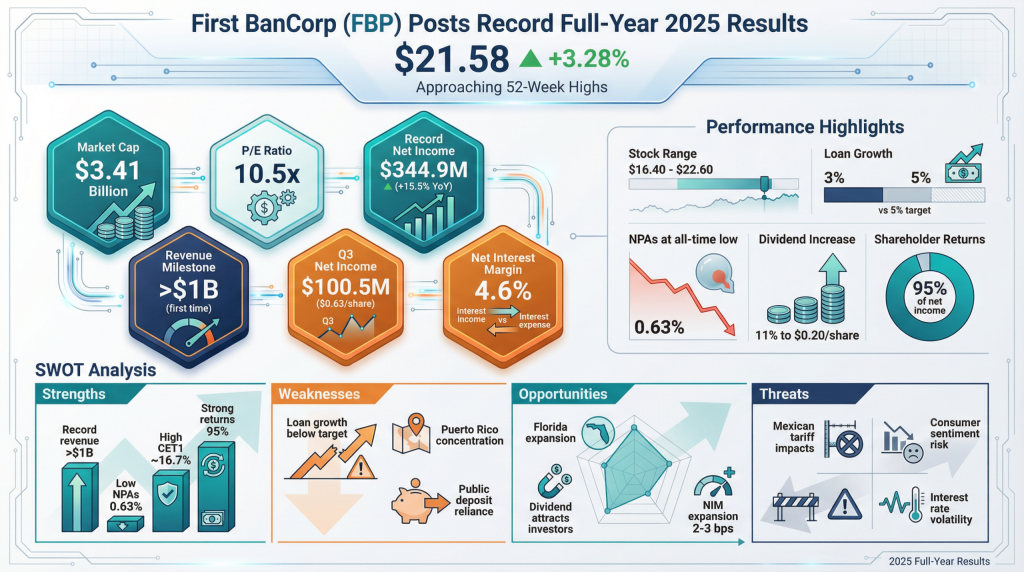

Despite record annual earnings, First BanCorp (FBP) management has moderated its loan growth outlook into 2026. Total loans grew by 3% in 2025, falling slightly below the original 5% target due to elevated commercial loan payoffs and a deceleration in consumer production during the second half of the year. Management has reiterated a conservative organic loan growth target of 3% to 5% for the coming year, focusing on maintaining its efficiency ratio at or below 52%.

The broader financial sector continues to grapple with macro pressures that vary by industry. While software and SaaS firms face “seat-count” rationalization and extended sales cycles, regional banks like First BanCorp (FBP) are managing “lumpy” commercial activity. The bank’s non-performing assets (NPAs) reached an all-time low of 63 basis points in late 2025, indicating that credit quality remains decoupled from the volatility seen in high-growth technology sectors.

Analyst sentiment remains cautiously optimistic. On January 27, 2026, several research notes highlighted the bank’s 11% dividend hike to $0.20 per share as a sign of balance sheet strength. While no major downgrades occurred today, price targets from firms such as UBS and Wells Fargo remain centered between $23.00 and $25.00, suggesting modest upside from current levels as the bank continues its share buyback program, which returned approximately 95% of net income to shareholders in 2025.