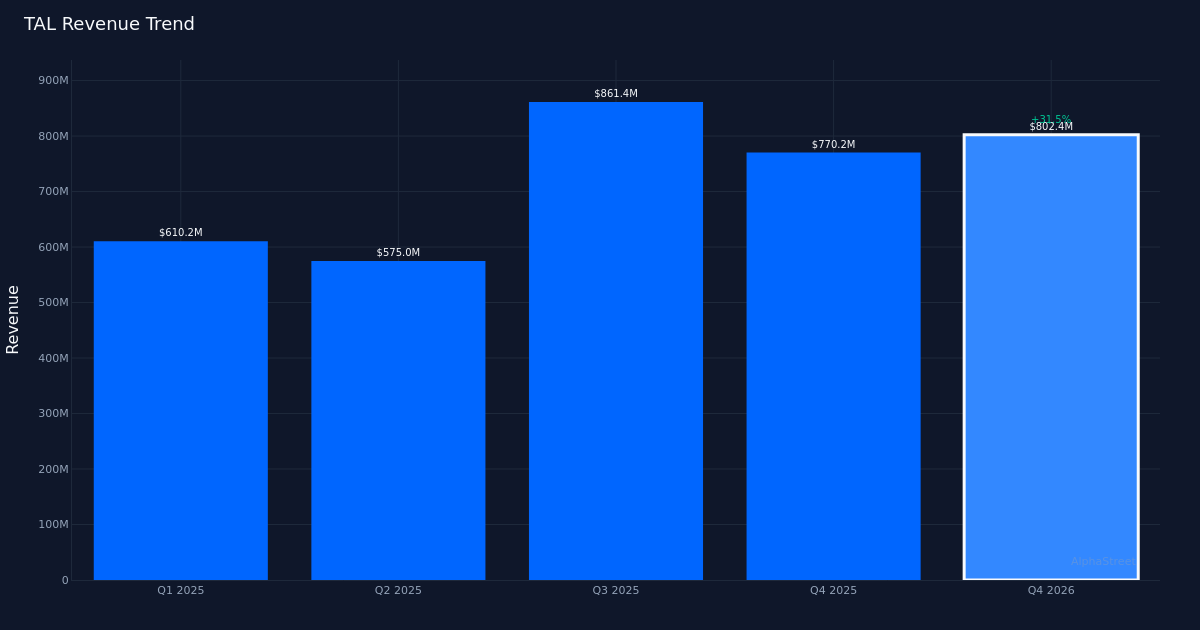

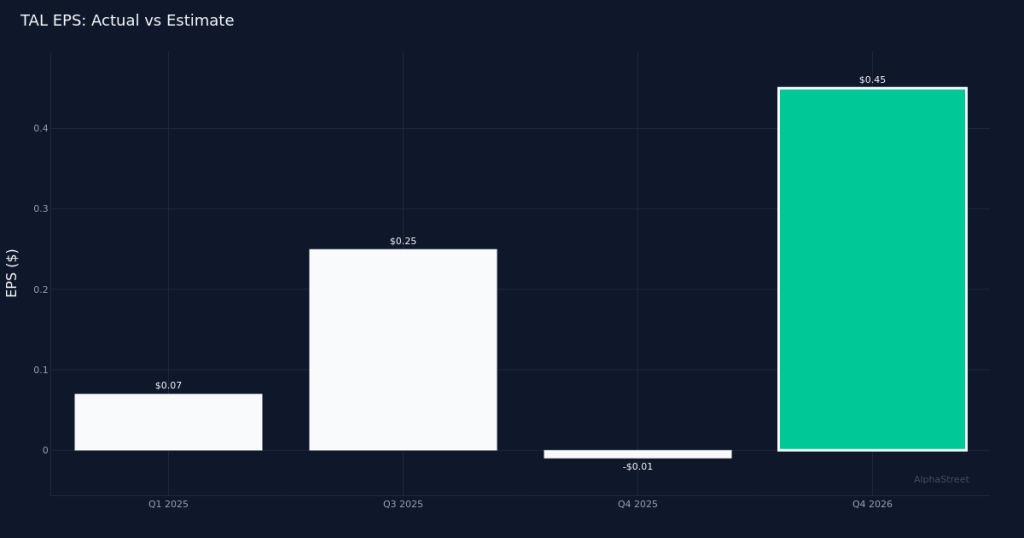

Massive beat. TAL Education Group (NYSE:TAL) delivered a stunning Q4 2026 performance, posting non-GAAP EPS of $0.45 versus the Street’s $0.07 estimate—a beat by 542.9% that signals the company’s transformation efforts are gaining meaningful traction. Revenue totaled $802.4M for the quarter, representing a 31.5% increase from the $610.2M recorded in Q4 2025, demonstrating robust top-line momentum alongside exceptional profitability improvements.

Quality earnings expansion. The company’s net income of $254.5M reflects impressive margin expansion that appears driven by both operating leverage and revenue growth rather than mere cost-cutting. The combination of 31.5% revenue growth alongside outsized earnings beat suggests TAL is successfully scaling its reformed education services business model while maintaining pricing power. This revenue-driven profitability stands in sharp contrast to the defensive cost management many education services peers have relied upon following regulatory headwinds in recent years.

Market validates execution. Shares traded largely unchanged following the report, a somewhat surprising reaction given the magnitude of the earnings surprise. The muted price action likely reflects investors taking profits after what has presumably been a strong run-up into the print, or perhaps caution about sustainability of these margin levels. Wall Street consensus stands at 16 buy, 3 hold, and 0 sell ratings, indicating strong institutional support for the TAL story despite the stock’s lack of immediate response to these results.

Strategic repositioning pays off. TAL’s ability to generate 31.5% year-over-year revenue growth demonstrates the company has successfully navigated China’s evolving education landscape. The education and training services sector has undergone significant regulatory transformation, and TAL’s performance suggests it has effectively pivoted its service offerings to align with current policy frameworks while capturing market share. The company’s ability to more than quintuple analyst expectations on the bottom line while driving substantial top-line growth positions it as a clear category leader.

This article was generated with the assistance of AI technology and reviewed for accuracy. AlphaStreet may receive compensation from companies mentioned in this article. This content is for informational purposes only and should not be considered investment advice.