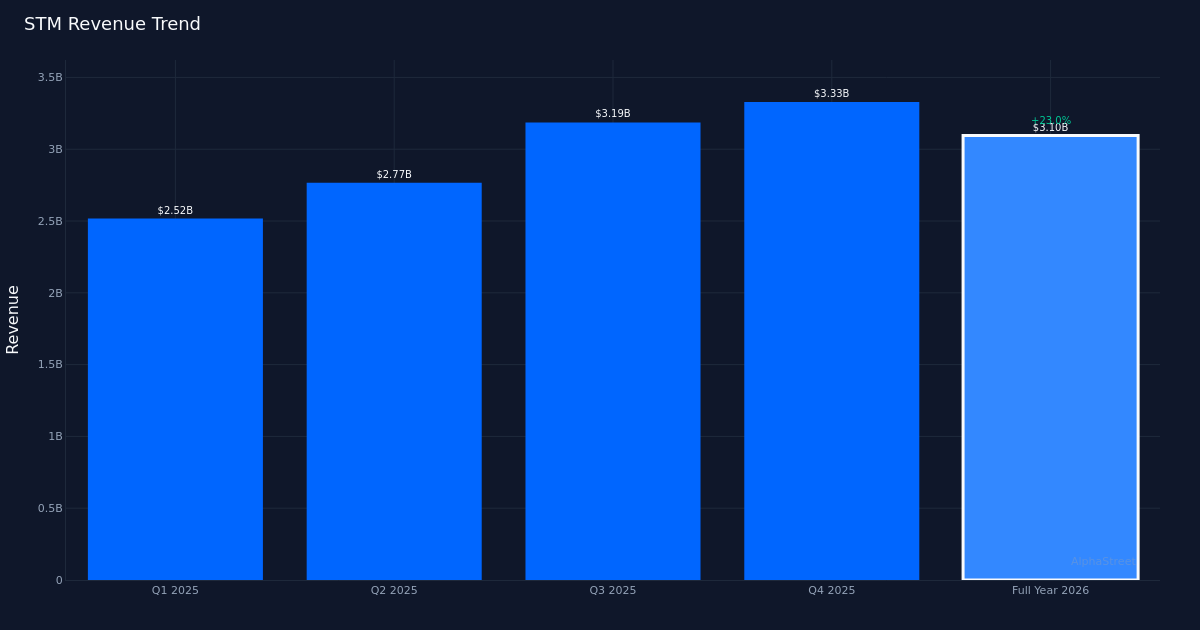

STMicroelectronics delivered a paradoxical Q1 2026 result that encapsulates the semiconductor industry’s current malaise: revenue growth has returned after a brutal downturn, yet profitability remains devastatingly compressed. The company posted $3.10B in revenue, beating estimates by 1.5% and marking 23.0% year-over-year growth, but earnings of $0.13 per share missed expectations by 27.8%. This divergence between top-line recovery and bottom-line weakness reveals fundamental margin pressure that revenue momentum alone cannot mask.

The earnings quality story is troubling despite the year-over-year comparisons appearing favorable on surface. While EPS of $0.13 represents an 85.7% increase from the year-ago $0.07, that comparison flatters a deeply challenged profitability profile. Net margin deteriorated from 2.5% a year ago to just 1.2% currently, a contraction of 1.3 percentage points even as revenue surged 23.0%. Net income of $37.0M on $3.10B in sales underscores the severity of margin compression—the company is barely profitable despite strong volume growth. Gross margin of 33.8% provides some cushion, translating to $1.04B in gross profit, but the collapse from gross to operating margin (2.3% operating margin yielding just $70.0M in operating income) signals bloated operating expenses consuming nearly all gross profitability.

The sequential revenue trajectory reveals underlying volatility that tempers enthusiasm about the growth narrative. The four-quarter trend shows $3.10B following $3.33B in Q4 2025, $3.19B in Q3 2025, and $2.77B in Q2 2025—a pattern that defies clean characterization. The sequential decline from Q4’s $3.33B to Q1’s $3.10B represents meaningful lost momentum, even accounting for typical seasonal patterns.

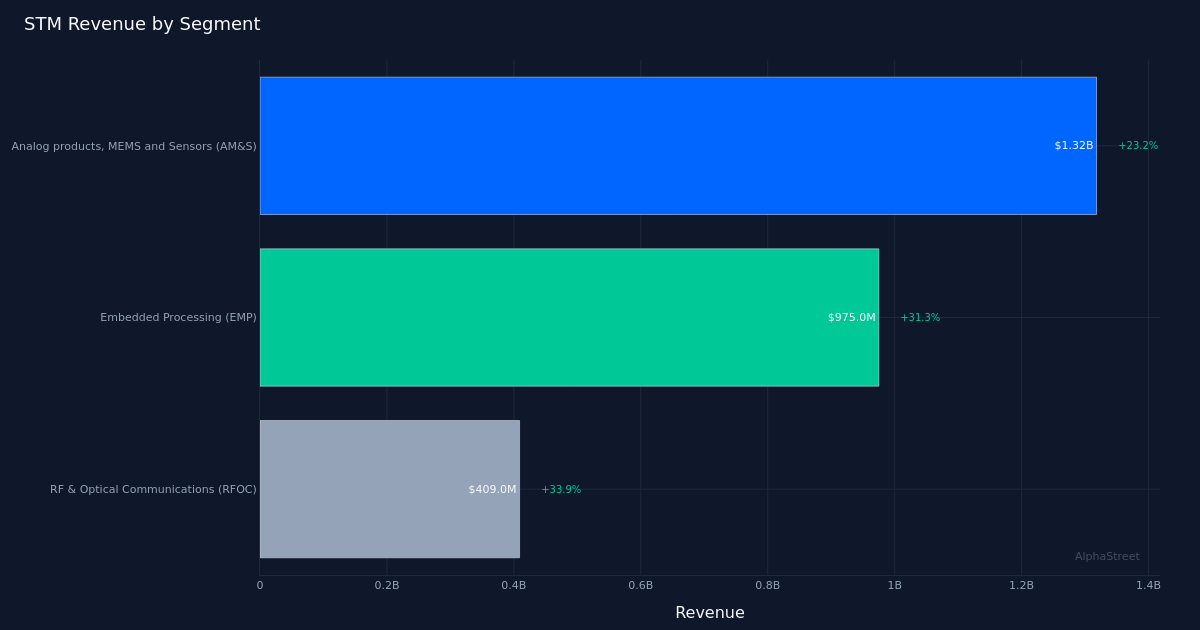

Segment performance demonstrates broad-based growth with RF & Optical Communications leading the charge. The RFOC segment delivered $409.0M with 33.9% growth, the strongest performer among the three reportable units. Embedded Processing generated $975.0M with robust 31.3% growth, while Analog products, MEMS and Sensors—the largest segment at $1.32B—posted 23.2% growth. Management noted that “our first quarter net revenues were $3.1 billion, including about $40 million revenues associated with NXP’s MEMS sensor business, which we acquired during the quarter,” providing important context that organic growth excluding the NXP MEMS sensor business was 21.4%. The relative outperformance of RFOC and Embedded Processing versus AM&S suggests strength in communications infrastructure and industrial applications, though without prior-period segment data, assessing whether this represents acceleration or normalization remains impossible.

Management’s forward guidance on data center revenue provides a concrete anchor for the growth thesis. The company confirmed “data centers revenue expectation to be nicely above $500 million for 2026 and well above $1 billion for 2027,” with subsequent reaffirmation stating “we confirm the revenue nicely well above $500 million.” This guidance matters because it quantifies STMicroelectronics’ participation in the AI infrastructure buildout that has enriched other semiconductor players. If data center revenue exceeds $500M for full-year 2026, it would represent meaningful diversification from the automotive and industrial end markets that have pressured results. The doubling trajectory implied for 2027—moving from “nicely above $500 million” to “well above $1 billion”—suggests management sees accelerating design wins converting to revenue.

The stock’s post-earnings gain reflects investor relief and enthusiasm. Markets evidently focused on the revenue beat and year-over-year growth resumption while looking past the earnings miss and margin deterioration. The positive reaction despite a 27.8% EPS miss suggests expectations had reset sufficiently low that any revenue growth qualified as victory.

STMicroelectronics finds itself in the uncomfortable position of growing its way toward profitability rather than from profitability. The return to year-over-year revenue growth after a downturn provides narrative momentum, and the data center revenue trajectory offers a compelling future story. Yet the margin structure—net margins barely above 1%—leaves virtually no room for execution missteps or pricing pressure. The company must demonstrate that gross margin improvement from current 33.8% levels can flow through to operating and net income, not get absorbed by operating expense expansion.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.