Shares of Take-Two Interactive Software, Inc. (NASDAQ: TTWO) stayed green on Friday. The stock has gained 7% over the past 12 months. The company reported its fourth quarter 2024 earnings results a day ago, with revenue decreasing and net loss widening versus the prior-year period. Here are the key takeaways from the Q4 report:

Revenue declines, loss widens

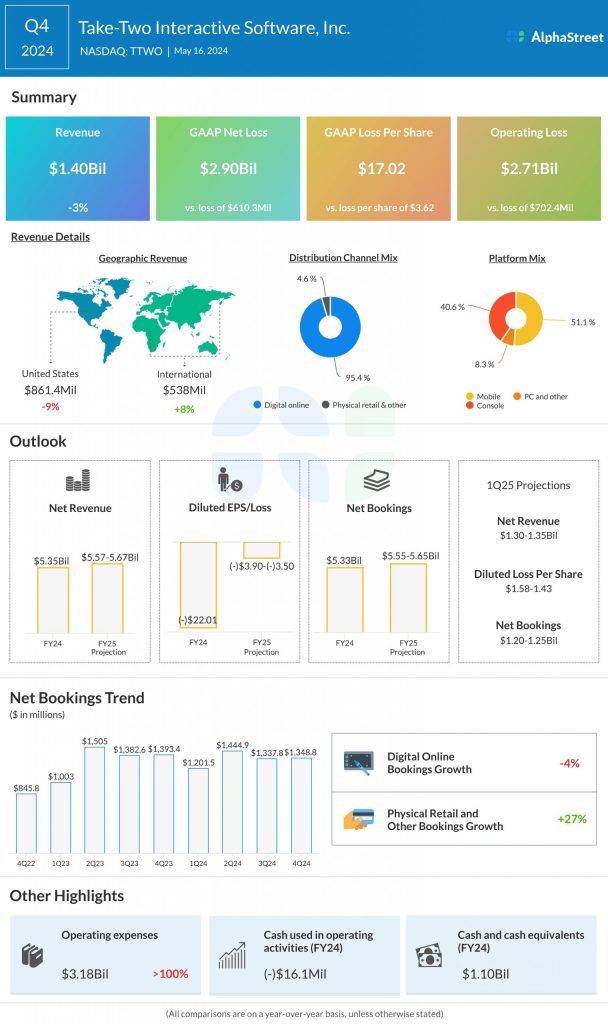

Take-Two posted net revenue of $1.40 billion for the fourth quarter of 2024, which was down 3% year-over-year but managed to surpass estimates of $1.30 billion. Net loss widened to $17.02 per share from a loss of $3.62 per share reported last year. The consensus target was for earnings of $0.09 per share.

Business performance and pipeline

In Q4 2024, net bookings fell 3% YoY to $1.35 billion, but came above the company’s guidance range. As mentioned on the quarterly conference call, bookings were led by gains from NBA 2K24, the Grand Theft Auto and Red Dead Redemption series, and Zynga’s in-app purchases, led by Toon Blast and Match Factory. Recurrent consumer spending declined 2% but was above the company’s outlook.

Take-Two’s pipeline includes around 40 titles through fiscal year 2027. The company cancelled many of its previously planned titles to reduce costs and to focus its resources on the franchises that have the most growth potential.

For FY2025, TTWO has 16 titles in the pipeline, three of which have been launched. These include seven immersive core titles, two independent titles from Private Division, five mobile titles, and two new iterations of prior releases.

The FY2026 and FY2027 pipeline has 24 titles, including 15 immersive core releases, one independent title, five mobile games, and three new iterations of previously-released titles. Take-Two expects net bookings to increase sequentially in FY2025, FY2026 and FY2027 as it releases its pipeline.

Outlook

For the first quarter of 2025, Take-Two expects revenue to range between $1.30-1.35 billion and net loss to range between $1.58-1.43 per share. For fiscal year 2025, the company expects net revenue of $5.57-5.67 billion and net loss per share of $3.90-3.50.

For the first quarter, net bookings are expected to be $1.20-1.25 billion. Net bookings for the full year are expected to be $5.55-5.65 billion, representing a year-over-year growth of 5%.

The main contributors to net bookings are expected to be NBA 2K, the Grand Theft Auto series, the Red Dead Redemption series, Toon Blast, Empires & Puzzles, Match Factory, Words With Friends, and the hyper-casual mobile portfolio. Q1 bookings will include contributions from Zynga Poker, while full-year bookings are expected to see contribution from an unannounced immersive core title from 2K.

In Q1, recurrent consumer spending is expected to increase by approx. 1% YoY, assuming mid-single-digit growth in mobile, flat results for NBA 2K, and a decline for Grand Theft Auto Online. For FY2025, recurrent consumer spending is expected to be up approx. 3% YoY, assuming high single-digit growth for mobile, a slight increase for NBA 2K, and a decline for Grand Theft Auto Online.