AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Wall Street expects Southside Bancshares to post modest growth when the regional bank reports first-quarter 2026 results on April 30. The consensus among four analysts calls for earnings of $0.76 per share on revenue of $70.9M. Estimates show tight clustering, with EPS projections ranging from $0.76 to $0.77 and revenue forecasts spanning $70.6M to $71.3M, suggesting limited disagreement about the bank’s near-term trajectory.

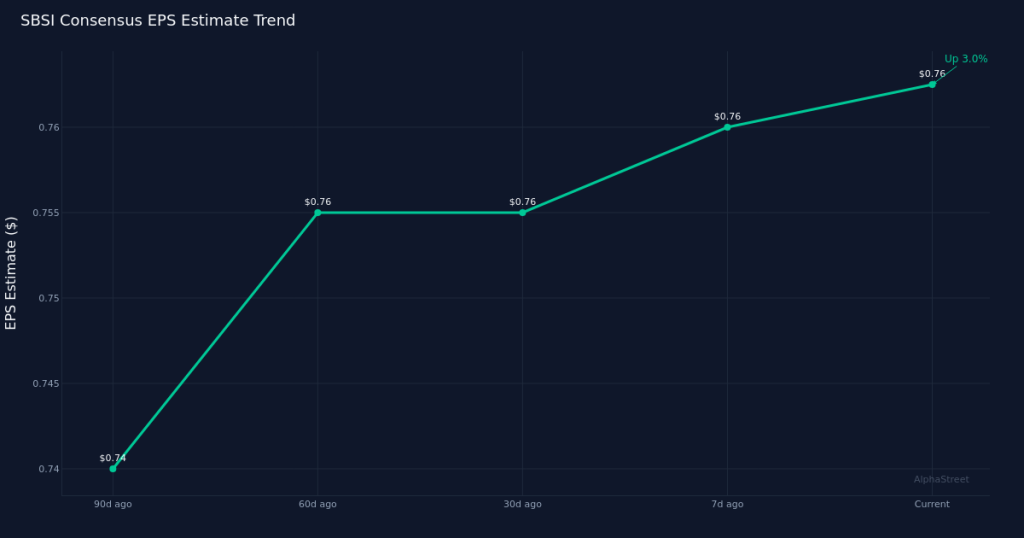

Analyst estimate revisions paint a picture of stable but gradually improving expectations. The EPS consensus has held flat over the past 30 days at $0.76, indicating no material change in sentiment as the report approaches. The 90-day view reveals more optimism, with estimates climbing up 2.7% from $0.74 three months ago. This modest upward drift suggests analysts have grown incrementally more confident in Southside’s ability to navigate the current interest rate environment and credit conditions, though the lack of movement in recent weeks implies that confidence has plateaued rather than accelerated.

The consensus implies solid year-over-year growth across both the top and bottom lines. Compared to first-quarter 2025 results, when Southside earned $0.71 per share on revenue of $67.0M, the Street’s forecast represents implied EPS growth of 7.0% and revenue expansion of 5.8%. A year ago, the bank generated net income of $21.1M and posted a net margin of 31.5%, reflecting the strong profitability profile typical of well-managed regional banks. Whether Southside can maintain or expand that margin level while growing revenue will be a key indicator of operating leverage and pricing power in its deposit and loan portfolios.

The regional banking sector faces a complex backdrop heading into earnings season. Banks have been managing the dual challenges of a still-elevated but potentially peaking interest rate environment and ongoing concerns about commercial real estate exposure. For Southside, investors will be looking for signals about net interest margin trends, deposit competition and pricing, and credit quality metrics. The ability to grow loans while maintaining disciplined underwriting standards, particularly in commercial real estate categories that have faced pressure across the industry, will be critical to sustaining the growth implied by consensus estimates.

Deposit dynamics warrant close attention given industrywide pressures on funding costs. Regional banks have faced intense competition for deposits as customers have become more rate-sensitive and willing to move funds to higher-yielding alternatives. How Southside has managed its deposit mix—the balance between non-interest-bearing and interest-bearing accounts, and the pricing discipline required to retain customers without eroding margins—will provide insight into the sustainability of its profitability. Any commentary on deposit flows, customer retention, and the competitive environment in the bank’s Texas-based markets will help frame expectations for the remainder of the year.

Credit quality indicators will be scrutinized for signs of stress or resilience. While the verified data does not include prior quarter specifics on loan loss provisions or non-performing assets, these metrics typically drive sentiment for regional bank stocks. Investors will parse management’s commentary on the loan portfolio, particularly any segments showing deterioration or improvement, and whether reserve levels remain adequate given the economic environment. The bank’s exposure to specific industries and geographies within its footprint could differentiate its performance from peers.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.