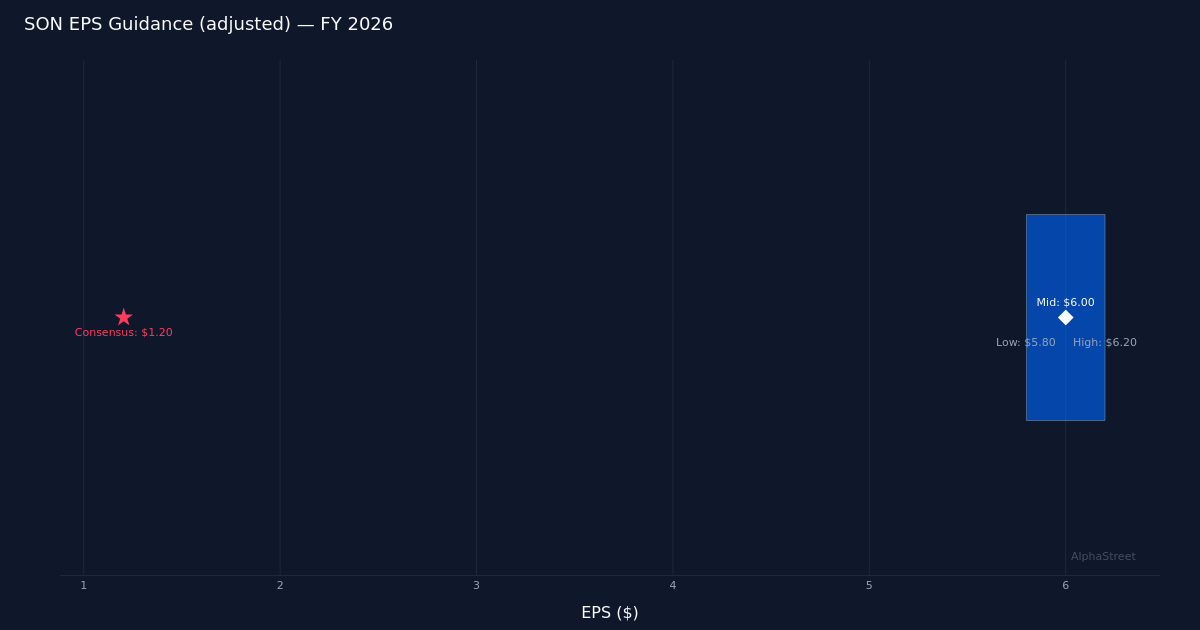

Guidance Signals Optimism. Management projected FY 2026 adjusted EPS in the $5.80 to $6.20 range, with revenue expected between $7.25B and $7.75B for the full year. The midpoint of the earnings guidance suggests sequential improvement from the current quarterly run rate, indicating that leadership anticipates stronger performance in the quarters ahead. This outlook provides meaningful context to the Q1 miss, framing it as a temporary soft patch rather than an enduring trend. The revenue guidance range implies management expects conditions to stabilize as the year progresses, with potential for returning to growth.

Analyst Sentiment. Wall Street consensus currently stands at 4 buy ratings, 7 hold ratings, and 0 sell ratings, reflecting a cautious but constructive view on the stock. The absence of sell ratings suggests analysts see limited downside risk, while the hold-heavy distribution indicates most are taking a wait-and-see approach on whether the company can reaccelerate revenue growth and reach the upper end of its full-year guidance range.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.