Shares of Target Corp. (NYSE: TGT) were up 1% on Tuesday. The stock has dropped 31% year-to-date and 35% over the past 12 months. The retail industry in general has been dealing with changes in customer preferences as well as inflationary pressures which have taken a toll on the profits and margins of several retailers. Target was among those impacted and the company’s recent quarterly results have dampened the sentiment around the stock. Here are a few factors to consider if you have an eye on this retailer:

Markdowns and margins

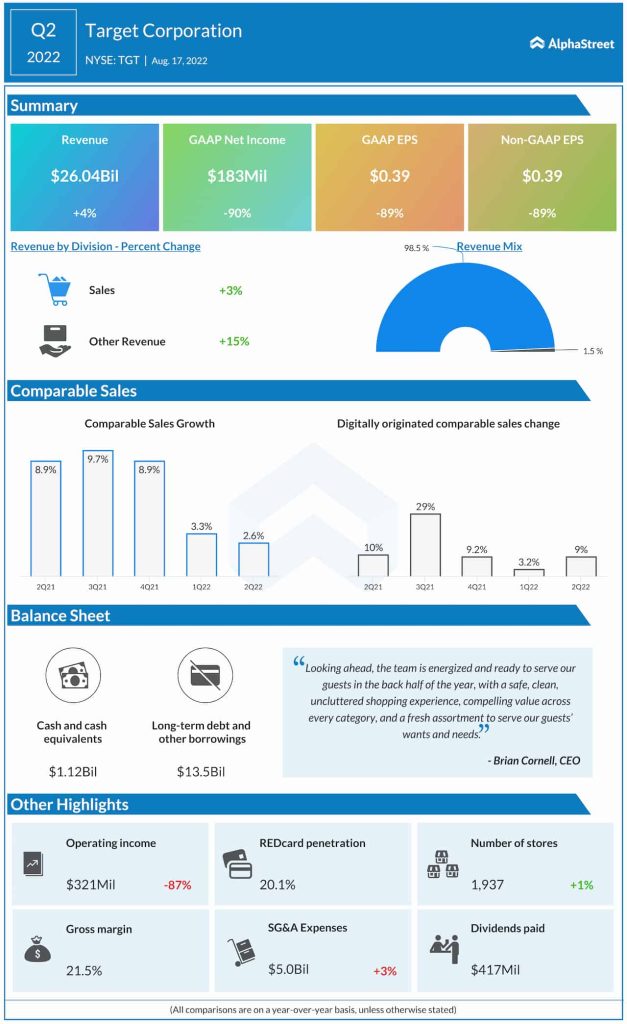

Target’s total revenue for the second quarter of 2022 increased 3.5% year-over-year to $26 billion while comparable sales were up 2.6%, driven by an increase in traffic. The company had to resort to heavy markdowns to move inventory out of its stores which weighed significantly on its profits.

Gross margin dropped to 21.5% from 30.4% in the same quarter last year, hurt by higher markdowns as well as higher costs. Operating margin was 1.2% compared to 9.8% last year. This led to adjusted EPS of $0.39, which was down 89% from last year. This sharp drop in profits overshadowed revenue growth. Despite the company’s optimism that its margins will pick up, concerns persist amid inflationary pressures.

Inventory levels

Target had to resort to heavy markdowns to clear out the excess inventory in its stores. As part of its inventory management efforts, the company reduced its ownership in categories that have been seeing softness and strengthened its position in categories that are seeing higher demand such as food and beverage, beauty and household essentials.

Food and beverage saw comps growth in the low double-digits while beauty and essentials grew in the mid to high single digits during the quarter. Discretionary categories like apparel, home and hardlines witnessed declines. The company has reduced its fall season receipt commitments in many discretionary categories.

Through its inventory management efforts, by the end of the second quarter, Target was able to reduce the physical space occupied by its distribution center inventory by more than 20% compared to the levels seen in June. It expects its DCs to remain at or below 85% capacity through the remainder of the year.

Even so, at the end of the second quarter, Target’s inventory stood at $15.3 billion which was higher than $11.3 billion in the year-ago period. The high inventory levels might lead to more markdowns which could further impact profitability.

Outlook

Target believes that the vast majority of the financial impact of these inventory actions is behind it and that it is capable of delivering a meaningful improvement in operating margin rates in the fall season. Operating margin is estimated to range around 6% in the fall season. Looking ahead, the company expects revenues for the full year of 2022 to grow in the low to mid single digit range.

Despite the company’s expectations for margin improvement, the still-high inventory levels and inflationary pressures continue to be a dark cloud.

Click here to read the full transcript of Target’s Q2 2022 earnings conference call