Target Corporation today reported financial results for the fourth quarter and full year ended January 31, 2026, marking a year of transition as the retail giant works to stabilize sales and boost profitability under new leadership. Despite a modest sales decline, Target delivered solid earnings, improved some margins and outlined a return to growth strategy for fiscal 2026.

Q4 Revenue Performance

-

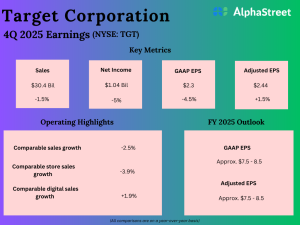

Net sales: $30.5 billion, down 1.5% from Q4 2024.

-

Comparable sales: decreased 2.5% overall, driven by an approximate 3.9% drop in comparable store sales, partly offset by a 1.9% rise in digital sales.

-

Growth in categories such as food & beverage, beauty and toys helped, and non merchandise revenue (e.g., membership programs) climbed over 25%, with membership revenue more than doubling year over year.

-

Same-day delivery, powered by Target Circle 360, expanded by over 30%, reflecting continued strength in convenience-based services.

Target’s sales trend reflects broader softness in discretionary categories like apparel and home goods, but the company saw acceleration in sales and traffic late in the quarter, including a healthy increase in February, a sign that turnaround efforts may be gaining traction.

Earnings and profitability

Target delivered solid earnings despite the sales decline:

Fourth quarter 2025

-

GAAP diluted EPS: $2.30, compared with $2.41 in Q4 2024.

-

Adjusted EPS: $2.44, in line with company expectations and modestly above some analyst views.

-

Operating income: ~$1.38 billion, down ~5.9% from the prior year.

-

Gross margin rate: 26.6%, mildly improved from 26.2% in 2024, aided by lower inventory shrink and fulfillment costs.

Full-year 2025

-

GAAP EPS: $8.13, down from $8.86 in 2024.

-

Adjusted EPS: $7.57, also lower than the prior year but consistent with guidance.

-

Full-year net sales: $104.8 billion, down about 1.7% from $106.6 billion in 2024.

-

Operating income: $5.1 billion, down 8.1% from the prior year, while adjusted operating margins remained stable.

Target continues to manage costs effectively (adjusted SG&A dollars were lower than a year ago), although expense rates reflect deleveraging due to lower sales volumes.

Segment insights and operational trends

Target’s results reflect a mix of resilient and challenged areas:

Sales by category

-

Essentials such as grocery and beauty delivered relative strength.

-

Discretionary categories (apparel and home goods) remained pressured.

Digital and convenience services

-

Digital sales growth was modest, while same day services (pickup, delivery) showed strong adoption trends, underscoring consumer preference for convenience.

-

Membership and marketplace revenue gains helped offset some revenue weakness in merchandise.

Inventory & margin management

-

Gross margin improved slightly due to lower shrink and cost control in fulfillment and digital channels.

-

Higher markdowns and purchase order cancellation costs weighed on some margin components.

Management commentary

CEO Michael Fiddelke said the company navigated through a challenging year while positioning the business for improved performance in 2026 and beyond.

“I’m incredibly proud of how our team navigated through a challenging year in 2025, as they focused on serving our guests while positioning our business for profitable growth in 2026 and beyond,” Fiddelke said.

He highlighted improvements in February sales and traffic as an important milestone on the path back to growth, reinforcing confidence in the company’s momentum.

Management stressed plans to strengthen merchandising authority, elevate shopping experiences, and advance technology investments, all aimed at reigniting sales growth.

Outlook

Target provided guidance for fiscal 2026:

-

Net sales growth: Expected in a range around 2%, driven by improvements in comparable sales plus contributions from new stores and non-merchandise revenue.

-

Operating income margin: Forecast to be ~20 basis points higher than the 4.6% adjusted operating margin recorded in 2025.

-

Full-year 2026 EPS: Expected in a range of $7.50–$8.50 (both GAAP and adjusted), with Q1 EPS forecast to be flat to slightly up year over year, and stronger growth anticipated through the remainder of the year.

This outlook suggests Target expects to break its multi quarter string of declining comparable sales and return to modest growth across all quarters in 2026.

Analysis

Target’s Q4 results tell a nuanced story:

1) Continued pressure on discretionary categories — While essentials and services grew, apparel and home goods, once core revenue drivers, remained soft, reflecting consumer caution.

2) Strong services momentum — Growth in delivery, membership, and marketplace revenue highlights Target’s strategic shift into higher-margin non-merchandise businesses.

3) Sales bottoming? — Improved traffic and February sales trends suggest Target’s turnaround efforts may be gaining traction under new leadership, though full stabilization will need consistent results across multiple quarters.

4) Profit resilience — Despite lower sales, EBITDA and adjusted earnings held up due to cost discipline and margin optimization, signaling that Target’s core profitability model remains intact.

Bottom line

Target’s Q4 and full-year 2025 results reflect a company in transition: declining sales alongside solid earnings performance, driven by strong category performance in essentials and digital convenience services. With a clearer path to net sales growth, improved margins and stronger earnings guidance for 2026, Target appears to be exiting the weak retail cycle and positioning for renewed momentum.

To view the company’s previous earnings and latest concall transcripts, click here to visit the Alphastreet news channel.