Bristol Myers Squibb Company (NYSE: BMY) is thriving on its multi-pronged growth plan, based on strategic acquisitions and the promising pipeline. Recently, the pharma giant jumped on the COVID vaccine bandwagon through a strategic partnership to develop a therapy that combines multiple antibodies.

Read management/analysts’ comments on quarterly reports

A Winning Model

In the past two years, the New York-based healthcare firm generated quarterly profit that consistently exceeded the market’s projection. Its cardiovascular portfolio got a major boost from the recent buyout of heart-drug maker MyoKardia, the biggest deal after the acquisition of biopharma firm Celgene two years ago. A patent lawsuit that was settled in favor of Celgene’s multiple myeloma drug Revlimid has eased concerns of generic threat, for the time being.

“Thanks to excellent execution throughout the year, we have continued to deliver on all value drivers of the Celgene acquisition and laid a strong foundation for the future growth of our new company. We are well-positioned to accelerate the renewal of our portfolio and support the long-term growth of our business. …The integration of Celgene has gone very well. Based on progress last year, we now expect total synergies to be close to $3 billion by the end of ’22. We have proven commercial capabilities, which enable us to fully realize the opportunities to grow our in-line portfolio and support strong execution of our launches,” said Bristol-Myers’ CEO Giovanni Caforio during his interaction with analysts at this week’s earnings conference call.

Road Ahead

It is estimated that newly launched products would account for about 30% of the company’s total revenues by 2025. Also, with continued R&D initiatives and investments in the business, the pipeline is expected to grow significantly during that period. The major upcoming milestones this year include proof-of-concept data for deucravacritinib in ulcerative colitis, mavacamten phase-II data for Factor XIa, and initial data for iberdomide in refractory multiple myeloma.

Overall, the market is bullish on the company’s growth prospects. Interestingly, the virus-induced disruption did not stop the management from expanding the portfolio further. After the recent pull-back, Bristol Myers’ stock price looks favorable, with experts predicting a near-term rebound and a double-digit increase this year. BMY offers a unique buying opportunity that can yield handsome returns. Analysts’ consensus rating this week is strong buy.

Broad Based Growth

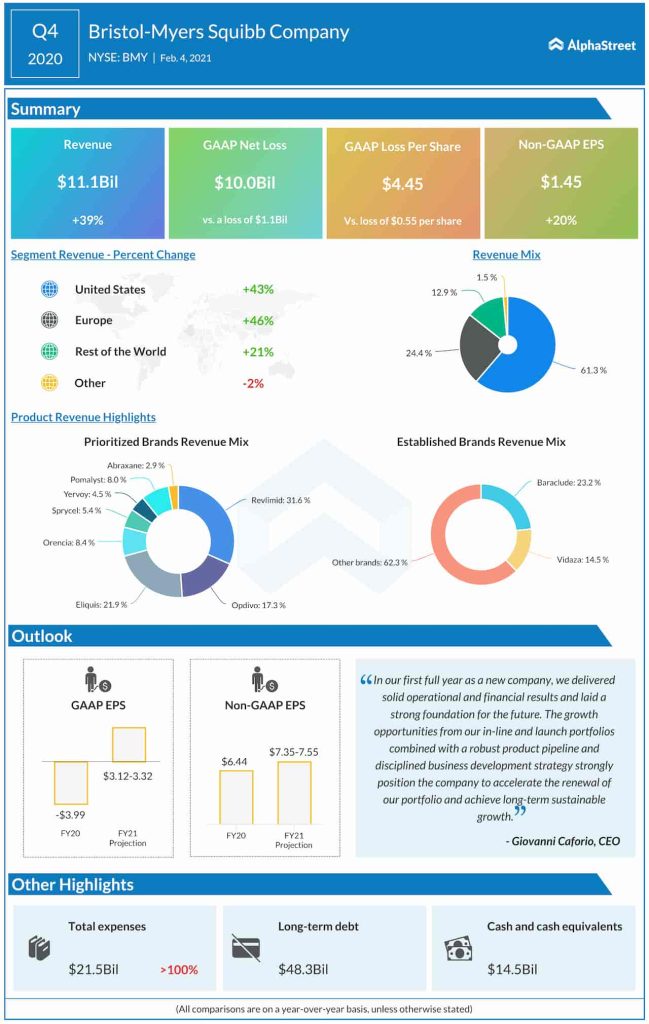

In the fourth quarter, reported results were negatively impacted by a significant one-time charge related to the $13-billion acquisition of MyoKardia, Inc. (MYOK), a clinical-stage biopharmaceutical company focused on therapies for the treatment o cardiovascular diseases. Consequently, Bristol Myers incurred a loss of $10 billion or $4.45 per share, on an unadjusted basis. Excluding the one-off items, it earned $1.46 per share, which represented a 20% year-over-year increase. There was a 39% growth in revenues to around $11 billion, thanks to the double-digit growth across all geographical segments.

The stock, which slipped below $50 early last year, made a quick recovery since then and is currently trading close to the pre-COVID levels. However, the momentum waned in the early weeks of this year. On Friday, the stock traded slightly below its previous close and hovered near the $60-mark.