More than two years into the pandemic, the healthcare sector remains under stress due to continuing COVID care activities and hospitalizations. However, the recent improvements in the pandemic situation and rebound in elective procedures are having a positive effect on the performance of medical device companies like Medtronic plc (NYSE: MDT).

The Dublin-based company, which is the largest medical device maker in the world, generates revenues from its Cardiovascular, Medical-Surgical, Neuroscience, and Diabetes segments. Of late, it has been making great strides in robot-assisted surgery — the healthcare segment that is rapidly gaining popularity due to minimally invasive procedures and shorter recovery time – giving competition to others like Intuitive Surgical, Inc. (NASDAQ: ISRG). Medtronic’s extensive global presence and strong growth prospects in emerging markets put the company in an advantageous position compared to its peers.

Valuation

After a losing streak that lasted for about a year, Medtronic’s stock has become cheaper. The company has a dividend yield that is much higher compared to the average for the industry, attracting retirement investors to the stock. The management has hiked the dividend almost every year, maintaining a decent payout ratio. Experts are optimistic about the stock’s future performance and have expressed hope of double-digit growth in the coming months.

Read management/analysts’ comments on quarterly reports

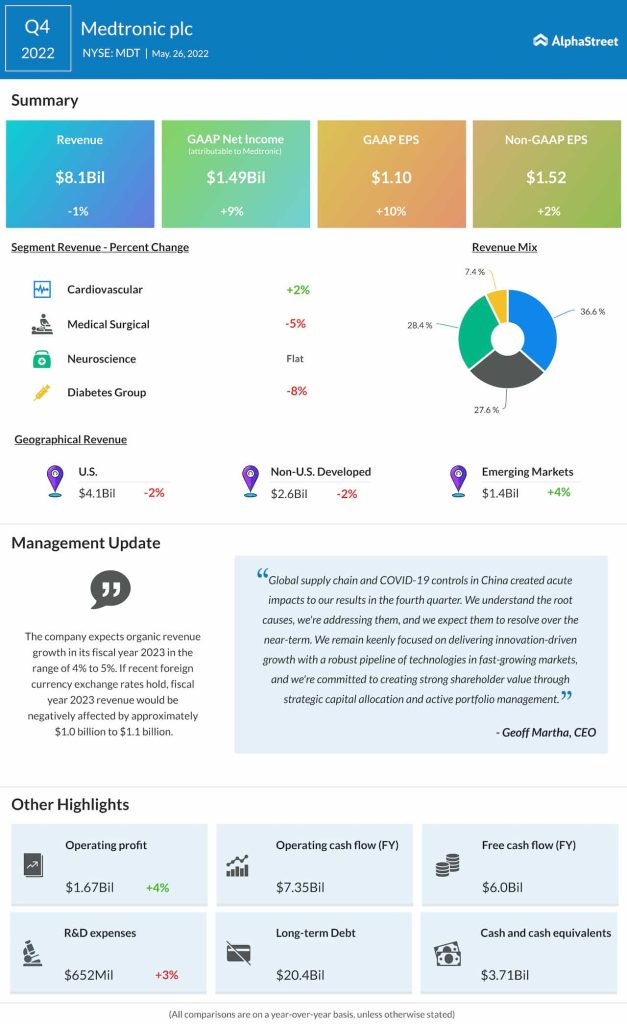

Geoff Martha, CEO of Medtronic, said in a statement last week, “Our pipeline is robust and continues to advance with a number of upcoming catalysts and fast-growing Medtech markets. We’re committed to creating strong returns for our shareholders, and we’re making progress with our enhanced portfolio management and our capital allocation processes. We’re investing in future growth drivers, while at the same time returning capital primarily through our meaningful and growing dividend.”

Reflecting the unfavorable market conditions, net revenue declined modestly to about $8 billion in the final three months of fiscal 2022. A modest increase in the core cardiovascular segment was more than offset by weakness in the other divisions. Adjusted earnings moved up 2% annually to $1.52 per share. The results fell short of expectations, as they did in the previous quarter. The strong organic growth and improvement in margin performance are reflective of the underlying strength of the business.

Strategy

The supply chain bottlenecks and fresh COVID-related curbs in China, which account for nearly half of the company’s emerging market revenues, remain a challenge when it comes to maintaining the growth momentum. Meanwhile, the management has initiated steps to deal with the situation and expects to resolve the issues in the near term. Currently, the strategy is focused on maintaining a strong pipeline of technologies in key markets and enhancing shareholder value through prudent capital allocation.

Is Merck & Co. a good investment after Q1 earnings?

The company recently came under regulatory scrutiny amid concerns over the safety and quality of its products in the diabetics business. This month, Medtronic’s shares slipped below the $100-mark for the first time in more than two years. The stock closed the last trading session higher, after losing 5% in the past 30 days.